The United Nations predicts that the African continent will be one of the most severely impacted regions in the world by climate change, which will manifest in widespread water stress and declining agricultural yields throughout the continent, exacerbating food insecurity, malnutrition, and poverty. However, a recent report from the Stockholm School of Economics’ Sustainable Finance Center highlights the role of green bonds—a relatively new, innovative financial product that raises funds for environmentally aligned sustainable development projects in accelerating climate change mitigation and adaption. In spite of green bonds’ potential, the author also finds that the African private and public sectors have lagged behind other emerging markets in their issuance of these innovative bonds.

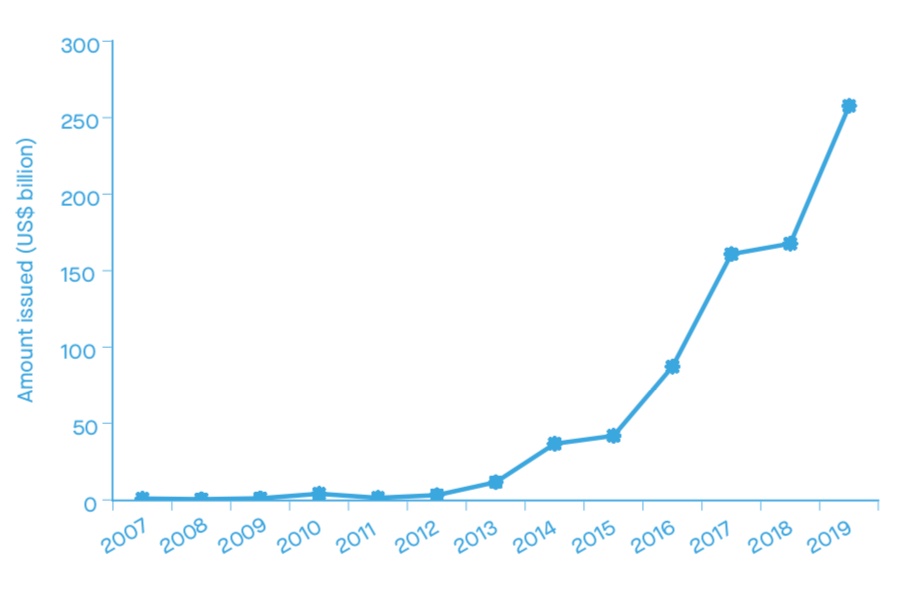

Although characterized by all the same features of a traditional bond in terms of structure, risk, and expected returns, green bonds are distinguishable by their environmental purpose. First issued in 2007 by the European Investment Bank, green bonds—also known as climate bonds—direct financing exclusively to projects with positive climate, environmental, and sustainability outcomes across a myriad of sectors, including energy, transportation, construction, agriculture, and water. These projects span from renewable energy infrastructure and upgrading energy efficiency to low-carbon transportation and buildings. As seen in Figure 1, the global market for green bonds experienced an explosion after 2013, with a more than 300-fold increase in issuance between 2007-2019 and a 104 percent average annual growth rate over the same period. The author attributes growing appetite for investment vehicles with positive impacts on climate and the environment to their reputational benefits, as well as to the exponential growth of this new market. In fact, according to the Harvard Law School Forum on Corporate Governance, the demand for green bonds gained significant momentum following the drafting and signing of the Paris Climate Agreement in 2015.

Figure 1. Annual green bond issuance

Source: George Marbuah, Stockholm Sustainable Finance Centre, “Scoping the Sustainable Finance Landscape in Africa: The Case of Green Bonds,” 2020.

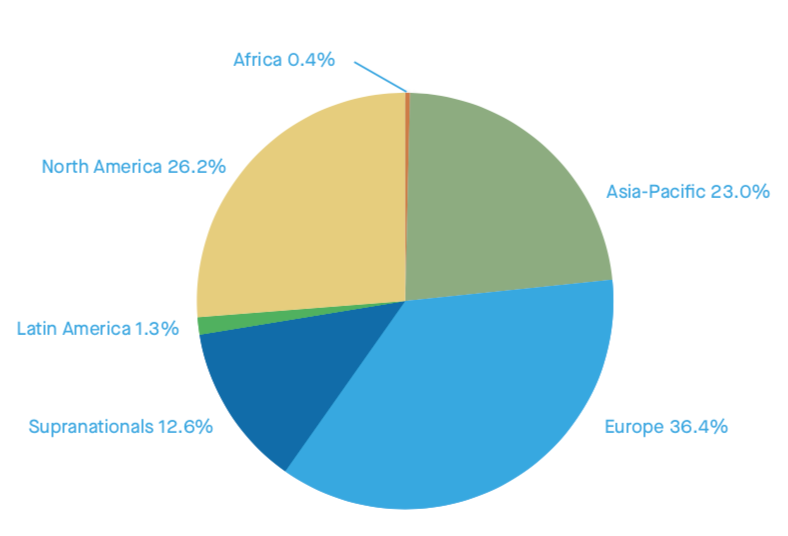

While the explosive growth of green bond issuance signals positive inroads for facilitating sustainable development, Africa has been the slowest adopter, limiting the potential for these innovative financial products to raise ancillary capital for sustainable development throughout the continent. Figure 2 shows the composition of the total green bonds issued by region from 2007 to 2018, where Africa constitutes a mere 0.4 percent of the market share by value.

