A year ago, someone—that would be me—wrote that 2014 was the year that the federal budget deficit largely disappeared from the political debate. So what about 2015? It was the year that that Congress talked occasionally about deficits, but did more to increase future deficits than reduce them.

For now, they can get away with this. The deficit is, indeed, shrinking. When the books closed on the fiscal year that ended Sept. 30, the deficit came in at $439 billion, about $45 billion less than the year before. Spending was up (5 percent), but revenues were up more (8 percent in part because of recovering economy). Measured against the size of the economy, the most meaningful metric, the deficit amounted to 2.5 percent of Gross Domestic Product (GDP) versus 2.8 percent the year before. That’s below the average of the past 40 years and far from the deficit of nearly 10 percent of GDP recorded during the worst of the Great Recession.

So the deficit doesn’t pose much of a risk right now. The U.S. government is still borrowing billions at very low interest rates and there aren’t any signs that government borrowing is crowding out borrowing by the private sector.

That calm seems to have bred fiscal complacency among many in Congress. They’ve gone from offsetting spending increases with spending cuts or revenue increases, to matching spending increases with accounting gimmicks, to simply voting to increase spending and extend expiring tax breaks. To “pay for” a highway bill, for instance, Congress took $53 billion from the Federal Reserve, draining what is effectively the Fed’s saving account. But that’s a shell game that amounts to moving money from one government pocket to another and claiming you’ve offset spending. Congress lifted the caps it had previously set on annually appropriated spending—and for good reason—but it didn’t fully offset those spending increases with spending cuts elsewhere or with tax increases. And, as it left town in December, Congress didn’t even pretend to offset the cost (nearly $700 billion over 10 years) of extending a variety of expiring tax breaks.

This isn’t a problem today. Indeed, the economy in recent years has been hurt by too much belt-tightening in Washington, not too little. (Don’t believe me? Ask Ben Bernanke.) And that highway-fund gimmick may have been a politically acceptable route to prudent policy—borrowing today to make infrastructure investments that’ll pay off in the future.

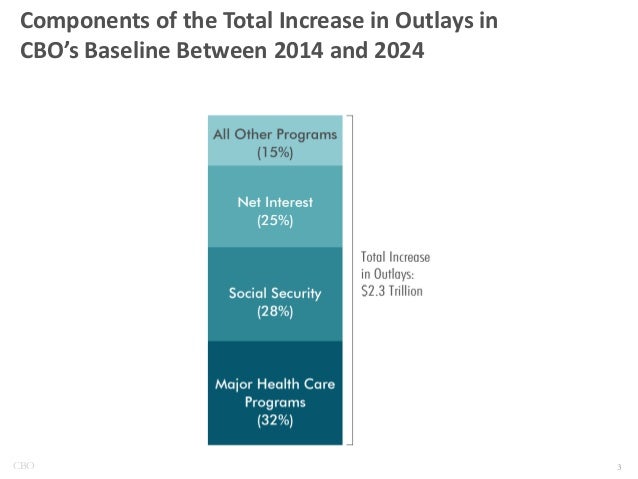

But all this threatens to make tomorrow’s problem worse. Today’s large debt leaves the nation less maneuvering room if it needs to borrow a lot in the future—to fight a war or another deep recession. Without a course correction, the debt will grow larger over the next couple of decades as more Baby Boomers become eligible for Social Security and Medicare and as health spending continues to grow faster than nearly anything else on the government’s shopping list. The federal debt held by the public, which amounted to about 35 percent of GDP before the Great Recession, is now about 75 percent of GDP. The latest Congressional Budget Office projections show that current policies will take it to about 103 percent of GDP—and that’s before the latest congressional gimmickry is accounted for. If all this borrowing were going to investments such as infrastructure, R&D and education—spending that could yield dividends in the future—that’d be one thing. But it isn’t. CBO says 85 percent of the projected rise in federal spending over the next decade will go to Social Security, major health-care programs and net interest on the federal debt.

Congress avoided catastrophe in 2015. It didn’t push the U.S. Treasury into defaulting on the federal debt. It didn’t force the government to shut down while it argued over spending bills. It didn’t allow federal transportation spending to halt abruptly for lack of legislative authority. So that’s a relief. But neither did Congress do much of anything to restrain the size of future deficits (which means belt-tightening and tax increases) or to take steps that might spur faster economic growth (which would be good for all, and would help relieve fiscal strains in the future.)

Oh well, there’s always next year.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

{kind=link}

Commentary

Op-edThe federal deficit is shrinking…for now

December 21, 2015