The seeming disconnect between consumer sentiment and the state of the macroeconomy has been a defining characteristic of the post-COVID economy. By most widely accepted measures, the state of the macroeconomy is historically robust: The topline unemployment rate has remained below 4% for the past two years, economic growth has been steady and recovered pandemic-era losses, and inflation has retreated to historical norms.

This apparent strength notwithstanding, various measures of household and consumer sentiment suggest a persistent dissatisfaction with the state of the economy. Less than one-quarter of registered voters surveyed by the Wall Street Journal in August 2023 answered that the economy was headed in the right direction. The Michigan Index of Consumer Sentiment is roughly in-line with levels reported during the heart of the Great Recession in 2009, while the share of respondents in a Pew poll with a positive view of the economy was roughly halved between 2016 and today.

Explanations for the gap between sentiment and economic fundamentals

The disconnect between sentiment and macroeconomic performance has given rise to a host of plausible explanations. A subset of these explanations relates to dissatisfaction over the current state of the economy and future economic opportunities. This includes persistently elevated inequality, the higher level of prices owing to elevated post-pandemic inflation, a widespread lack of affordable housing, and a loss in faith about future economic prospects—including concern over the negative impact of artificial intelligence on quality jobs. Yet, this theory of dissatisfaction does not explain why, on the whole, the many positive elements of the macroeconomy do not seem to influence consumer sentiment as much as more limited negative elements.

A second set of explanations ties economic dissatisfaction to non-economic concerns, a phenomena characterized as “referred pain” by Wall Street Journal columnist Greg Ip. Ip suggests non-economic sources of dissatisfaction could include issues such as wars in the Middle East and Ukraine, political and culture conflict, mass shootings, and crime; other plausible factors include growing discrepancy in measures of wellbeing such as life expectancy, social isolation, and marriage. While such a theory is difficult to test, one relevant critique is that such geopolitical and social concerns are not new, and certain concerns—such as crime—are even abating over time.

A third set of explanations relates to economic perception and the influence of negatively biased news sources. One aspect of this theory is heightened political polarization owing to increased consumption of ideologically biased cable news sources, which could lead to both direct dissatisfaction over polarization and indirect dissatisfaction over a biased perception of the state of the economy. A related aspect of this theory is what former White House economists Ryan Cummings and Neale Mahoney call “asymmetric amplification”—the notion that Republicans are relatively sourer on the economy under a Democratic president. In the analysis below, we offer a complementary explanation related to perception: that the tenor of economic news has become systemically more negative over time. A key assumption behind this theory is that a fundamentally more negative economic news tenor will lead U.S. households to perceive the economy to be less robust than it actually is, driving down sentiment in household surveys.

To test this hypothesis, we model the relationship between the sentiment of economic news stories and fundamental economic measurements, such as growth and inflation, to measure the presence of systematic deviation in sentiment away from fundamentals. We refer to such deviations as “tone.” If the sentiment of economic news stories is more positive than expected given fundamentals and prior relationships, the tone is positive. If sentiment is more negative than expected, the tone is negative. Our analysis suggests that over the past six years, tone has shifted more negative, with an increase in the magnitude of negative tone over the past three years.

This explanation is appealing on three fronts. First, a systematic negative bias helps to explain a negative gap between sentiment and macroeconomic indicators that began in 2017 when price levels had not risen sharply, and housing affordability was less of a concern. Second, systematic bias can help explain why Americans appear to wrongly report on the state of the economy. For example, a recent Bankrate survey revealed that approximately six-in-ten respondents described the U.S. economy being in a recession, despite strong quarterly economic growth and a tight labor market. Similarly, a Financial Times survey found large shares of Americans getting basic facts about the economy wrong, including for example 90% incorrectly saying that prices have risen faster than wages over the last year. (This survey shows Americans also wrongly characterize a host of other economic trends, including those related to real wages, wealth accumulation, and poverty.) Third, Americans’ assessments of their local community’s economic circumstances are far more positive than their assessments of the national economy, and they rely on economic reporting more heavily for the latter. All of these mischaracterizations and deviations may be partly attributed to a growing negativity in the tone of economic news. Below, we briefly describe our methodology before quantifying the systemic negative bias that arose six years ago and expanded since 2021.

