Last week, the Fed announced its intention to keep interest rates at historic lows until the unemployment rate drops below 6.5 percent, so long as projected inflation remains below 2.5 percent. The Fed has now explicitly linked its interest-rate policy with future economic conditions.

But how long it will take to reach 6.5 percent?

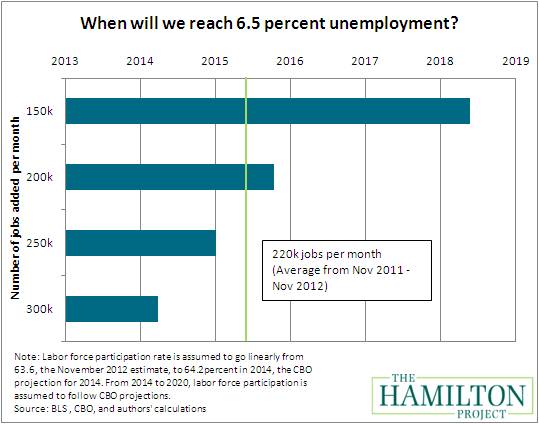

In today’s analysis, The Hamilton Project presents a range of estimates of when the unemployment rate will reach the Fed’s benchmark. The chart below shows how long it will take to reach an unemployment rate of 6.5 percent based on different assumptions of monthly job growth.

Predicting when the economy will get back to 6.5 percent unemployment depends on many factors. For example, if monthly job growth averaged 150,000, the unemployment rate would not reach 6.5 percent until 2018. Employment growth—as measured in the household survey—has averaged about 220,000 jobs per month over the past year. Continuing at this pace, it would take about two and a half years to get back to 6.5 percent [1].

While the Federal Reserve has set its benchmark at 6.5 percent, that is significantly higher than the unemployment rate in the year before the start of the Great Recession, which never exceeded 5 percent. Returning to pre-recession normal will necessarily take even longer.

The Hamilton Project’s “jobs gap” calculator allows you to explore how long it will take to return to the pre-recession employment rates, rather than unemployment rates, at various levels of job growth each month. The jobs gap calculator can be found here, and the state-by-state breakdown of the jobs gap, updated each month, can be accessed here.

[1] Because the unemployment rate is defined as the share of the labor force without a job, changes in the labor force—the number of American either working or actively searching for work— have important implications for the unemployment rate. Consequently, these estimates depend critically on assumptions about changes in the labor force. Our calculations use the 2011 estimates from the Congressional Budget Office of labor force participation over the next decade, which are subject to uncertainty; to the extent that the labor force grows more quickly over the next few years, the length of time required to return to 6.5 percent will be longer (and the converse is true if labor force growth is slower).

Michael Greenstone

is the director of The Hamilton Project and

Adam Looney

is its policy director. For more about the Project, visit

www.hamiltonproject.org

.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How Long Will it Take to Get to 6.5 Percent Unemployment?

December 14, 2012