African hopes are on the rise with the African Continental Free Trade Area (AfCFTA) that became effective on January 1, 2021. Foreign Policy celebrated the agreement as a game-changer for Africa, with the potential to create the world’s largest free trade area since the creation of the World Trade Organization. The excitement is understandable. After all, the AfCFTA will cover a market of 1.2 billion customers and an estimated $3 trillion in combined GDP, with the potential of increasing intra-African trade by over 50 percent. According to the World Bank, the agreement could lift millions out of extreme poverty and add $76 billion in income to the rest of the world.

But the successful implementation of this trade agreement is going to be a long and uphill path. Political turmoil, infrastructure gaps, and security threats are among the impediments to free trade in much of Africa. Of particular importance here is the mix of exchange rate regimes from one sub-regional market to another, which entails heterogeneous reactions to price, fiscal, productivity, and debt shocks, resulting in significant misalignments and substantial growth disparities among countries. In this blog, we provide our thoughts on the relevance of monetary and exchange rate policy for countries with different governance structures and membership in trade agreements.

What are exchange rate misalignments and why do they matter?

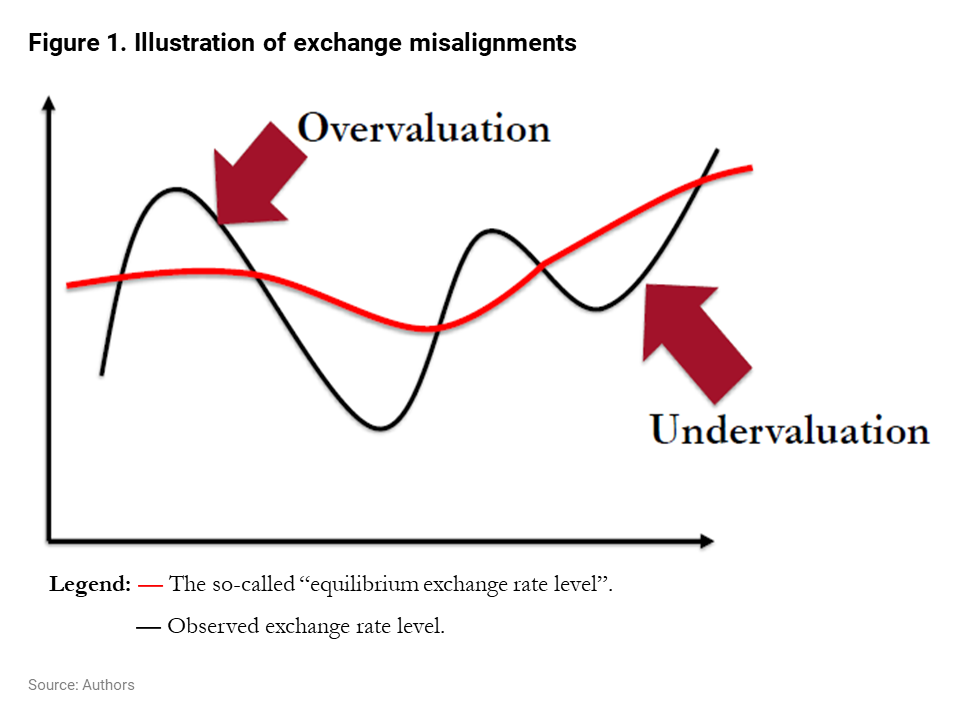

Exchange rate regimes essentially define rules under which central banks would intervene to determine the exchange rate—the price of one currency in terms of one other currency or a basket of currencies. These rules translate into a wide range of regimes, from purely floating exchange rates to fixed or rigid regimes in which the central bank tries to make sure that the exchange rate does not vary (too much) over time. A big problem for economic policy is that the diversity of exchange rate regimes entails divergent exchange rates and big departures from equilibrium levels, viz., what the exchange rate level would be in the best possible situation for a country. Deviations on either side of the equilibrium level (see Figure 1) are referred to as exchange rate misalignments. On the one hand, misalignments may translate into overvaluation phases where a country’s currency value is higher than it should be, implying lower competitiveness compared to trading partners. On the other hand, they might instead converge to undervaluation periods characterized by a cheaper currency value than expected implying, ceteris paribus, higher competitiveness margins.

The implications of these different dynamics are straightforward. If countries face an overvalued currency, the central bank will need to sell its foreign currency reserves to “mop up” the excess supply of its own currency. That in turn could potentially reduce the domestic rate of inflation and lead to a nominal appreciation, moving the exchange rate’s fundamental value toward the peg. The success of this strategy is obviously limited by the size of the country’s reserves that can become seriously depleted in case of a persistent misalignment. And if market agents believe that the government lacks sufficient reserves to support the peg, then a country is exposed to a speculative run on its currency.

The implications of these different dynamics are straightforward. If countries face an overvalued currency, the central bank will need to sell its foreign currency reserves to “mop up” the excess supply of its own currency. That in turn could potentially reduce the domestic rate of inflation and lead to a nominal appreciation, moving the exchange rate’s fundamental value toward the peg. The success of this strategy is obviously limited by the size of the country’s reserves that can become seriously depleted in case of a persistent misalignment. And if market agents believe that the government lacks sufficient reserves to support the peg, then a country is exposed to a speculative run on its currency.

