Editor’s Note: The U.S.-Africa Leaders Summit blog series is a collection of posts discussing efforts to strengthen ties between the United States and Africa ahead of the first continent-wide summit. On August 4, Brookings will host “The Game Has Changed: The New Landscape for Innovation and Business in Africa,” at which these themes and more will be explored by prominent experts. Click here to register for the event.

On the second day of President Obama’s three-day U.S.-Africa Leaders’ Summit, the U.S. Department of Commerce and Bloomberg Philanthropies will convene the inaugural U.S.-Africa Business Forum. This event represents an unprecedented occasion for U.S. and African heads of state to meet with business leaders and discuss ways of catalyzing new, continent-wide trade and investment opportunities.

As the summit draws closer, the Brookings Institution’s Africa Growth Initiative (AGI) has reviewed and compared economic relations between sub-Saharan African countries and some of their major commercial partners: the U.S., China, the European Union (EU) and Japan. In this second installment of the Africa Leaders Summit series, AGI examines the trends of U.S. foreign direct investment in the region and proposes potential topics of focus for the forum, to help inform the participants on the key investment issues.

Foreign Direct Investment in Sub-Saharan Africa: Trends and Highlights

FDI to sub-Saharan Africa has increased substantially, in part driven by China, but remains low compared to other regions.

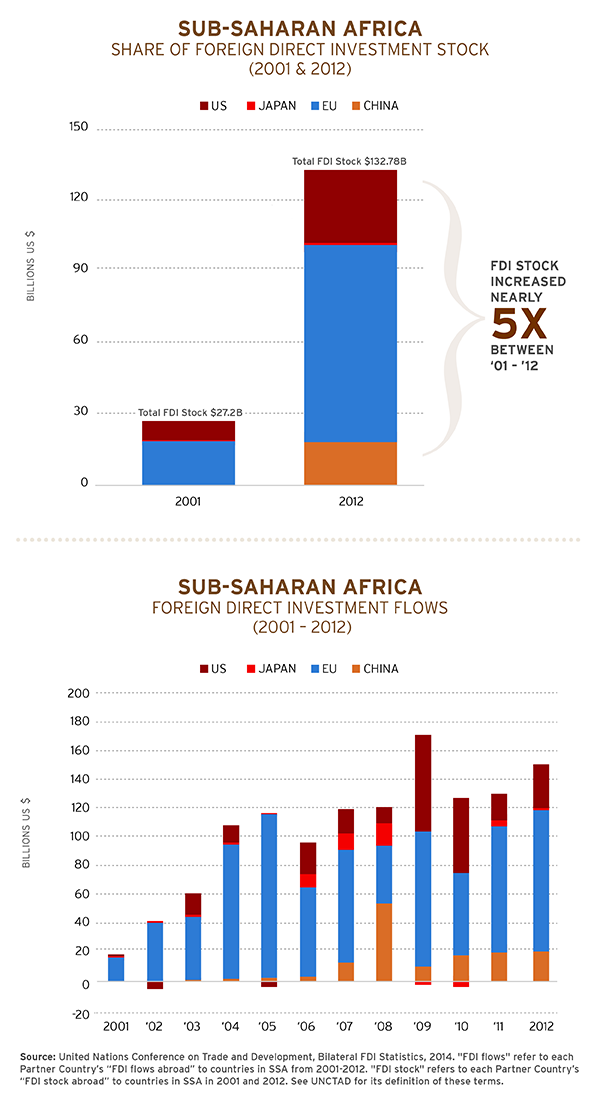

Since 2000, global FDI stock in sub-Saharan Africa has increased dramatically, from over $33.5 billion to $246.4 billion in 2012. According to analysis of UNCTAD’s Bilateral FDI Statistics (2014) [1], the EU, China, Japan and the U.S accounted for approximately 54 percent of the stock of FDI in the region in 2012. South-South investment was also important and included partners such as South Africa (9 percent), Singapore (6 percent), India (5 percent) and Mauritius (5 percent).

The stock of FDI in sub-Saharan Africa from the EU, China, Japan and the U.S. grew by nearly five times between 2001 and 2012, from $27.2 billion to about $132.8 billion. This growth was primarily driven by China, whose FDI grew at an annual rate of 53 percent, compared with 29 percent for Japan, 16 percent for the EU and 14 percent for the U.S. China’s stock in SSA amounted to $18.191 billion in 2012.

