The “One Big Beautiful Bill Act” of 2025 (OBBBA), like the Tax Cuts and Jobs Act (TCJA) of 2017, became law despite polling that showed many Americans viewed it unfavorably. This pattern is not unique to tax legislation: Counter to public preferences, there has been a lack of legislation on gun safety, and there have been new restrictions on reproductive health care. In the case of tax laws, the fiscal stakes are especially high. OBBBA’s provisions are projected to add trillions to the federal deficit over the next decade and reshape major federal tax and spending programs.

Understanding why major tax legislation can diverge from public preferences helps identify how to close the gap between what lawmakers enact and what the public supports, all while improving the nation’s fiscal outlook over the long term.

What the polling says

Among its many provisions, OBBBA made permanent the TCJA’s tax cuts, allocated funds for immigration control, and substantially cut Medicaid and food stamps. In June, before OBBBA was enacted, a Washington Post-Ipsos poll revealed that 42% of respondents opposed OBBBA while only 23% supported it. About one-third of respondents had no opinion, which suggests they had little knowledge of the bill’s provisions.

This raises broader concerns about how little substantive information about tax legislation reaches—or resonates—with the public. Among those who were aware of the legislation, opposition rose to 64%.

A Wall Street Journal poll taken after enactment found that 70% of respondents believe that OBBBA tax cuts will help the wealthy and over half say the legislation will be detrimental to social programs. Research supports those views.

