Studies in this week’s Hutchins Roundup find that some state programs for monitoring prescriptions of controlled substances reduce prescriptions of opioids most likely to be abused by Medicaid enrollees, the Fed’s quantitative easing was more effective than forward guidance during the zero lower bound period, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Some prescription drug monitoring programs significantly reduce the use of opioids with the highest risk of abuse

Currently about half the states require prescribers of opioids to register with – and, in some states, to use – a statewide database gathering information from pharmacies on dispensed prescriptions of controlled substances. Using data on opioid prescriptions for Medicaid enrollees over 2011–2014, Hefei Wen of the University of Kentucky and Bruce Schackman, Brandon Aden and Yuhua Bao of the Weill Cornell Medical College find that such mandates were associated with a 9–10 percent reduction in the use of Schedule II opioids, the class of prescription opioids with the highest risk of abuse and dependence. Simply requiring prescribers to register had a significant effect on the number of prescriptions written.

The Fed’s quantitative easing was more effective than forward guidance during the zero lower bound period

From December 2008 to December 2015, the Fed kept its key interest rate near zero and turned to forward guidance and large-scale asset purchases, also known as quantitative easing, to help the economy. Eric Swanson of the University of California at Irvine shows that both of these policies had a significant impact on various asset prices, similar in magnitude to the impact of the federal funds rate before the zero lower bound period. However, while the effects of forward guidance died out quickly, the effects of quantitative easing were more persistent, making large-scale asset purchases the more effective policy of the two, he concludes.

Speedier flows of information lead foreign exchange markets to react less to macroeconomic news

Improvements in information technology might make financial markets react more to new economic data by facilitating algorithmic trading, for instance. Or they might make markets react less because they spreads information more quickly to all investors. Using data on over 50 currencies during 1997-2015, Barry Eichengreen of the University of California, Berkeley, Romain Lafarguette of the IMF and Arnaud Mehl of the ECB find that connections to fiber-optic submarine cables, which connected different countries at different times, dampen the response of exchange rates to monetary policy news by 50 to 80 percent. “Wider and more comprehensive provision of information may have a dampening effect on volatility,” the authors conclude.

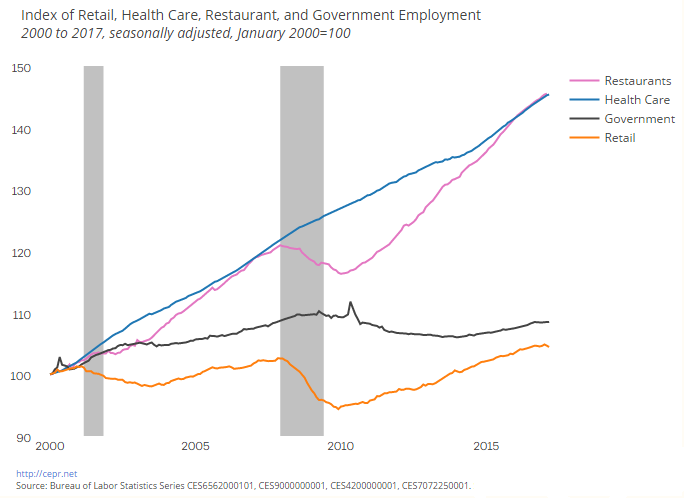

Chart of the week: Employment in restaurants and health care has grown far more over the past 15 years than in government and retail

Quote of the week: “What accounts for this improved resilience of the euro area economy?” asks European Central Bank president Mario Draghi.

“Certainly the recovery cannot be explained by ‘endogenous’ or underlying growth forces, which were unusually weak in its early phase. Nor can several of the ‘exogenous’ factors that have supported previous euro area recoveries provide an answer… First, in the past euro area growth has been closely interdependent with world trade… Since mid-2014, however, world trade has weakened considerably… Second, though fiscal policy has stopped being a headwind – as it was during the 2011-13 period – it has not been much of a tailwind to the recovery either… Third, the contribution of the supply side to the recovery has so far been limited… So based on simple growth accounting, there are only two ‘exogenous’ factors left that can realistically explain the resilience of the recovery: the collapse in oil prices in 2014-15 and our monetary policy….All told, we estimate that half of the extra GDP growth achieved during the current recovery has been attributable to our policy, with a material contribution from oil prices as well.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Opioids, unconventional monetary policies, and more

Thursday, April 13, 2017