Modeling the relationship between economic news sentiment and fundamentals

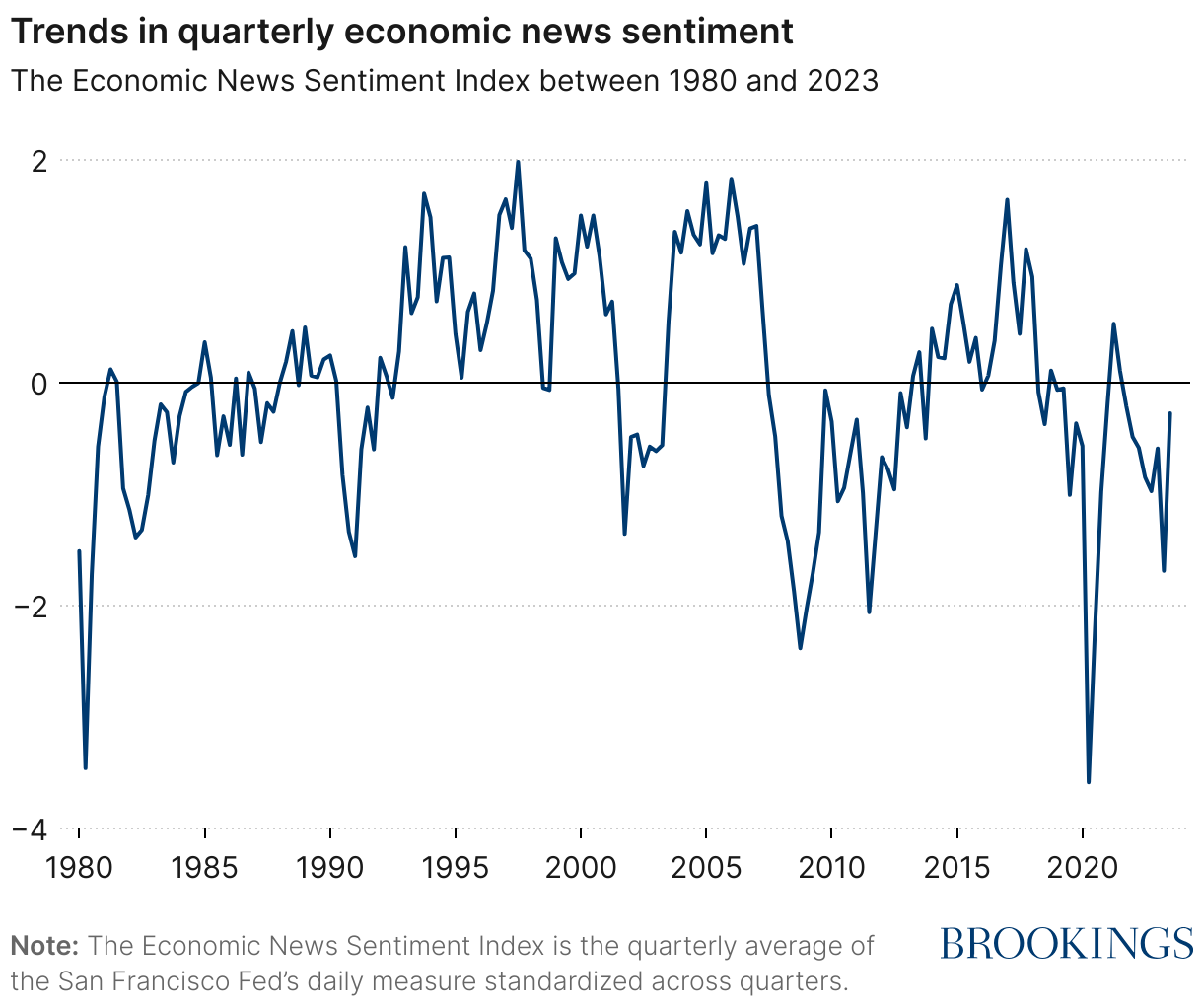

Our analysis models the historical relationship between the sentiment of economic news and macroeconomic fundamentals.1 We measure the sentiment of economic news between January 1980 and September 2023 with the San Francisco Federal Reserve’s Economic News Sentiment Index. This index measures the daily economic news sentiment in a set of two dozen major newspapers from 1980 forward, aggregating and scoring the text of major news articles and editorials that focus on the U.S. economy.