But some public preferences carry more weight

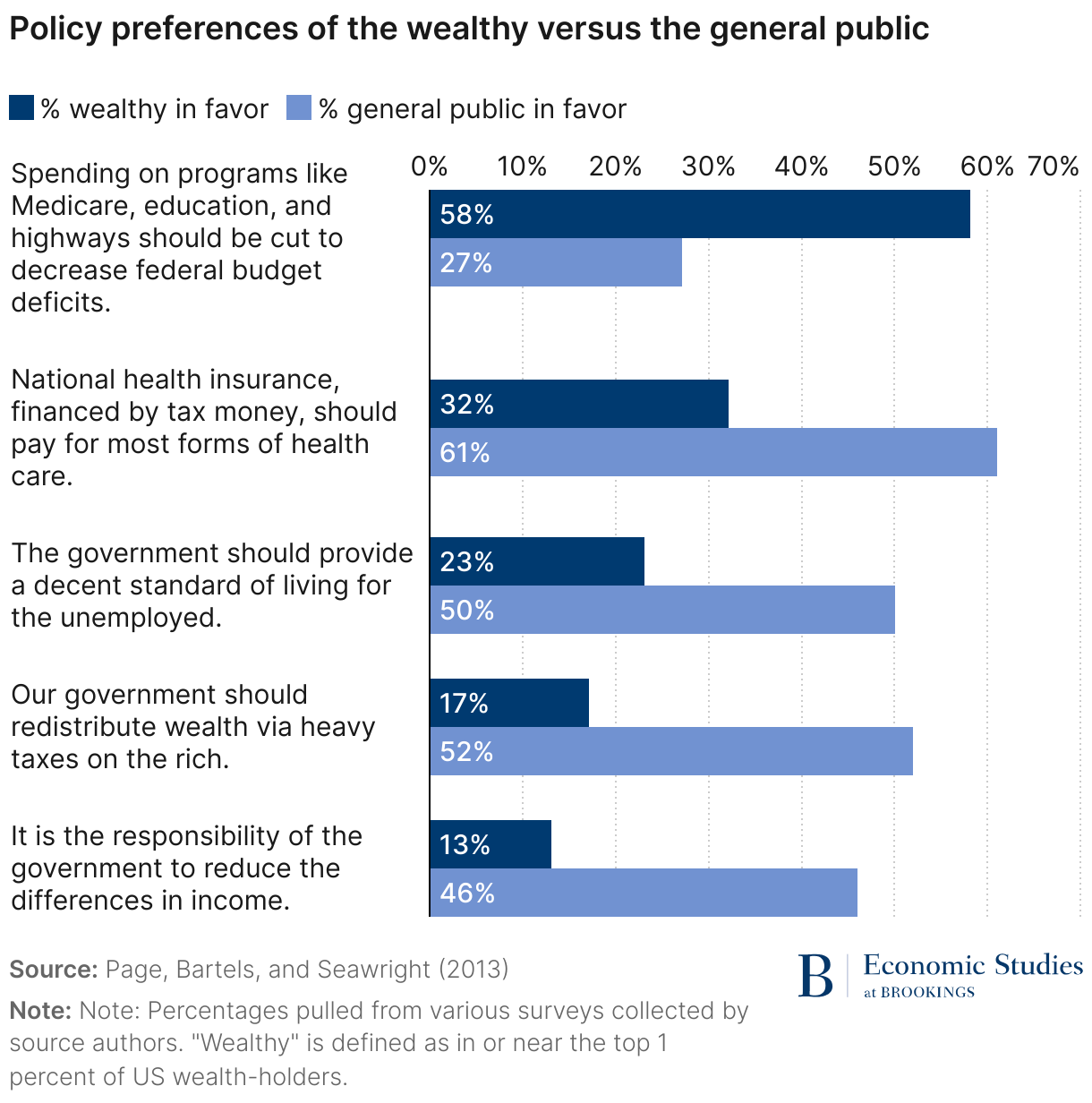

The divergence between public opinion and legislation has deep roots. Scholars have confirmed that legislative outcomes tend to reflect the preferences of wealthy citizens. As shown in Figure 1, the preferences of the wealthy and the general public often differ sharply, with more affluent individuals generally backing less spending on social programs and lower taxes on the wealthy. Enacted legislation often reflects these positions, and recent research confirms that these gaps remain persistent.

One plausible explanation for this phenomenon is that affluent individuals can afford to be more politically engaged and informed. They are more likely to call their elected representatives and, importantly, donate to re-election campaigns. During the 2024 election cycle, super PACs (political action committees) and billionaires outspent small donors, giving a record-setting $2.7 billion to candidates and major parties. Another explanation is that much of the public may lack sufficient awareness about fiscal legislation, as the polling on OBBBA suggests.

Policymakers seeking to better align legislation with public preferences have choices

First, they could expand programs that generate public funding for campaigns. Connecticut serves as a model with its successful Citizens Elections Program (CEP). First implemented in 2008, CEP dramatically decreased big-dollar influence in campaigns. By 2018, 99% of state legislative campaign financing came from individual donations, and winning candidates accepted 98% less money from private interest groups, on average.

Common Cause reports that this shift produced policies that are more responsive to the general public, and many voters express that public financing is producing better governance. Such programs can help align policymaking with public opinion and thus merit national consideration.

Second, policymakers could frame fiscal issues in ways that connect directly to voters’ priorities. Evidence shows that support for progressive tax policies rises when survey questions are framed around facts on tax fundamentals, emphasize the benefits of taxation, and draw connections to spending considerations. This effect is strongest when that connection is emphasized in polling questions, tax forms, or even ballots.

Kansas provides an instructive example. The state cut taxes in 2012, leading to reduced funding for education and infrastructure. By 2017, public dissatisfaction with those spending cuts led the Republican-controlled legislature to reverse course and raise taxes. This underscores the importance of linking abstract fiscal policy to tangible outcomes. Framing tax debates around their real-world consequences—in surveys and other outreach methods—could help voters evaluate tax proposals more fully and make more informed decisions at the ballot box. In turn, this clarity has the potential to decrease the volatility of policy changes and stabilize tax policy decisions.

Public spending depends on taxes

Taxes and spending are inextricably linked, and voters’ understanding of that connection could shape policy outcomes. While many people support tax cuts in isolation, support declines when the trade-offs—like higher debt or cuts to Social Security and other welfare programs—are made explicit.

The passage of OBBBA marks yet another instance of tax legislation out of step with public preferences and the country’s needs. Closing this gap will be neither quick nor easy, but it is essential for the health of our democracy and for sound fiscal policy.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

When tax laws defy public opinion: What OBBBA reveals

August 19, 2025