Many countries have made hydropower a key pillar of their renewable energy strategies. Hydropower has been a reliable and affordable source of power for over a century. Relative to other renewables such as wind and solar, reservoirs give electricity companies some measure of control on when to produce a certain level of energy. Moreover, reservoirs can contribute to flood control, irrigation, and management of water supply. There are now 35 countries in the world that cover more than 50 percent of their electricity production with hydropower (sample includes 141 countries).

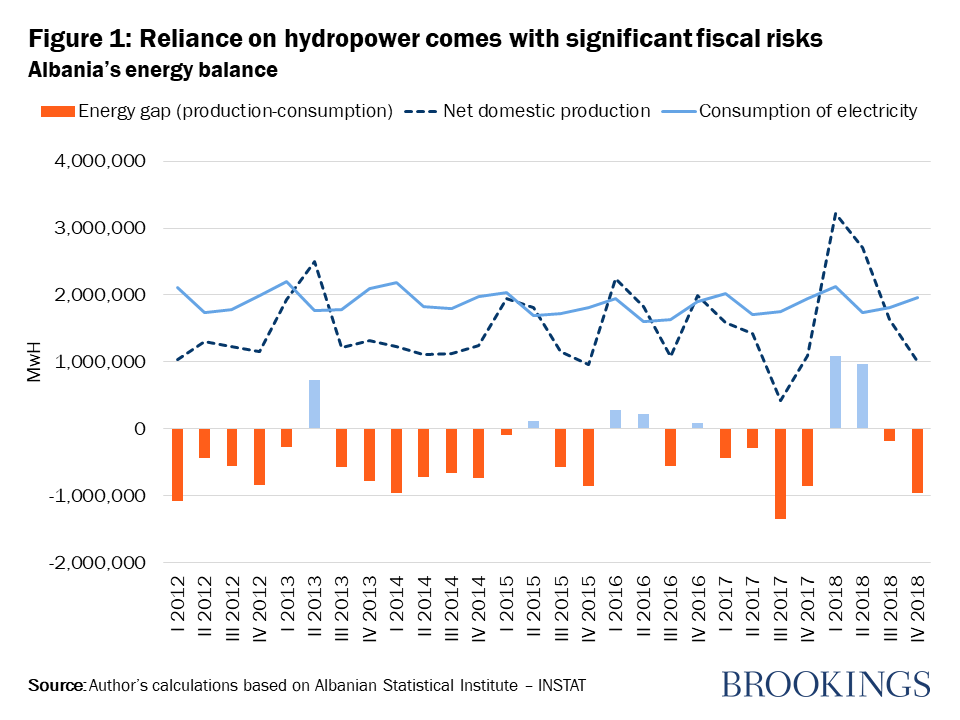

However, the success of hydropower can come with financial risks linked to volatility in production. A particularly striking example is Albania, where nearly all domestic power production comes from hydropower. As a result, electricity production is highly dependent on variations in rainfall across seasons and across years. Domestic electricity production falls short of consumption in periods of low rainfall and when reservoirs run low. Albania’s energy sector is then required to purchase expensive electricity from abroad to meet domestic needs—selling to regulated end users at the fixed regular tariff. When low rainfall coincides with high international energy prices, this results in large financial gaps at Albania’s state-owned electricity utilities (see Figure 1). The government is then forced to intervene. For instance, in 2016, such net budget lending to Albania’s electricity sector amounted to 0.4 percent of GDP, and 0.6 percent of GDP in 2017.

Albania needs better management of financial risks resulting from its dependence on hydropower. Governments and their corporate partners in the energy sector have a menu of risk mitigation instruments that can be deployed, either separately or in combination. Building on international experience in managing fiscal risk in hydropower, such as the hydropower risk mitigation strategy deployed by Uruguay with support of the World Bank, three main lessons stand out.

First, countries need to increase the reliability of their domestic energy production base, by complementing hydropower through a diversified energy base and by strengthening hydro reservoir management. Countries need to encourage diversification of their energy base, complementing hydropower with other energy sources that can meet electricity consumption during periods of low rainfall. Other clean sources of energy such as solar and wind energy are promising complements. Investment in dams and reservoirs to give energy companies optimal control over strategic water storage opportunities to smooth out hydropower across periods of high and low rainfall can complement this approach. With sufficient domestic production to cover consumption, whether in dry or wet years, countries can avoid having to import electricity, limiting their vulnerability to high and volatile international energy prices.

Second, the energy sector needs to develop financial instruments to smooth out financing needs, particularly when facing a combination of volatile domestic hydro generation and volatile international import tariffs. Emergency budget lending to the energy sector in years with low rainfall and high energy import prices can put public finances at risk. Transfers from the budget also hollow out the principle proclaimed by many governments that electricity companies should be run on a commercial basis. Instead, the energy sector itself needs to develop its own financial instruments to smooth out financing needs. A segregated account—with clearly defined contribution and pay-out rules—can automatically ring-fence a fraction of profits during surplus periods, which can then be used to fund financing gaps due to adverse weather and international price events. A financial guarantee can charge a regular premium against an insurance payout to the electricity companies in years of low domestic rainfall and high electricity import prices. A contingent loan or credit line can ensure that credit is available to the energy sector when facing financing gaps.

Third, liberalization of electricity tariffs or a temporary tariff surcharge during dry periods can help transfer risk away from the energy sector. As more customers face tariffs determined by the market, their electricity prices will fluctuate to reflect supply conditions. In periods of low hydropower production, prices will increase, generating additional funds for the electricity companies and incentivizing customers to adapt their consumption patterns to available production. Proxying this, regulated tariffs could be augmented with a temporary tariff surcharge during periods of low rainfall. Alternatively, a permanent hydro-risk premium could compensate the electricity companies for bearing the volatility from hydropower. Small tariff adjustments are often sufficient to protect the sector from substantial fiscal outlays.

Implementing this hydropower risk mitigation strategy is daunting. Increasing the reliability of domestic supply, including by diversifying the energy base, will take time and will require the mobilization of considerable new investments. Equally, electricity companies may be reluctant to pay up-front costs for expensive financial instruments to smooth out their financing needs, as long as the regulated tariffs are not cost-reflective and there is an implicit expectation of government bailouts. Contingent loans or credit lines can be expensive if financial conditions are too stringent or if the energy sector does not collect sufficient revenues to repay the loan quickly. This suggests that a measured, gradual, and combined implementation of these different categories of risk mitigation instruments is needed.

Many countries are already gaining from the rollout of hydropower risk management instruments. In the United States, local electricity companies—such as the Roseville electricity company in California—have implemented hydroelectric adjustment tariffs that are contingent on weather conditions. In China, the Meiyan electricity company has purchased weather insurance. In Mali, a segregated account has been set up to smooth fluctuations in hydropower production.

Hydropower risk mitigation tools can play a key role in meeting the Sustainable Development Goal to substantially increase the share of renewable energies in the global energy mix. Risk mitigation tools hold the promise of de-risking hydropower. As such, they may be the crucial ingredient that helps tilt the balance the next time a country decides whether to invest in clean hydro or dirty coal.

Related Books

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Managing financial risks from hydropower

May 1, 2019