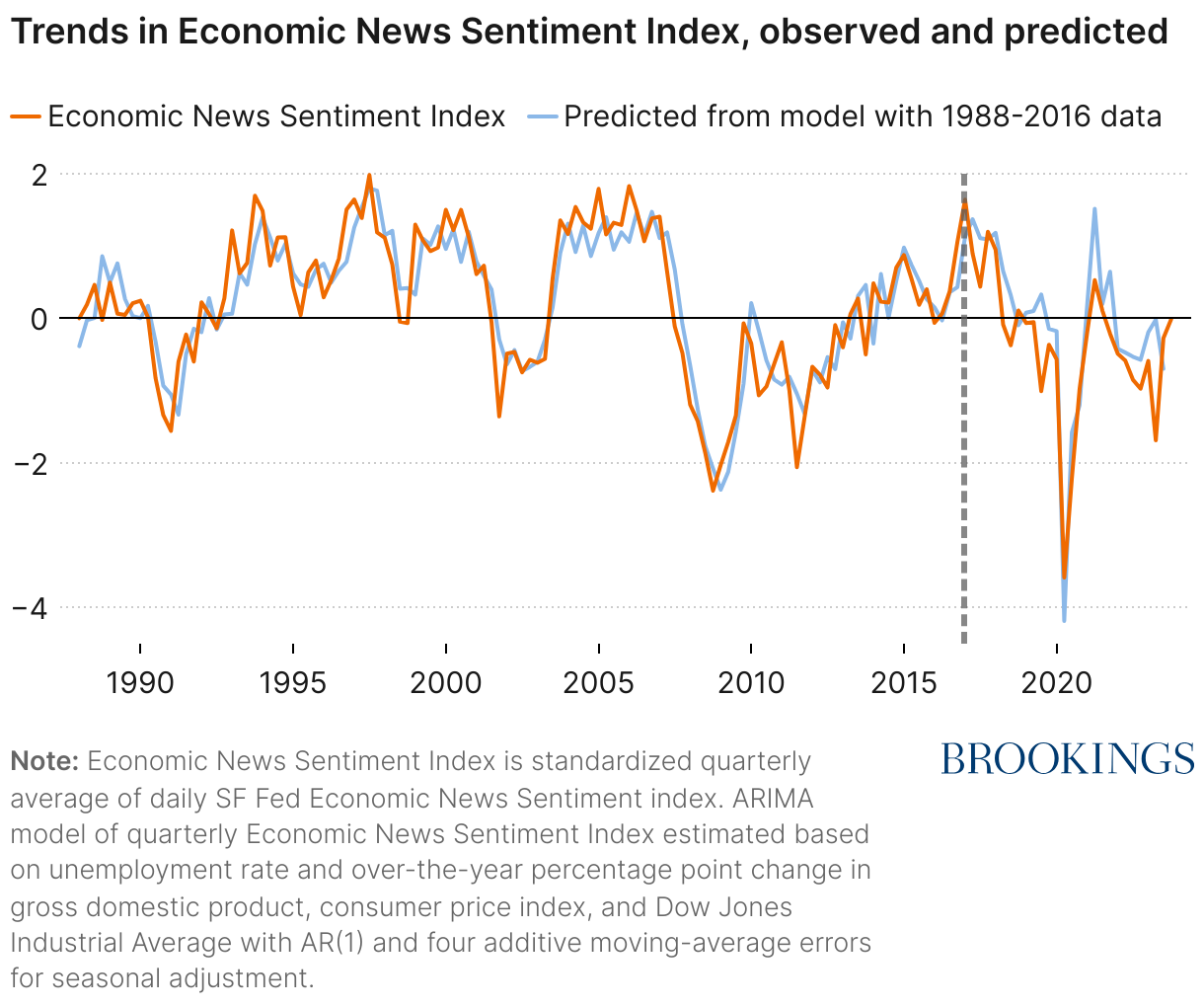

To produce a quarterly measure, we average the Index’s daily measure within each quarter of a calendar year and then standardize the quarterly measures so that it has mean zero and standard deviation of one across quarters. When the index is higher, the sentiment of economic news is more positive; when it is lower, sentiment is more negative. The Index is shown below (see Figure 1), with recent values turning negative—similar to the values observed in the recession of the early 2000s and sluggish recovery following the Great Recession.

To measure whether news sentiment has systematically separated from economic fundamentals, we estimate a regression model predicting the quarterly sentiment index using a set of macroeconomic variables capturing economic growth, unemployment, inflation, and equity prices. Specifically, we use the following four quarterly variables to capture economic fundamentals:

- Gross domestic product (GDP), percentage point change over the year: nominal output for the U.S. economy, Bureau of Economic Analysis.

