This month, the Africa Growth Initiative at Brookings published a policy brief examining trends in illicit financial flows (IFFs) from Africa between 1980 and 2018, which are estimated to total approximately $1.3 trillion. A serious detriment to financial and economic development on the continent, illicit financial flows are defined as “the illegal movement of money or capital from one country to another” by the research nonprofit Global Financial Integrity. Among other methods, the report looks at one way perpetrators wrongfully funnel resources out of African economies: trade misinvoicing, or the purposeful false reporting of the cost and quantity of commodities.

The losses caused by illicit flows significantly contribute to the constriction of economic growth, as they result in fewer available resources for local economic and social investments. Illicit financial flows also exacerbate risk and uncertainty, thus disincentivizing private investment and widening wealth gaps between elites and those living in poverty.

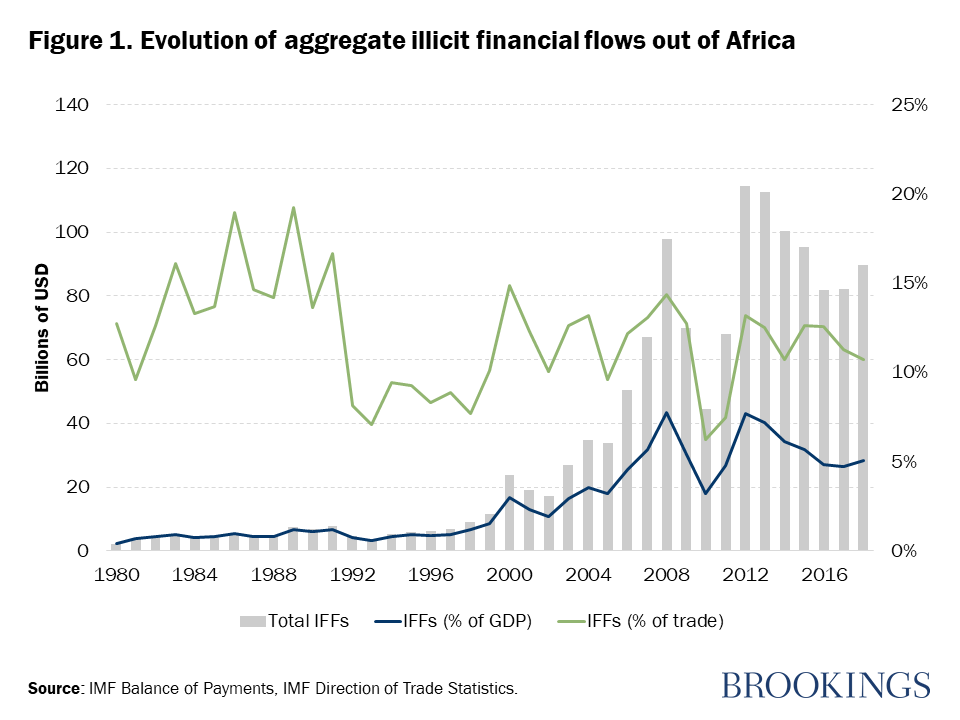

In the brief, the authors show that, over the last four decades, billions of dollars have left the African continent, although the share of IFFs as a proportion of GDP and trade has not seen the same dramatic increase (Figure 1). Indeed, total IFFs peaked in 2012, but IFFs as a percentage of GDP have remained relatively stagnant since 2004, following two decades of gradual increase. Meanwhile, IFFs relative to trade have fluctuated over time, but have generally declined. Notably, the authors posit that the sharp upturn in IFFs in the 2000s is a result of Africa’s greater involvement in global trade as further opportunities for fraud began to emerge.

The report examines other trends in IFFs coming from Africa, noting that several nations and sectors tend to contribute disproportionately to illicit financial flows. In particular, the oil extraction and mining industries are particularly vulnerable to financial flow discrepancies, and four of the continent’s prominent economies—South Africa, the Democratic Republic of the Congo, Ethiopia, and Nigeria—are responsible for more than half the IFFs on the continent. Notably, smaller countries, like Sierra Leone and São Tomé and Príncipe, demonstrate the highest reported levels of IFFs relative to trade.

As IFFs have shifted from more industrialized economies to emerging ones, further efforts to limit illicit outflows prove necessary in order to curb the loss of domestic financial resources. According to the policy brief’s authors, effective policy agreements with key trade partners in Asia and the Middle East can aid in the prevention and mitigation of IFFs, and repatriation efforts for illicit funds from all trade partners will continue to provide an avenue to return outflows to the origin economy. Ultimately, say the authors, these efforts must exist alongside robust preventative measures to inhibit illicit financial flows at their origin.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figure of the week: Illicit financial flows in Africa remain high, but constant as a share of GDP

March 5, 2020