Five EU member countries —France (38 percent), the U.K. (31 percent), Germany (8 percent), Belgium (8 percent)—accounted for over 80 percent of the EU’s share of FDI stock in the region. While the EU is considered the largest of the four partners in terms of FDI stock, when the EU is disaggregated by country, the U.S. and France were the largest sources of FDI stock for sub-Saharan Africa in 2012 at $31 billion each, followed by the U.K. with $25 billion. Yet, even though the U.S. is one of the top contributors of FDI stock to sub-Saharan Africa, less than 1 percent (0.7 percent) of the U.S.’s global FDI stock abroad is destined for the region. The U.S primarily invests its $367 billion of FDI in Europe (55 percent), Latin America (13 percent), Canada (8 percent), and other developed countries such as Australia, New Zealand, Israel and Japan (13 percent collectively). Similarly, the EU and Japan direct only 0.8 and 0.2 percent of their FDI, respectively, toward sub-Saharan African countries abroad. China, on the other hand, invested 3.4 percent of its FDI stock abroad in the region in 2012.

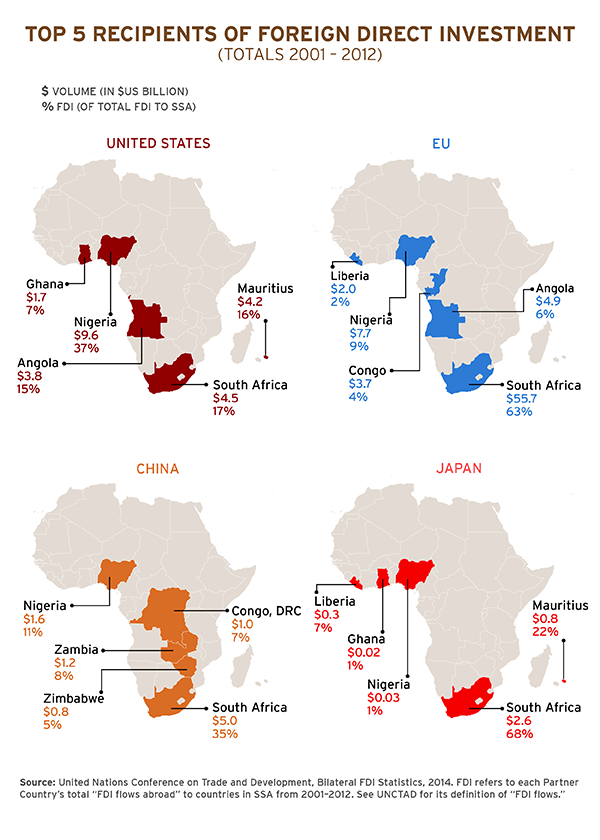

FDI flows to sub-Saharan Africa are highly concentrated in only a few countries; South Africa and Nigeria are the top recipients of sub-Saharan Africa-bound FDI flows for China, the EU and the U.S. The top destinations for U.S. FDI flows in the region are Nigeria (37 percent), followed by South Africa (17 percent) and Mauritius (16 percent). For the EU, South Africa comprises 68 percent of its FDI flows to sub-Saharan Africa while for China, South Africa receives 35 percent of its flows. For Japan, South Africa is also the top recipient (with 68 percent of flows), but Mauritius (22 percent) and Liberia (7 percent) each receive sizable shares as well.

Predominantly resource-rich countries—South Africa with its precious metals and minerals as well as Nigeria with its oil reserves—receive a majority of FDI, indicating that natural resources remain a significant factor in attracting investors to the continent. For example, the main sectors in which the U.S. and China both invested in sub-Saharan Africa were the mining and extractive industries, comprising approximately 58 percent and 30.6 percent of each country’s FDI stock to the region, respectively, in 2011. [2] However, financial services, manufacturing and construction also received notable shares of FDI stock from both countries. China’s reported FDI composition was more diversified than the composition of U.S. FDI, with 19.5 percent in financial services, 16.4 percent in construction, 15.3 percent in manufacturing, and the remaining 18.2 percent in business and tech services, geological prospecting, wholesale retail, agriculture and real estate. U.S. FDI was concentrated 12 percent in finance and insurance, 5 percent in manufacturing and 25 percent in other industries. Despite this emphasis on mining and extractive industries in 2012, according to the World Investment Report of 2014, international investors are increasingly looking to new opportunities in consumer-oriented sectors (such as information technology, foods, financial services and wholesale retail) that target the region’s expanding middle class.