- Unemployment rate, percent: among people employed or job seeking, the percent who are jobseekers, Bureau of Labor Statistics.

- Consumer prices (CPI), percentage point change over the year: the consumer price index for all urban consumers and all items, a standard measure of consumer price inflation, Bureau of Labor Statistics.

- Equity prices, percentage point change over the year: the Dow Jones Industrial Average, FRED, Federal Reserve Bank of St. Louis.

In the estimation, we use data from a base period of 1988 through 2016, leaving seven years of data to estimate out-of-sample both before and after, and employ an Autoregressive Integrated Moving Average (ARIMA) model that includes an AR(1) autocorrelated error and four lagged moving-average terms to capture seasonality. We can use the model’s estimated parameters to predict sentiment in any quarter given data on the economic fundamentals of that quarter and four quarters prior. This approach allows us to predict the level of news sentiment that is expected given current economic fundamentals and to measure whether tone (the gap between observed and expected sentiment) has become more negative in recent years. While some may object that the model omits important predictors, we note that the model yields essentially identical results under several robustness checks—including employing alternative measures of equity prices or adding real disposable personal income as a predictor. Ultimately, we believe this simple analytic framework provides a structured approach to measuring a systematic shift in the tone of economic news conditional on fundamentals.

Measuring whether the sentiment of economic news has become systematically more negative

Estimates from the regression model during the base period indicate that the relationship between economic news sentiment and economic fundamentals follows an expected pattern: News sentiment tends to be more positive when the unemployment rate is lower, when consumer price inflation is slower, when the economy is quickly expanding, and when stock prices are rising faster.2