Figure 2. Composition of total green bond issuance by region (2007-2018)

Source: George Marbuah, Stockholm Sustainable Finance Centre, “Scoping the Sustainable Finance Landscape in Africa: The Case of Green Bonds,” 2020.

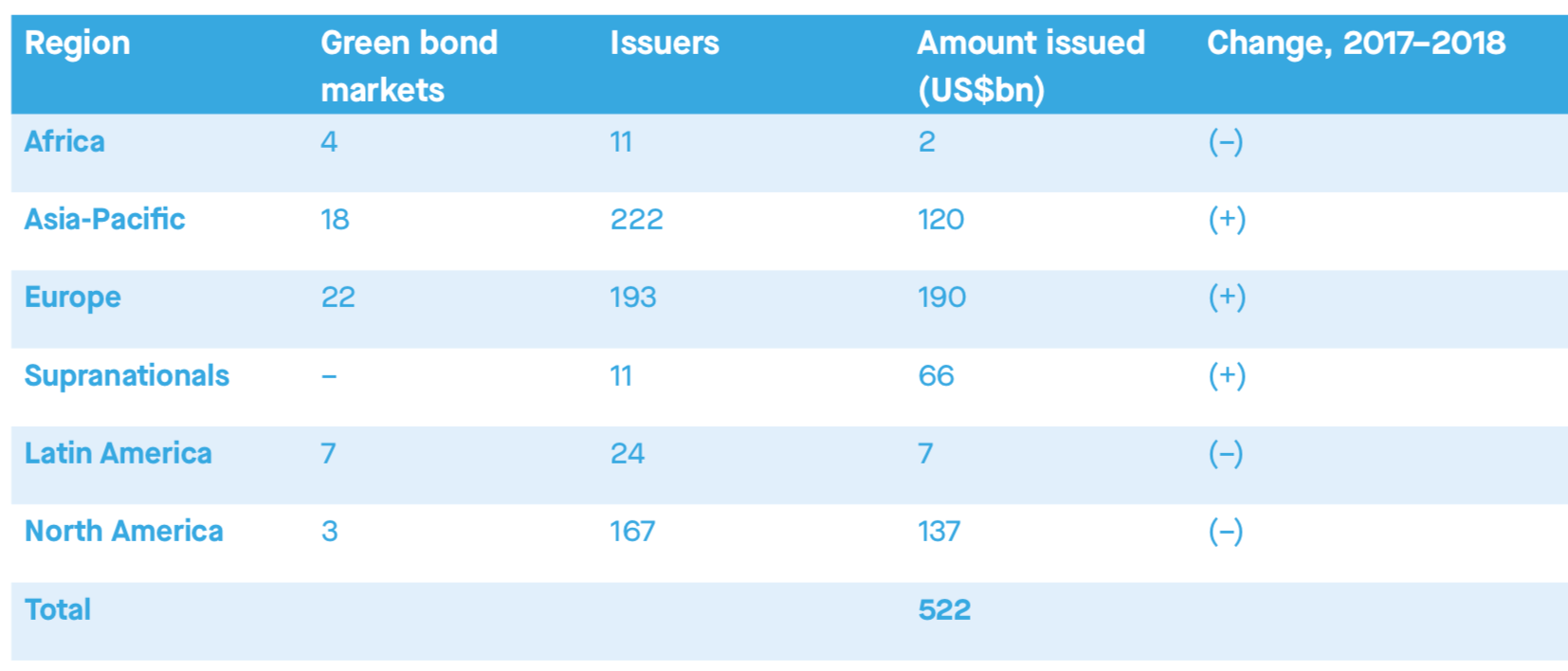

Table 1 breaks down green bond issuance by region, revealing that Africa issued just 11 green bonds between 2007-2018. In terms of actual funds, the $2 billion raised by these bond issuances in Africa is only a fraction of what other emerging markets have raised; Asia-Pacific and Latin America, have, respectively, issued 222 and 24 green bonds and raised $120 billion and $7 billion over the same time period.