Investors’ Pledge for Good Governance in Sub-Saharan Africa

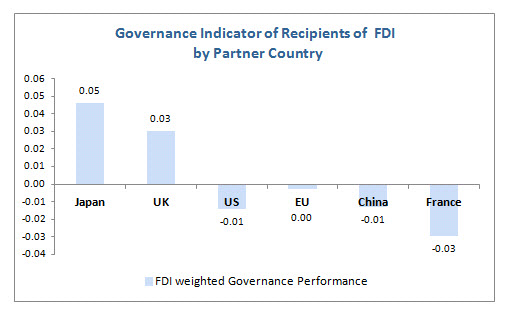

Along with the appetite for mineral resources, energy and other returns that drew massive investment into Africa, we compared the status of the quality of governance in the countries where the U.S., Japan, the EU and China invested in 2012.

Investing in countries with relatively higher governance performance can reflect at least three concerns: (i) the investors’ level of risk aversion, (ii) the pursuit of democratic principles or non-ideological relationship based on non-interference, and (iii) the level of pressure from global consumers, who are increasingly scrutinizing their choices along the global value chains according to the respect of governance indicators, such as respect for human rights.

We used the World Governance Indicators [3] in 2012 produced by Kaufman, Kraay and Mastruzzi, which cover six dimensions of governance: voice accountability, rule of law, government effectiveness, political stability, regulatory quality, and control of corruption. The governance index ranges from -2.5 (weak) to 2.5 (strong governance performance). In 2012, Botswana and Mauritius top the list with a score of governance performance of 0.71 and 0.66 respectively, while Zimbabwe and the Democratic Republic of the Congo (DRC) are at the bottom with a respective score of -1.35 and -1.74.

Our computed levels of average governance indicators (weighted by the share of total FDI flows in the host countries between 2001 and 2012) are comparable across the EU, U.S. and China. Japan’s investment is concentrated in South Africa where the overall governance performance is high. When we disaggregated the EU by individual member countries, France has the largest share of investment in countries with the lowest levels of governance.

Given its focus on oil-producing countries with low governance levels, the U.S. is comparable to other regions. Importantly, however, the U.S. Dodd-Frank Act, requires public disclosure of payments at the project level from listed companies, involved in extractive industries. Other initiatives require companies to eliminate conflict minerals from their supply chains. For instance, the use of coltan originating from the DRC and neighboring countries is effectively banned. UNCTAD data actually show no record of U.S. investment stock in the DRC from 2007 onwards. The EU has a similar set of policies manifested in its Accounting and Transparency Directives. Furthermore, the U.S., along with China, the EU and Japan, is a participant in the Kimberley Process, which has banned the sale of “blood diamonds.” Other transparency initiatives supported by the U.S. include the Extractive Industries Transparency Initiative (EITI), the International Tropical Timber Organization (ITTO) and the International Chamber of Commerce (ICC) Rules on Combating Corruption. [4]

Engagement through Bilateral Investment Treaties

Bilateral investment treaties (BITs) are agreements signed between countries aiming to promote FDI by ensuring certain guarantees [5]—against expropriation, for example—for investors in unstable business environments. BITs are low-cost options to encourage business climate reform while simultaneously signaling investor commitment to host countries and providing them with policy space to design and implement their development agendas. These BITs and other international investment arrangements (IIAs) have proliferated widely over the past 50 years: the total number of BITs globally reached 2,902 [6] in 2013 with the number of sub-Saharan Africa-specific BITs comprising at least 300 of these treaties.

Among sub-Saharan Africa’s partners there is significant variation in the number and distribution of BITs with the continent. China has BITs with 27 sub-Saharan African countries [7], signing 10 in the past 10 years.[8] For the EU, member countries negotiate BITs bilaterally, and France has 18 in sub-Saharan Africa, the U.K. has 21 and Germany has 39. The U.S. has six, and Japan has only one. So why is the U.S. so far behind in the number of BITs it has enacted?

According to Benjamin Leo from the Center for Global Development, it is in part due to the U.S.’s limited “negotiating capacity”—it has only a few foreign commercial officers on the ground to negotiate these treaties, whereas the EU and China have distributed delegations of commercial attachés at offices and embassies in nearly all African countries. The U.S. has also focused its efforts on establishing trade and investment framework agreements (TIFAs) in the region, which provide a forum for engaging in discussions on trade and investment, but do not confer protections on investors or indicate a serious commitment to host countries since they are not legally binding. Furthermore, the U.S. Model BIT, which it uses in its negotiations, is a very dense and complicated legal document, which is difficult for many countries to review and discuss without adequate legal support (that some of them lack). These compounding factors hinder the U.S. from establishing mutually beneficial investment agreements with countries in sub-Saharan Africa.