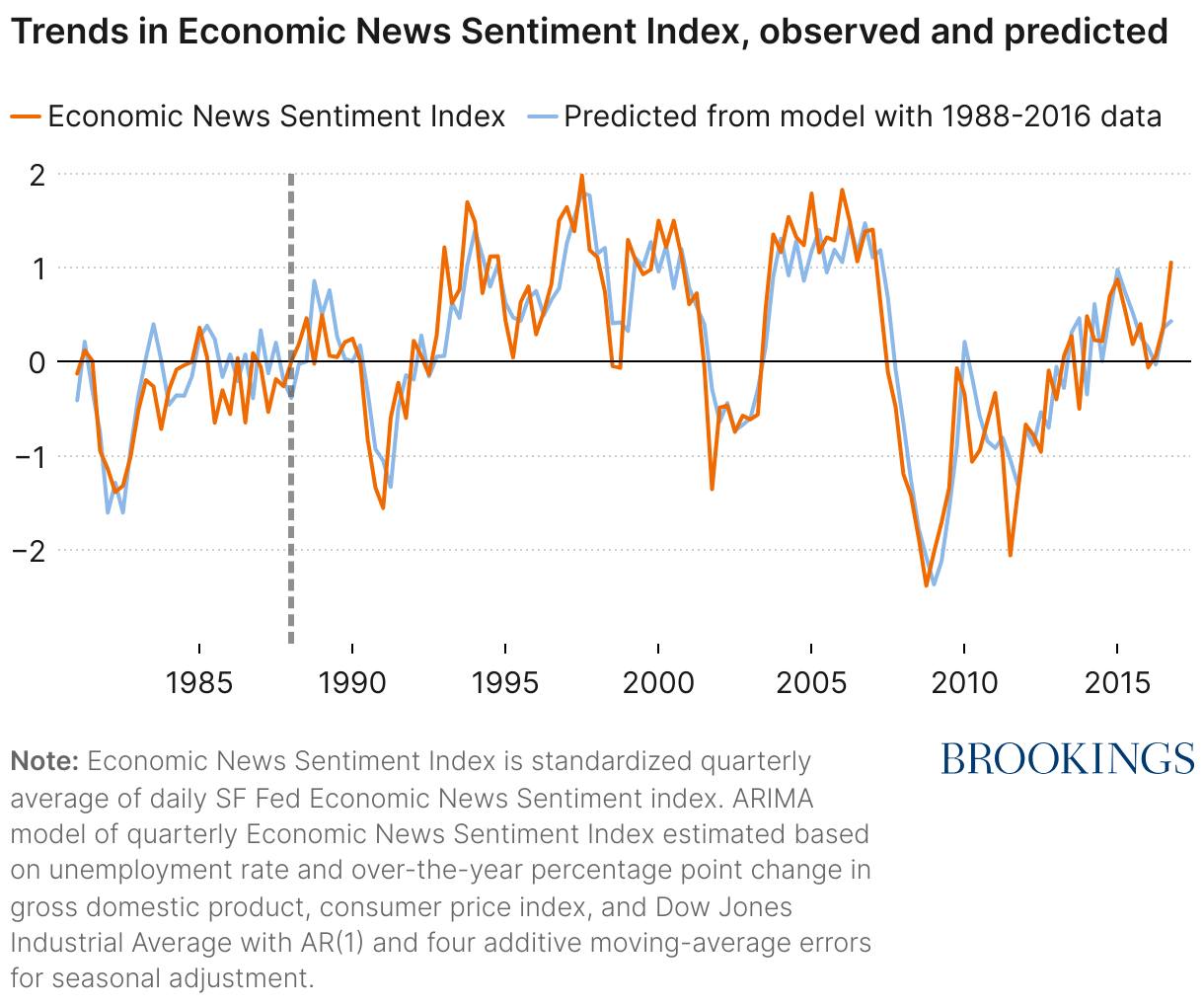

The model performs well with in-sample economic news tone prediction during the 1988-2016 base period (see Figure 2 below). Gaps between observed and predicted sentiment tend to be small, suggesting that this parsimonious set of fundamentals does a very good job predicting news sentiment over these years. When the gap is positive (orange above blue), observed sentiment is above predicted sentiment, so the sentiment of the news is more positive than expected given the fundamentals and we say that the tone of economic news is positive. When blue is above orange, sentiment is more negative than expected so the tone is negative. By construction, for the base period, gaps are positive and negative in about equal measure (in other words, no bias in tone on average).

We can also measure how well the model performs at prediction in periods outside of the base period used to estimate the model parameters. In this kind of out-of-sample prediction task, there is no guarantee that gaps will average to zero. In such a period, we can conclude whether or not the sentiment of coverage is following fundamentals like it was during the base period. We started the base period in 1988 (Figure 2: right of dotted vertical line) so that we could test the model in the prior seven years from 1981 through 1987 (left of vertical line). Here, the model performs very well in predicting news tone. The gaps are a bit larger, but they still look to average about zero, amounting to -0.11 on average. This provides some assurance that the model is not just fitting noise.

We now turn to testing the main question: Has the sentiment of economic news been more negative lately given the fundamentals? Does recent economic news bias more negative than fundamentals would predict based on 1988 to 2016 relationships?

As shown in Figure 3, we use the same base-period (left of dotted vertical line) model and parameters but predict out-of-sample for 2017 to the present (right of line). Over this period, the model again performs well. In particular, it closely matches the COVID-recession dip in news sentiment. But observed sentiment (orange) appears to be systematically below predicted sentiment, evidence of more negative news sentiment than expected from fundamentals (i.e., negative tone). While the gaps averaged -0.11 in the pre-base out-of-sample period, they average -0.33 in the post-base out-of-sample period.3

