The paper summarized here is part of the Fall 2022 edition of the Brookings Papers on Economic Activity (BPEA), the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. The conference draft of this paper was presented at the Fall 2022 BPEA conference. The final version was published in the Fall 2022 issue by Johns Hopkins University Press.

See the Fall 2022 BPEA event page to watch conference recordings and read conference drafts of all the papers from this edition. Submit a proposal to present at a future BPEA conference here.

Read final paper with comments and discussion summary here»

Download data for main paper here»

Download data for Gale comment here»

The US government’s capacity to continue running large budget deficits could be threatened if interest rates remain even modestly higher than currently expected, suggests a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on September 8.

A hypothetical 1 percentage point upward shift in projected interest rates over the next three decades would “require large fiscal adjustments”—tax increases, spending cuts, or both, according to the paper’s authors—Zhengyang Jiang of Northwestern University, Hanno Lustig of the Stanford University Graduate School of Business, Stijn Van Nieuwerbergh of the Columbia Business School, and Mindy Z. Xiaolan of the University of Texas at Austin.

In Measuring US Fiscal Capacity Using Discounted Cash Flow Analysis, the authors use the type of valuation exercise typically applied to corporations to develop “a coherent forward-looking approach to measuring [the government’s] fiscal capacity.” They assume budget deficits and interest rates over the next 30 years as projected in May by the Congressional Budget Office (CBO) and, for purposes of the exercise, that deficit spending ends after 30 years.

“Modest increases in interest rates, of the kind the US economy experienced in the first half of 2022, then lead to sharp increases in the size of required fiscal adjustments.”

They conclude that the government’s capacity to run the projected deficits and then continue financing the debt after 2052 is “quite limited,” even assuming the CBO’s interest rate projections prove accurate.

If the government needs to pay higher-than-forecast interest rates, the duration mismatch between the maturity of Treasury debt and the assumed end to deficits after 2052 further reduces the government’s fiscal capacity. (Treasury debt totaled $22.3 trillion at the end of last year and had an average maturity of about five years.)