The situation differs slightly when the currency is undervalued. Faced with this scenario, a central bank would react by expanding its own money supply to buy foreign currency. Since there are no inherent limits to the creation of fiat money, there would be no obvious limits to the central bank’s ability to play this game. We know that money supply expansion may eventually be inflationary, but that would itself tend to drive down the freely-floating value of the currency.

Currency regimes are not by themselves the reason for misaligned exchange rates

Carmen Reinhart and Kenneth Rogoff have looked at the costs and benefits of alternative exchange rate regimes with respect to economic performance and found that unified exchange rate regimes vastly outperform dual or multiple exchange rate arrangements. Although the authors do not impute causation in their analysis, Nigeria’s multiple exchange rate windows and the country’s dismal growth performance over the last 10 years or so seem to be a good recent illustration of that finding. Despite their benefits (e.g., a reduction in uncertainty), fixed regimes gradually lead developing countries to overvaluation over time, undermining competitiveness and reducing trade. Based on recent research by one of us, we also posit that the extent of the misalignment in flexible regimes appears significantly higher than in fixed regimes.

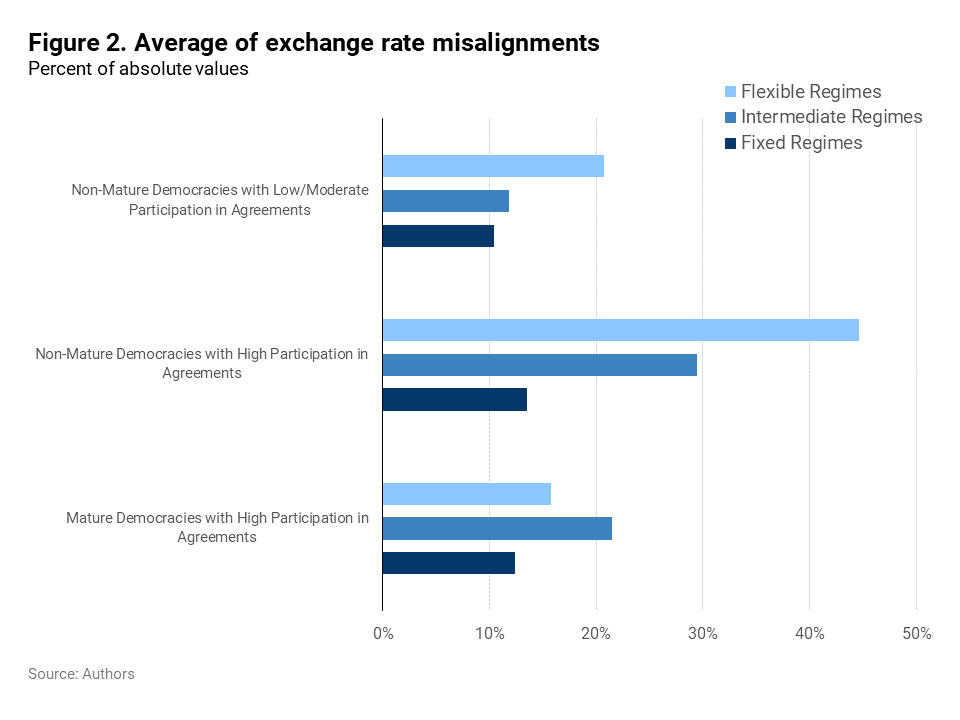

The contribution of this work, summarized in Owoundi’s Policy Research Working Paper, is to jointly consider membership in regional trade and investment agreements and political governance as explanatory factors for exchange rate misalignments. It shows that fixed regimes tend to limit exchange rate misalignments in less mature democracies as participation in trade and investment agreements increases, whereas more mature democracies are able to avoid these misalignments through the use of flexible exchange rate regimes. However, for mature democracies, high openness to trade and investment might also come with some drawbacks in the form of higher misalignments in non-fixed regimes (see Figure 2). Hence, by combining three topics usually addressed separately in the economic literature, Owoundi’s findings suggest that the exchange rate system per se is not responsible for misalignments. Instead, what seems to matter a lot is whether countries have mature democracies and are members of trade/investment agreements.

What lessons for the AfCFTA?

Because of weak governance, less mature democracies may find it harder to respond to exogenous shocks. The variety of exchange rate arrangements within a single free trade area represents another level of complexity, resulting in disagreements between “winners” and “losers”. Winners are likely to be found in countries with stronger governance and democratic institutions with somewhat more flexible regimes where sound monetary and exchange rate policies can lead to competitiveness gains. On the other hand, losers would be most commonly found in less mature democracies and a higher tolerance for overvalued currencies for which the AfCFTA might not yield net positive gains given their weaker competitiveness.

We conclude this blog in the same fashion as Jeffrey Frankel, by reiterating that no single exchange rate regime is good for all countries. Good governance plays a key role in good macroeconomic management. We postulate that more mature democracies are likely to be more resilient to shocks and benefit more from the AfCFTA. The less mature democracies have two alternatives: resist continental trade and investment agreements or institute stronger democracies at home. AfCFTA’s success will depend on how effective it is in convincing them to eschew the former and adopt the latter.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The African Continental Free Trade Area and exchange rate misalignments

April 27, 2021