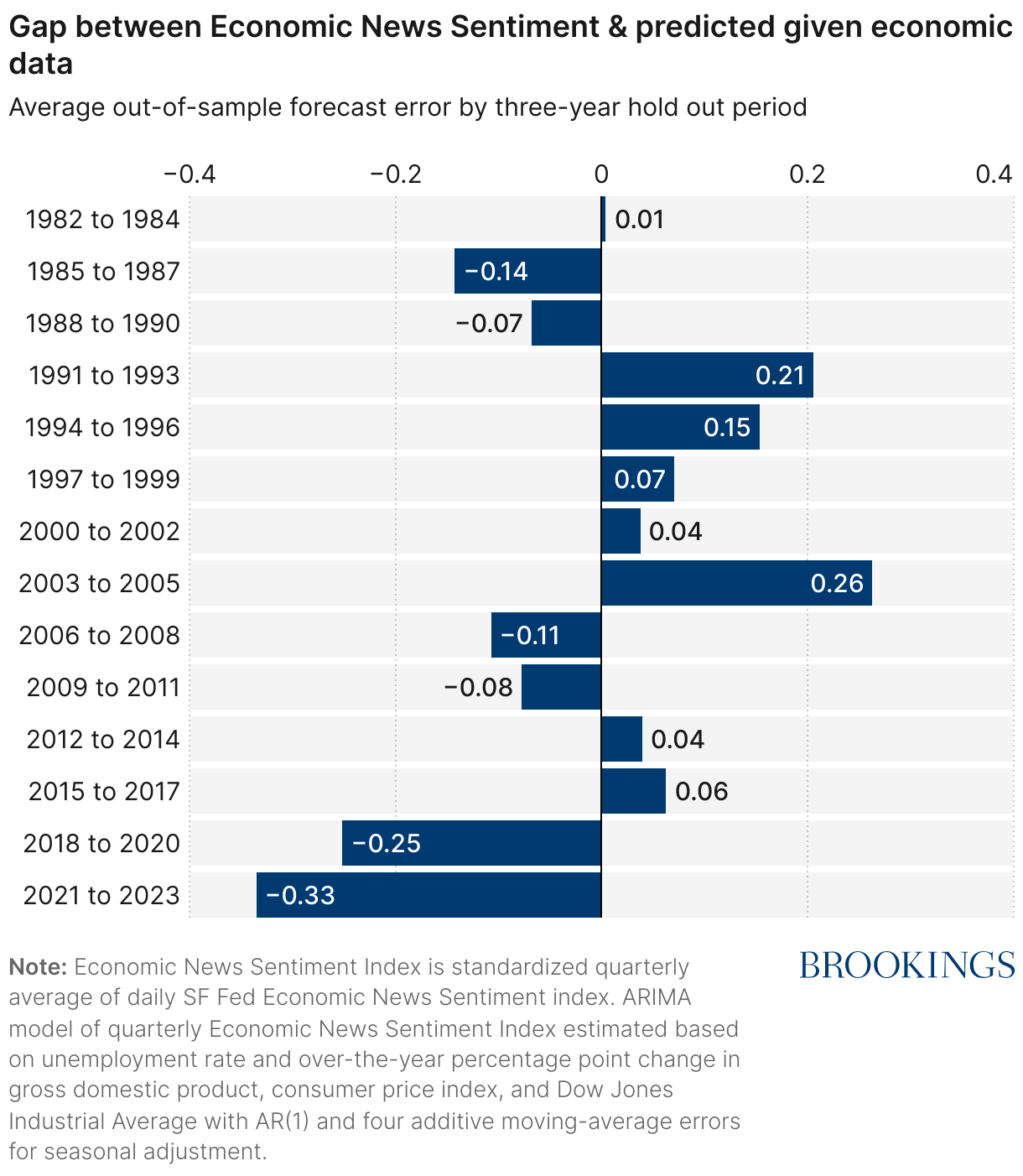

To quantify the gap between observed and predicted news tone in a different way, we estimate a series of models each time holding out a different three-year period from the estimation sample. Then, each estimated model is used to predict out-of-sample for economic news tone for the hold-out period. Figure 4 below describes the average tone for each hold-out period. For most periods, models using other periods’ data reasonably predict sentiment in that period.

However, the news tone has been more negative than the fundamentals would predict during 2018 to 2020 and even more negative than predicted in 2021 to 2023. Looking at gaps by year shows that the recent negativity seems to have started pre-pandemic in 2018. But the “negativity gap” spanning 2021 to 2023 is about one-third larger than in the prior three-year period.

In sum, the discrepancy between the macroeconomy and household sentiment has given rise to several competing theories to explain the apparent disconnect. Our simple econometric model adds to evidence that biased sources of information play a role, and suggests that economic news has become systemically more negative beginning in 2018, with the negative bias growing over the past three years. To be clear, this analysis shows that the conditional tone of news is becoming more negative over time, but requires assumptions about how this increased negativity affects sentiment—including in particular the role of systematic bias in driving inaccurate perceptions about U.S. economic performance. While this new relationship may not explain the entire sentiment puzzle, it presents novel explanations for why consumer sentiment appears to be divorced from the macroeconomy and why survey respondents inaccurately describe the U.S. economy to be in a recession.

Authors

-

Acknowledgements and disclosures

The authors thank Carol Graham for helpful comments and Stephanie Holzbauer and Chris Miller for assistance preparing the document.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

-

Footnotes

- For further details on the construction of the Index, see Adam Hale Shapiro, Moritz Sudhof, and Daniel Wilson, “Measuring News Sentiment,” Federal Reserve Bank of San Francisco Working Paper 2017-01, March 2020, https://doi.org/10.24148/wp2017-01 and https://www.frbsf.org/economic-research/indicators-data/daily-news-sentiment-index.

- All factors are statistically significant with 95% confidence. Regression results are available from the authors upon request.

- Note that p=0.08 for the null hypothesis that average gaps are pre- and post-base are equal.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).