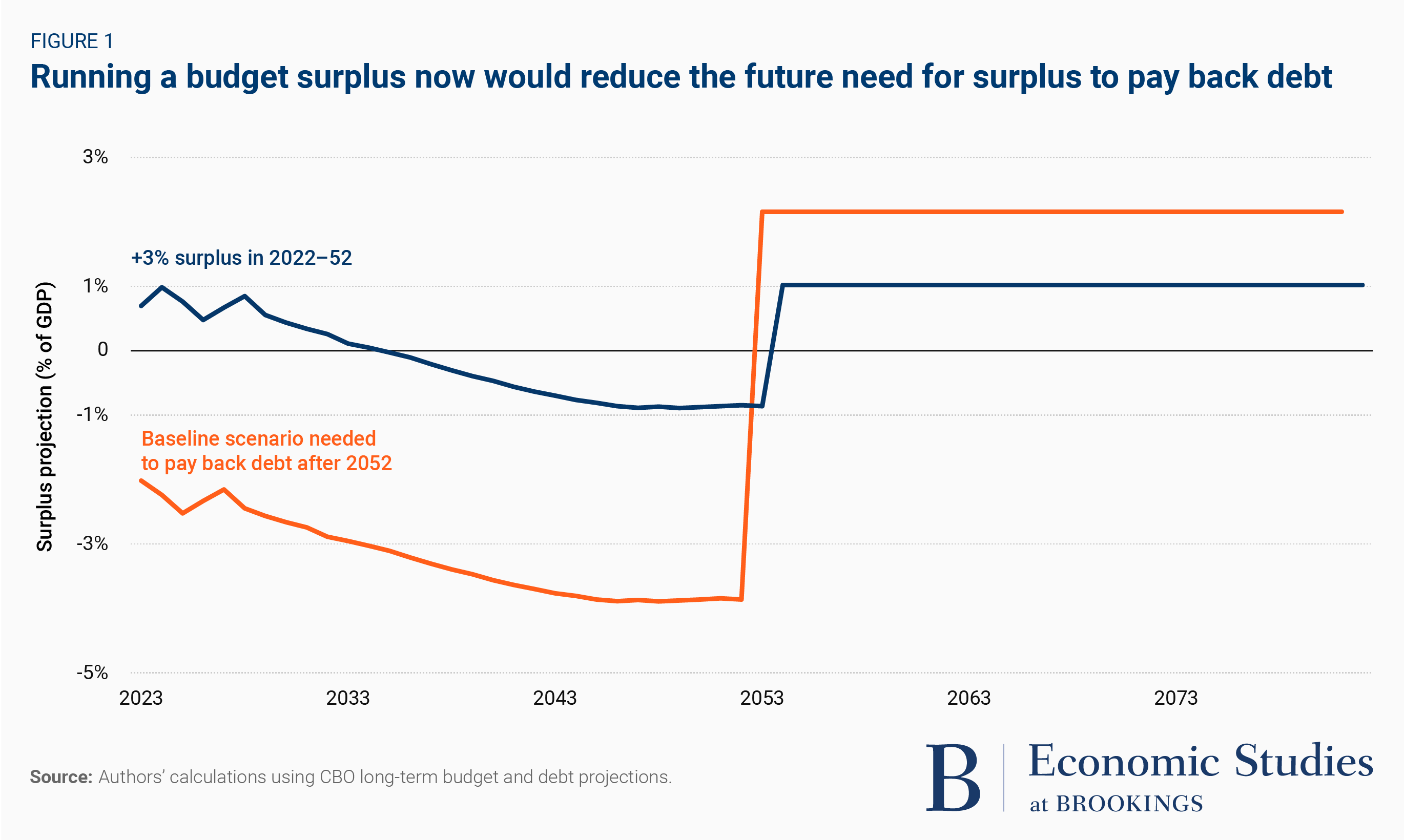

The authors’ baseline scenario (accepting the CBO’s interest rate forecast) suggests that to finance the debt accumulated through 2021, plus the deficits through 2052, the government would have to run a budget surplus equal to 2.16 percent of the gross national product (GDP) for many years after 2052. But if interest rates through 2052 prove to be 1 percentage points higher than the CBO projects, for example because the Federal Reserve reduces its holdings of Treasury and other securities, then the annual surplus needed after 2052 more than doubles to 4.83 percent of GDP.

A similar exercise incorporating the interest rate increases during the first five months of this year into the interest rate forecast nearly triples the projected ongoing annual surplus needed after 2052 to 6.24 percent of GDP, according to the paper.

“Modest increases in interest rates, of the kind the US economy experienced in the first half of 2022, then lead to sharp increases in the size of required fiscal adjustments,” the authors write.

Eliminating all defense spending after 2052, for example, would not be enough to close the gap, Lustig said in an interview with The Brookings Institution.

Alternatively, in the baseline scenario (with the CBO interest rate forecast), the government could shrink this duration mismatch and reduce needed surpluses after 2052 by raising taxes and/or cutting spending now. For example, the government could reduce the need for on-going surpluses after 2052 to 1.02 percent of GDP by running surpluses of 3 percent of GDP from now until then.

Citations

Jiang, Zhengyang, Hanno Lustig, Stijn Van Nieuwerburgh, and Mindy Z. Xiaolan. 2022. “Measuring US Fiscal Capacity Using Discounted Cash Flow Analysis.” Brookings Papers on Economic Activity, Fall. 157-209.

Gale, William. 2022. “Comment on ‘Measuring US Fiscal Capacity Using Discounted Cash Flow Analysis’.” Brookings Papers on Economic Activity, Fall. 210-215.

Lucas, Deborah. 2022. “Comment on ‘Measuring US Fiscal Capacity Using Discounted Cash Flow Analysis’.” Brookings Papers on Economic Activity, Fall. 215-225.

Authors

Discussants

-

Acknowledgements and disclosures

This research was supported by the National Science Foundation grant no. 2049260. Stijn Van Nieuwerburgh is a director at Moody’s Investor Services. Other than the aforementioned, the authors did not receive financial support from any firm or person for this paper or from any firm or person with a financial or political interest in this paper. Other than the aforementioned, the authors are not currently an officer, director, or board member of any organization with a financial or political interest in this paper. David Skidmore authored the summary language for this paper. Becca Portman assisted with data visualization.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).