Tax policy reform specifically targeting the digital economy is being hotly debated in the European Union. EU member states have had difficulty taxing digital technology giants such as Amazon, Facebook, and Google. Supporters of reform, such as the governments of Germany and France, argue that companies operating in the digital arena profit unfairly from their internet-based operations. Others, such as the governments of Ireland and Luxembourg, worry that tax reform could lead to double taxation and higher prices.

While reform on corporate tax policy for the digital economy at the global level is far from reaching a consensus, the European Commission is calling for immediate change. Just a couple of months ago, in a report prepared for the European Parliament and the Council, the commission called for reform in the corporate tax framework within the EU.

Difficulties in taxing digital technology companies

In the last decade, digital technology companies have outperformed traditional brick-and-mortar companies. In 2006, only one digital technology company was among the top 20 companies in the EU, accounting for 7 percent of the market share among these high performers. Today, nine digital technology companies are in the top 20, accounting for a far more substantial 54 percent of market share. Between 2008 and 2016, the revenue of the entire retail sector in the EU grew 1 percent on average. In the same period, the revenue of the top five e-retailers grew 32 percent.

Yet, due to the virtual nature of business conducted by these digital technology companies, tax loopholes were invariably created, preventing many EU member states from collecting taxes on profits from such companies. Unlike traditional companies, whose profits are taxed at value creation, digital technology companies conduct most transactions electronically. This makes it challenging to capture where value is created, what it is, and how to measure it.

Additionally, companies are taxed through permanent establishment rules, which are largely based on physical presence. So, while digital technology companies operate virtually all over Europe, their profits are taxed only in the state where they have a physical establishment. Last summer, France lost a case against Google, which has a permanent establishment in Ireland, and consequently did not have to pay a 1.11 billion euro tax bill to France. The European Commission doesn’t believe this is a fair rule, arguing that such companies have access to markets, infrastructure, and regulatory institutions all over the EU, but “are not considered present for tax purposes.”

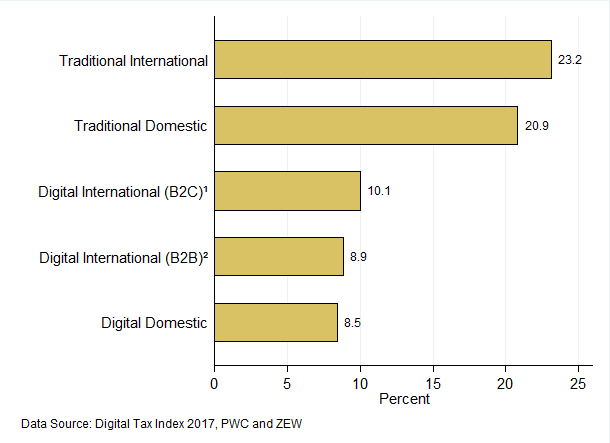

Even when taxes are collected, the average tax rate for digital companies ends up being much lower than that for non-digital, traditional companies. The Center for Economics and Business Research found that in the United Kingdom, for example, Amazon pays 11 times less corporation tax than traditional booksellers do. Differences in effective rates between digital technology companies and traditional ones, within the EU, are shown in Figure 1.

Figure 1. Effective average corporate tax rate by business model in EU-28

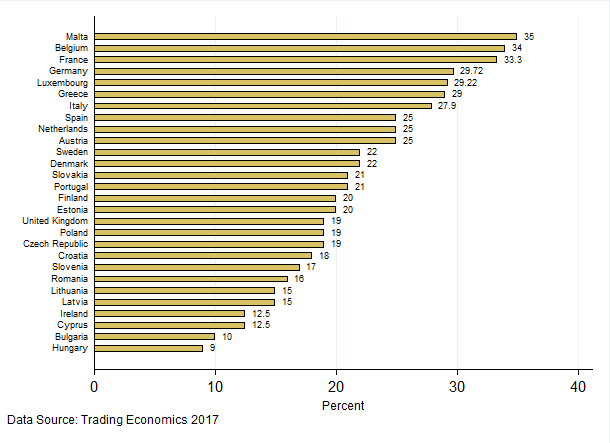

States with lower rates might think that they are benefiting from “permanent establishment” rules by attracting digital technology companies to physically headquarter there, as in the case of Ireland. This relationship clearly benefits the companies, but at what cost to their hosts? The European Commission has raised questions on the magnitude of benefits that these low tax-rate states receive from tax collection. In example of Ireland, at 12.5 percent, the country offers one of the lowest corporate tax rates within the EU, as shown in Figure 2. But last year, the commission found that in 2014 Apple paid an effective tax rate of only 0.005 percent to Ireland, leaving an unpaid tax bill of around 13 billion Euros.

Figure 2. Corporate tax rates by EU member states

In defense of digital technology companies

Arguably, the attitude of the European Commission, especially of Margrethe Vestager, who is the EU’s competition commissioner, has sometimes been described as openly belligerent against these digital giants. Some have argued that the proposed changes in the EU’s corporate tax policy outline would create a “hostile work environment” for U.S. businesses. Uncertainties among consumers may also arise since such reforms could lead to changes in prices, which could directly affect consumers within the EU. Finance ministers from Ireland and Luxembourg, who are not in support of the proposed changes, have raised the issue of double taxation as another concern. Moreover, the framework of the international tax rules would need to be re-written in case different countries and regions start to neglect or redraw rules concerning permanent establishment or transfer pricing.

The EU may show others the way

In the long run, the EU is planning to move toward an integrated digital single market, where rules regarding digital economy would be harmonized among all EU member states through policies such as the Common Consolidated Corporate Tax Base. This would create “a single set of rules to calculate companies’ taxable profits in the EU.” In the meantime, the European Commission suggests an “equalization tax on turnover of digitalized companies.” This, the commission believes, would address the issue of fairness within the EU member states, since taxes would no longer depend on “permanent establishment” but rather on “income generated from all internet-based business activities.”

Unlike traditional companies, digital companies already operate virtually all over the EU, while maintaining a “permanent establishment” in the countries with the lowest tax rates. Some believe that low tax rates helped states such as Ireland or even the U.K., but as in the case of Apple in Ireland, even these countries do not always generate revenues from their already-low rates. Targeting digital technology companies would narrow the current gap in tax rates between these companies and non-digital, traditional companies.

The EU is not the only one considering tax policy reforms for the digital economy. Numerous countries around the world, as well as major international bodies such as the OECD, have joined the discussion on taxing the digital economy. Indeed, issues related to rules such as “permanent establishment” go beyond the EU borders. Although EU member states have not reached a consensus on joint policies—a challenge in any economic union—the EU may end up showing the rest of the world how the digital economy should best be taxed.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Taxing the digital economy—It’s complicated

December 13, 2017