Many economies are still reeling from the global financial crisis. Now, at least, there is some emerging clarity about how the crisis changed the global economy, and what countries should do to protect themselves from future shocks.

It is too early to tell whether the global crisis will permanently lower global growth. But clearly, the global economic landscape has changed substantially since the crisis. An important question is whether vulnerability and adjustment to shocks has also changed fundamentally.

This is key for developing Asia, which is deeply integrated with the world economy but generally lacks the policies and institutions to cope with shocks.

Recent research on the relationship between volatility and GDP growth suggests that country-level growth since the crisis is more dependent on external factors, including global growth, oil prices, and financial volatility. Econometric analysis indicates that the effect of global GDP growth on national GDP growth jumped by 85 percent since the crisis. One possible reason for this is that the global financial crisis deprived the world economy of its traditional anchor and source of stability—the United States.

This has made the global landscape more volatile, leaving individual economies more vulnerable to external shocks. Moreover, despite the slowdown of global trade since the crisis, there is evidence that growth spillovers from trade partners are significant determinants of a country’s growth.

The evidence suggests that a recession at a major trading partner now has bigger repercussions. The spillover effect of a downturn was zero before the crisis, but turned positive post-crisis. One explanation for this is the reduction of monetary and fiscal policy flexibility caused by the global financial crisis, which has left countries with fewer tools to mitigate external shocks.

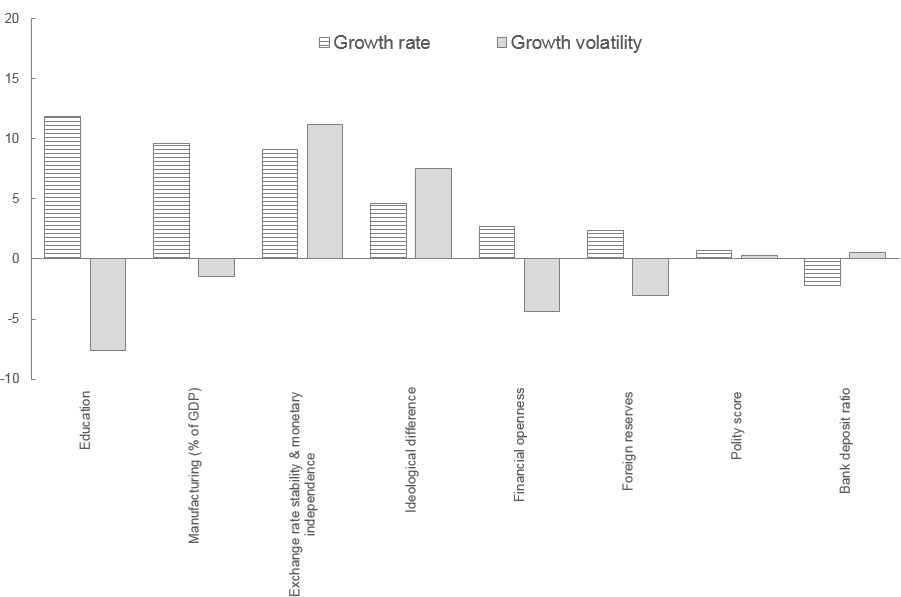

For middle-income countries, including most of developing Asia, several factors help countries adjust to shocks. Specifically, economic growth is buoyed if a country prioritizes advanced education, has a greater share of manufacturing output in GDP, and stable exchange rates (Figure 1).

Figure 1: Correlations of shock-adjusted growth and volatility with fundamental and institutional factors in middle-income countries

This finding confirms the key role of human capital and a skilled workforce in sustaining rapid growth in middle-income countries. At low income, an abundant pool of unskilled workers can power economic growth, as China’s experience shows. But as an economy shifts to middle income, knowledge and skills come to the fore.

The study finds that a strong manufacturing sector is crucial for growth, especially in middle-income countries. This belies the notion that information and communications technology (ICT) makes it possible for countries with an excellent ICT sector, like India, to bypass manufacturing and leapfrog from agriculture directly to services.

Lower political polarization, greater exchange rate flexibility, and higher educational attainment also mitigate volatility. Political instability increases uncertainty for both firms and households. This can, in turn, lead to more volatile behavior, which translates into growth that is more volatile. For example, firms might change their investment plans abruptly in response to new political developments in a highly charged political environment.

Another key ingredient of economic stability is the availability of skilled workers. They can adapt more smoothly than unskilled workers can to new technologies and other jarring changes. Among all ingredients of economic growth, education was the most positively related to the level of growth, and an important factor as well in the volatility of a country’s growth trajectory. Adaptable and versatile workers not only help an economy to grow faster but also absorb shocks, resulting in less volatile growth.

Flexible exchange rates can also act as a shock absorber, helping an economy to adjust by weakening the currency and boosting exports. Stable exchange rates, on the other hand, foster faster growth overall. This dichotomy makes exchange rate management more of an art than a science, as a balance is required between shock-mitigating flexibility and growth-promoting stability.

This is certainly the experience of most middle-income countries that made a relatively quick transition to high income, such as South Korea. As well as maintaining competitive but flexible exchange rates, those countries invested heavily in education and developed vibrant export-oriented manufacturing sectors.

In an uncertain global economic environment, the message—especially for middle-income countries in the developing world—is clear: To withstand external shocks and sustain growth, they need to get the basics right on manufacturing, currency management, and above all on education.

Joshua Aizenman is professor of international relations and economics at University of Southern California. Gemma Estrada is senior economics officer, Donghyun Park is principal economist, and Shu Tian is economist at the Economic Research and Regional Cooperation Department of the Asian Development Bank. Yothin Jinjarak is associate professor, School of Economics and Finance, Victoria University of Wellington.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The global financial crisis and middle-income countries

October 27, 2017