Table 1. Breakdown of green bond issuance by region

Source: George Marbuah, Stockholm Sustainable Finance Centre, “Scoping the Sustainable Finance Landscape in Africa: The Case of Green Bonds,” 2020.

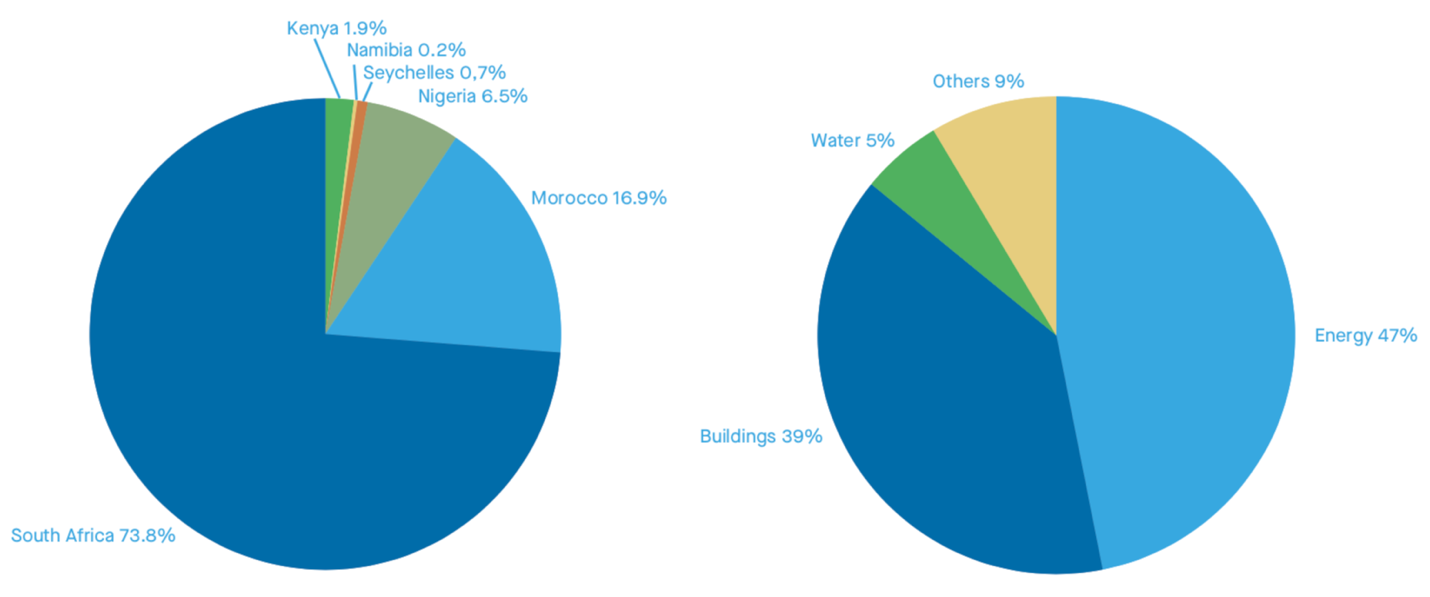

Within Africa, the distribution of the funds raised by green bond issuance has been overwhelmingly concentrated in South Africa. Figure 4 reveals the share of green bonds issued by country (left) and by use of the proceeds (right). With nearly three-fourths of the total market share, South Africa leads the continent by an extremely wide margin. Add in Morocco and Nigeria, and these three countries make up more than 97 percent of the total issuance of green bonds in Africa. The right panel of Figure 4 shows that climate-conscious energy and building dominate Africa’s use of green bond financing with 47 percent and 39 percent, respectively, of the market share. The “Others” category, where nearly a tenth of the funding is directed, constitutes projects like low-carbon transportation, resource conservation, and waste management.

Figure 4. Composition of green bond issuance by country (left) and by sector (right)

Source: George Marbuah, Stockholm Sustainable Finance Centre, “Scoping the Sustainable Finance Landscape in Africa: The Case of Green Bonds,” 2020.

Given the increasing consciousness of stakeholders—namely governments, agencies, municipalities, multinational development banks, and corporations—to the funding capacity of green financial products and with a multitude of new issuances in the pipeline, the author maintains a positive outlook on the nascent green bond market in Africa and its potential to accelerate achievement of the Sustainable Development Goals across the continent.

For more on building green economies in Africa, read the Foresight Africa 2021 viewpoint, “Recipe for a green recovery: Carbon taxes.” For more on sustainable and green finance in Africa, read “Sustainable financing for economic development: Mobilizing Africa’s resources” and “Approaches for better resource mobilization to finance Africa’s Sustainable Development Goals.”

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Africa’s green bond market trails behind other regions

March 26, 2021