Studies in this week’s Hutchins Roundup find that increases in minimum-wage result in net losses in employment and earnings among workers with wages below $19/hour, implausibly large sums spent on foreign travel in Chinese official data are actually capital flight, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Minimum-wage increases lead to employment and earnings losses for low-wage workers

Joining the debate over the impact of raising minimum wages, Ekaterina Jardim and co-authors at the University of Washington examine Seattle’s minimum wage increases in 2015 ($9.47 to $11) and 2016 (to $13), and find significantly greater negative effects than some previous research. For low-wage employees (those earning less than $19/hour), the authors estimate that the increase to $13 cut hours worked by 9.4 percent; by a different estimate, the number of low-wage jobs declined by 6.8 percent. They also find that the income from higher wages was not enough to offset the income lost from working fewer hours. A low-wage employee’s earnings decreased by $125 per month (6.6 percent) on average in 2016, they estimate. They do not find these negative patterns with restaurant workers. The magnitude of the effects is large compared to earlier work, and drew immediate criticism from Berkeley’s Michael Reich.

China’s current account numbers distorted by household capital flight

Using counterparty trade data and Chinese international arrival statistics, Anna Wong of the Federal Reserve Board suggests that Chinese households’ purchases of foreign assets (an outflow of capital) are inaccurately recorded as foreign travel by Chinese residents (an import of services). She estimates that financial outflows that are concealed as travel imports grew to around 1 percent of GDP in 2015 and 2016, almost a quarter of recorded net private outflows. As a result, China’s current account surplus was likely lower than reported in the 2000s, increased more sharply in 2014 and 2015 and decreased less in 2016 than official statistics. Wong suggests that Chinese households recently have, in part, replaced the official sector in directing domestic surplus savings abroad.

Clear communication of future actions is especially important for unconventional monetary policy

Assessing several years of unconventional monetary policies by the European Central Bank (ECB) and Federal Reserve, Günter Coenen and co-authors from the ECB argue that communication about new policy tools reduces uncertainty about those policies, especially when providing specific details on implementation such as the planned size of asset purchases. They demonstrate that forward guidance reduces uncertainty more when it is state-contingent or when it covers an extended period of time than when an announcement is open-ended or covers a short time span. Credibility of forward guidance is strengthened when central banks have an asset purchase program in place. These findings suggest that when central banks use unconventional monetary policy tools or forward guidance, they should communicate the expected workings of the tools and provide as much detail about the actions as possible, they say.

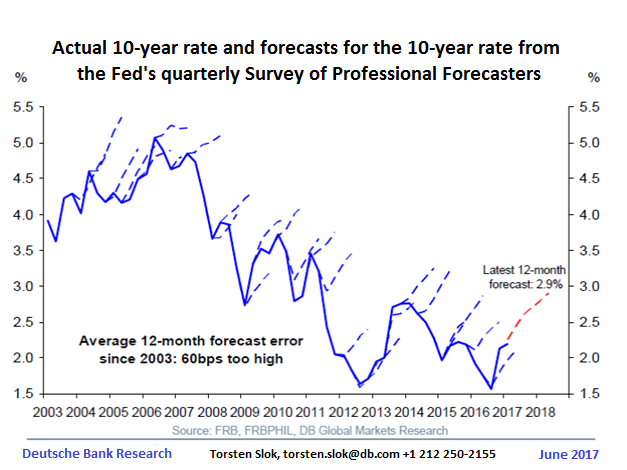

Chart of the week: Wall Street economists have been consistently wrong in 10-year rate forecasts

Quote of the week: “[M]onetary policy is working to build up reflationary pressures, but this process is being slowed by a combination of external price shocks, more slack in the labor market and a changing relationship between slack and inflation. The past period of low inflation is also perpetuating these dynamics,” says ECB President Mario Draghi.

“These effects, however, are on the whole temporary and should not cause inflation to deviate from its trend over the medium term, so long as monetary policy continues to maintain the solid anchoring of inflation expectations. Hence we can be confident that our policy is working and its full effects on inflation will gradually materialize. But for that, our policy needs to be persistent, and we need to be prudent in how we adjust its parameters to improving economic conditions.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Minimum wage increases, Chinese capital flight, and more

Thursday, June 29, 2017