Opening an hour-long conversation last week with visiting American think tank scholars, a Chinese official said, “I have more questions than answers.” It may have been a throwaway line. But in hindsight, it seems representative.

Here are a few of the big questions I brought back from a quick trip to Beijing:

How much is the Chinese economy slowing?

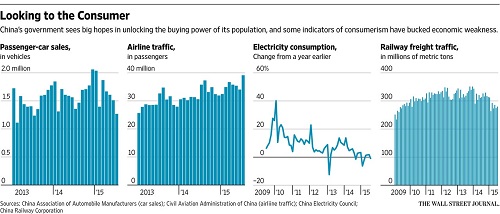

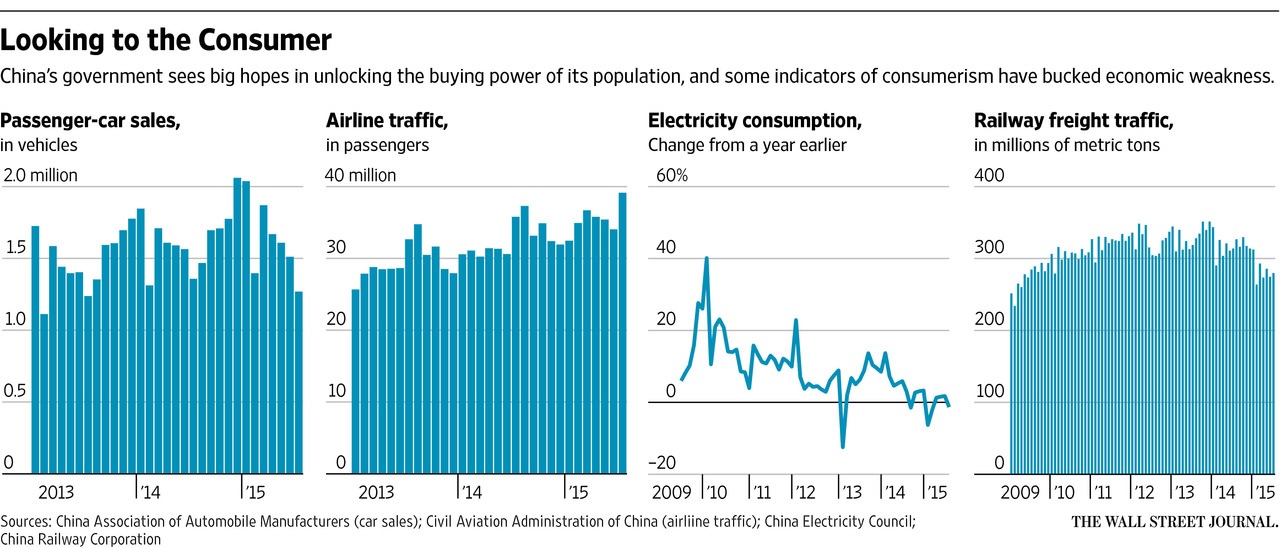

China’s industrial sector has cooled. Labor-intensive manufacturing has lost competitiveness as wages have risen. Demand for big-ticket items is weakening at home and abroad. Plenty of data show that, such as the electricity output that is so widely tracked. The harder-to-answer question is how much China’s growing service sector is picking up the slack. Very little information about that sector is publicly available. In other words, is China’s new economy growing fast enough to offset the weakening of its old economy as it attempts to “rebalance” away from exports and mega-infrastructure projects toward domestic consumption?

If the job market remains tight, then the economy probably is OK. But reliable data are sparse. China has no monthly payroll or household surveys. Wages appear to be rising still, a sign that the economy is holding up. But there are anecdotal reports of unpaid furloughs and reverse migration from cities to the countryside.

China’s central bank–the People’s Bank of China–sounds confident that the softness of the economy is temporary and exaggerated by pessimistic observers, both domestic and foreign. Other officials sound more worried. “China’s economy is in its wintertime. It may be long. It may be short,” said one.

Why have world markets reacted so much to the latest twist in China’s exchange rate policy–the devaluation and announced shift to rely more on markets to set the currency’s value?

A few possibilities, not mutually exclusive: One, the Aug. 11 devaluation was a sign that China’s leaders have information that we don’t that its economy is in bad shape. Two, one of the few constants in the tumult of the past several years has been China’s resolve to keep its exchange rate stable or rising gradually. That predictability is gone. Three, the klutziness of the announcement damaged the notion that, if nothing else, the Chinese government is highly competent.

Competing explanations for the decision underscore divisions within the Chinese government on economic policy. Was it a simple export-boosting devaluation with a little reform tossed in? Or was it an International Monetary Fund-backed move to let markets have more say over the exchange rate at a (domestically) politically convenient moment ? Both?

In any event, what happened was a communications debacle. Chinese officials were stunned by the global market reaction to the yuan and to the instant devaluations by Kazakhstan, Malaysia, and others. After so many years of lecturing Washington about “spillovers” from U.S. economic policy, the Chinese discovered that their economy is big enough that its policies have spillovers, too.

What happens to the currency next?

The short-term answer is easy: China won’t let the yuan depreciate much more against the U.S. dollar before President Xi Jinping’s visit to the U.S. in mid-September. After that, predicting is tougher. Money is flowing out of China through increasingly porous capital controls, putting downward pressure on the currency. More bad news about the Chinese economy, weaker exports, and/or more monetary stimulus will tend to pull the yuan down (either by government fiat or market forces). But China still has a large current-account trade surplus, which leads some officials to argue that the fundamentals may–at some point–arrest the currency’s decline.

What’s happening to the pace of economic reform?

It’s hard to tell. Outside of the stock market (where recent gyrations have spooked officials), financial-sector reforms appear to be continuing, in part so the IMF will include the yuan in its official currency basket. China’s central bank slipped a bit of reform–removing the controls on the interest rate that banks pay on deposits of a year or more, for instance–into a decision to cut interest rates and reserve requirements. But a long-promised policy statement on diversifying ownership of state-owned enterprises so they are more subject to market forces has yet to appear. Changes to the residency-permit system (known as “hukou”) are moving very slowly. So is the sorely needed introduction of competition into telecommunications, which is dominated by monopolies, and other service industries.

Reformers in China are frustrated by resistance to changes, many of which challenge vested interests. The stock-market turbulence and exchange-rate uproar will be used by opponents of reform as further reasons to delay and dilute.

Chinese government rhetoric talks about relying more on market forces. In some parts of the economy, China is moving, haltingly, in that direction. But the government and the Communist Party are reluctant to let go. Skies in Beijing were usually clear last week, supposedly because the government shut polluting factories and took other steps to reduce pollution for an international track and field competition and a big military parade Sept. 3. Government officials who can clear the skies probably believe they can control the stock market, the currency, and the economy, too.

This piece originally appeared on the

Wall Street Journal

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

{kind=link}

Commentary

Op-edFour questions, and answers, about China’s economy

September 1, 2015