Policy Recommendations

There is ample scope to expand the U.S.’s investment strategy with Africa. The U.S. funnels less than 1 percent of its FDI abroad toward the region, and it invests largely in only a few countries and sectors. While the perceived risks of investing in Africa have historically been high, rates of return have also proven to be high, averaging 11.4 percent on inward FDI for the period 2006-2011 (compared with 5 percent for developed countries) [9]. UNCTAD’s World Investment Report 2013 also reported that four of the top 20 economies with the highest rates of return on inward FDI in 2011 were in sub-Saharan Africa.

- One way in which the U.S. can increase FDI to sub-Saharan Africa is through the promotion of BITs. African countries are seriously engaging in the negotiation of BITs: Among the most active countries at concluding BITs (globally, in 2013) were Mauritius and Tanzania, which each concluded three BITs. The U.S. should reciprocate this engagement by focusing its efforts on implementing sustainable-development-oriented, legally-binding BITs [10] rather than TIFAs; providing technical assistance to reform business environments and reduce the cost of doing business; and establishing BITs with strategic countries like Nigeria. With China and the EU continuing to sign BITs, the U.S. risks being “locked out” of certain markets or industries.

- So-called “blended initiatives,” such as Power Africa, offer another useful model to increase investment through partnerships between the African private sector, U.S. government agencies, African governments, and other partners like multilateral institutions such as the African Development Bank.

At the same time, African policymakers should engage the U.S. authorities and its private sector to:

- Get more transfer of knowledge and skills from FDI. For example, policymakers can provide incentives for investors to include local businesses in the value chain and invest in education and training;

- Reduce illicit financial flows from tax evasion, the underpricing of concessions and trade mispricing; and

- Strengthen African common institutions. For instance, the NEPAD-OECD Africa Investment Initiative aims to raise the profile of Africa as an investment destination while facilitating regional cooperation and has led to a number of investment policy reviews in four South African Development Community countries (Mozambique, Botswana, Tanzania and Mauritius).

[1] The FDI data were collected from UNCTAD’s publically available Bilateral Investment Statistics database, 2014, which provides bilateral, geographically disaggregated data on stocks and flows from 2001-2012. Our analysis specifically focused on outward FDI or FDI abroad, originating from our selected partners and destined for sub-Saharan African countries. Data on the European Union was aggregated for all EU member countries (at time of accession).

[2] Figures based on Chinese White Paper on Economic Cooperation (2013) and a 2012 CRS paper entitled “U.S. Trade and Investment Relations with sub-Saharan Africa and the African Growth and Opportunity Act.” Data for the EU and Japan were not available.

[3] The Mo Ibrahim Foundation also produces governance performance indices specifically from sub-Saharan African countries that monitor changes in 182 indicators of governance from judicial process independence to equity of access to public services. Their index scores range from 0 to 100, where 100 is the best possible score. Mauritius (83) and Botswana (78) had the strongest governance performance while the Democratic Republic of the Congo (31) and Eritrea (32) had the worst performance.

[4] The U.S. is a candidate country for EITI and is also a supporting government stakeholder in the initiative, but is not yet on record as being an EITI compliant country.

[5] According to the Office of the United States Trade Representative, these include most-favored-nation treatment for investors, protection against expropriation and/or provision of adequate compensation, the right to transfer investment funds using market-based exchange rates, limitations on performance requirements, the authority to choose their top managerial personnel and access to international arbitration to settle investment disputes.

[6] Plus an additional 334 IAAs.

[7] Data on BITs are from UNCTAD’s country-specific list of BITs, however, the Chinese White Paper on Economic Cooperation (2013) states that China has signed more than 30 BITs.

[8] This includes Benin, Chad, the DRC, Equatorial Guinea, Guinea, Madagascar, Mali, Namibia, Seychelles (not yet entered into force) and Uganda.

[9] Figures based on statistics in UNCTAD’s World Investment Report, 2013, p. 33.

[10] Sustainable-development-oriented features include measures explicitly stating that that countries should not take measure to promote investment that would harm health, safety and environmental standards. They also ensure public policy space for host countries and minimize exposure to investment arbitration.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The U.S.-Africa Leaders Summit: A Focus on Foreign Direct Investment

July 11, 2014