In Ivory Coast, the poor prefer to keep their savings under their mattresses or in informal community associations, while the wealthy invest directly in real estate or send their money offshore. People’s reluctance to use local banks explains to a large extent why financial intermediation is still nascent in the country. The lending rate (as of percent of GDP) is today three to four times lower than in middle-income African countries such as Morocco, Namibia, and South Africa. The gap is even greater when compared to the emerging countries of Southeast Asia. Why are Ivorians not backing up their banks even if it would be safer and potentially more profitable for each person? How could one close the apparent “trust gap” between citizens and the banking sector?

Little gains, huge costs for savers

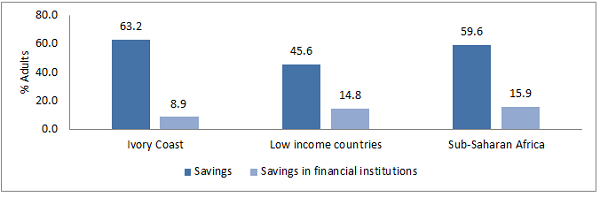

In Ivory Coast, only one out of eight savers opts to put their savings in a bank or a financial institution. This is half of the African average and a third of the levels observed in low-income countries. There is clearly a lack of trust in the relationship between Ivorian savers and their banks, which partly broke down during the 10-year political crisis that only ended in 2011. It has also been weakened by the failure of several public banks that had to be closed down, restructured, or privatized in recent years. As expected, it will take some time to rebuild this trust.

Figure 1: Ivorians do save money but not in their financial institutions

Source: http://datatopics.worldbank.org/financialinclusion/

However, the low propensity of Ivorians to save in their financial institutions can be interpreted as a simple portfolio choice. They are favoring other opportunities that offer higher rates of returns. Indeed, opening and managing a bank account is costly and does not include many benefits. The normal travel time to a bank or ATM is long because the density of the banking infrastructure is low with less than two bank branches and about five ATMs per 100,000 adults, while the average in Africa is four and 5.3 respectively. Then, most banking transactions are slow and costly, as, for example, it takes three times longer to cash a check in Ivory Coast than in France. Moreover, customers have to pay excessive commissions since non-interest income represents more than 60 percent of banks’ revenues in Ivory Coast, compared to only 40 percent in Morocco and South Africa.

Faced with excessive costs for their banking transactions, Ivorians turned to mobile phone operators. Like in other parts of Africa, Ivory Coast has experienced a mobile money revolution. There are now more adults with mobile money accounts (24.3 percent) than with bank accounts (15 percent). In fact, Ivory Coast has the fifth highest rate of mobile money accounts in the world behind Kenya (58 percent), Somalia (37 percent), Uganda (35 percent), and Tanzania (32 percent). These mobile accounts facilitate payments and transfers of funds, but they do not give credits, which is one of the main functions of a financial system.

Closing the gap between savers and banks

If Ivory Coast wants to develop a performing and inclusive financial system, its leaders should encourage banks, including microcredit institutions, to build stronger relationships with their customers. Banks can reduce their transaction costs through innovation and partnerships. For example, they could build small and mobile branches in less population dense areas in combination with microfinance institutions or diversify their distribution network through the inclusion of non-banking agents. Such expansion was achieved in Kenya, Tanzania, and Brazil. Concurrently, local banks should also take more advantage of the information and communications technology revolution. They are already doing it, but they still lag behind their competitors in East Africa or Nigeria where banking has increasingly become possible through a simple application in their customers’ smart phones. Finally, creating stronger relationships also means that Ivorian banks will have to be more innovative by introducing new financial products, such as leasing and factoring, which are better adapted to the limited resources of their clientele.

The second option would be to transform non-banking financial institutions into banks, for example, by allowing them to create credit. This transformation has already begun in Kenya for mobile operators. In 2013, the operator Safaricom introduced a (micro) credit facility in partnership with a bank (M-Shwari), which currently serves more than 10 million customers. Microfinance institutions could be allowed to deliver debt and credit cards to their customers.

Needless to say, these two options will require flexible but prudent regulation: flexible regulations because of the emergence of M-Pesa and other financial innovations in East Africa; prudent regulations because there is a need for close monitoring and supervision to avoid excessive risks by financial institutions. Engaging the clients of banks through better financial information and education has also proved to be a good means of improving both the efficiency and accountability of the system. The balance between innovation and prudence will have to be stricken by Ivorians and as well as regional leaders within the West African Economic and Monetary Union if they want to advance their financial system toward economic emergence.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Why Ivorians do not use their banks?

July 14, 2016