This chapter is part of USMCA Forward 2026.

Opportunities for agriculture

North American agriculture’s integration under NAFTA and now USMCA has created a continental market that buffers producers and consumers from global shocks, ensuring affordable food, stable value chains, and continued competitiveness. This integration is more important in an increasingly uncertain global trade environment, providing stability and resilience for producers and consumers across the continent. The upcoming USMCA review should be approached not as a reopening of settled ground, but as an opportunity to reinforce a framework that has already proven its worth in supporting stability, affordability, and competitiveness across North America’s agricultural economy.

Integration and competitiveness in North American agriculture

The United States, Canada, and Mexico together represent one of the most competitive and productive agricultural regions in the world. The United States and Canada are consistently among the top five global exporters of agricultural products over the past decade, accounting for 12% and 4.7% respectively of global agricultural exports in 2023,1 Mexico accounting for 3.1% in 2023.2

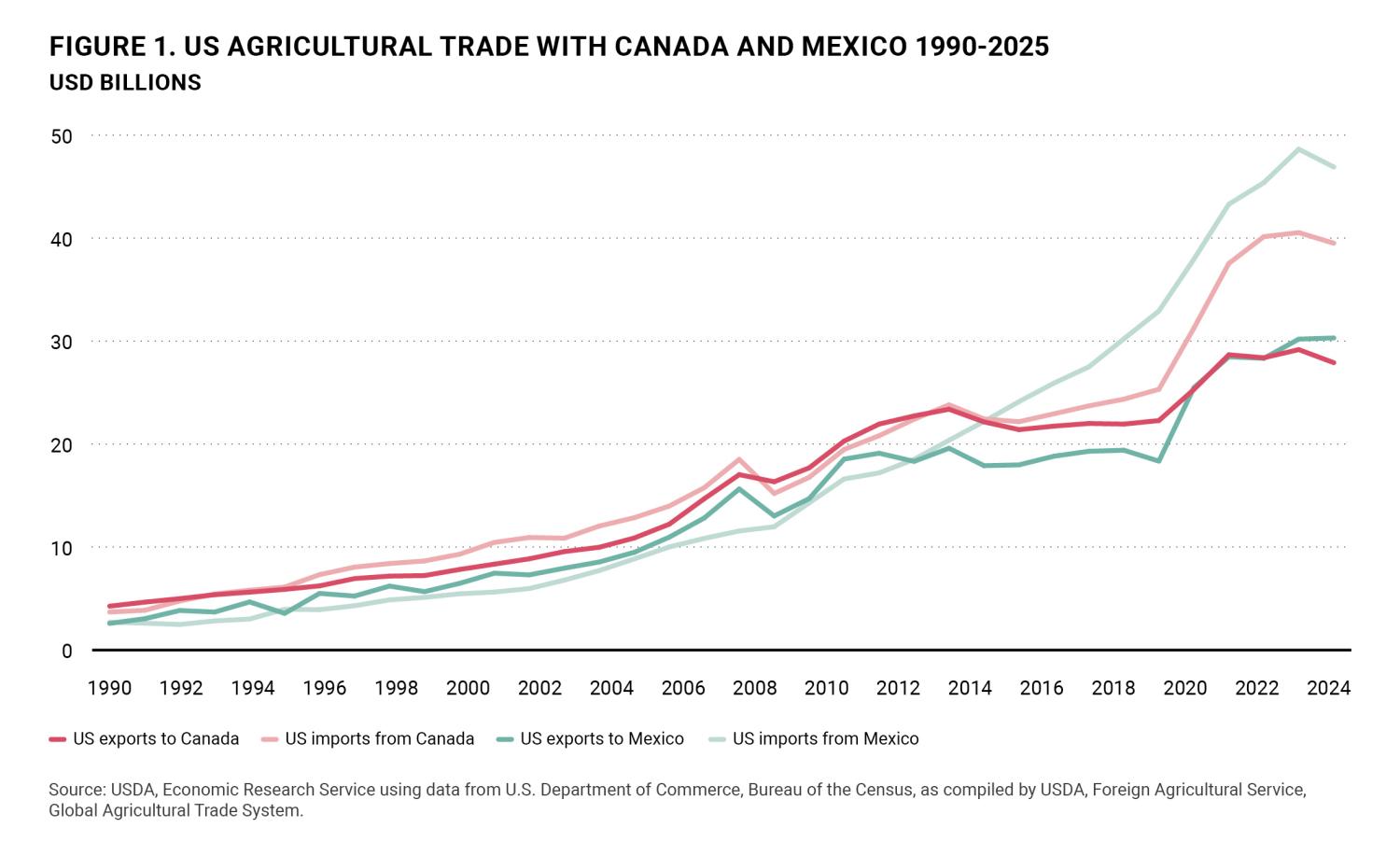

Intra-North American trade anchors the agricultural economies of all three countries. Since the inception of NAFTA, U.S. agricultural exports to Canada and U.S. agricultural imports from Canada have grown fourfold and tenfold respectively.3 At the same time, U.S. agricultural exports to Mexico and U.S. agricultural imports from Mexico have grown over fivefold and close to fifteenfold respectively (see Figure 1).4 Canada and Mexico are the destination for about one-third of U.S. agricultural exports, while for Mexico, 90% of exports go to the United States and Canada, and for Canada, 63% of exports go to the United States and Mexico.5

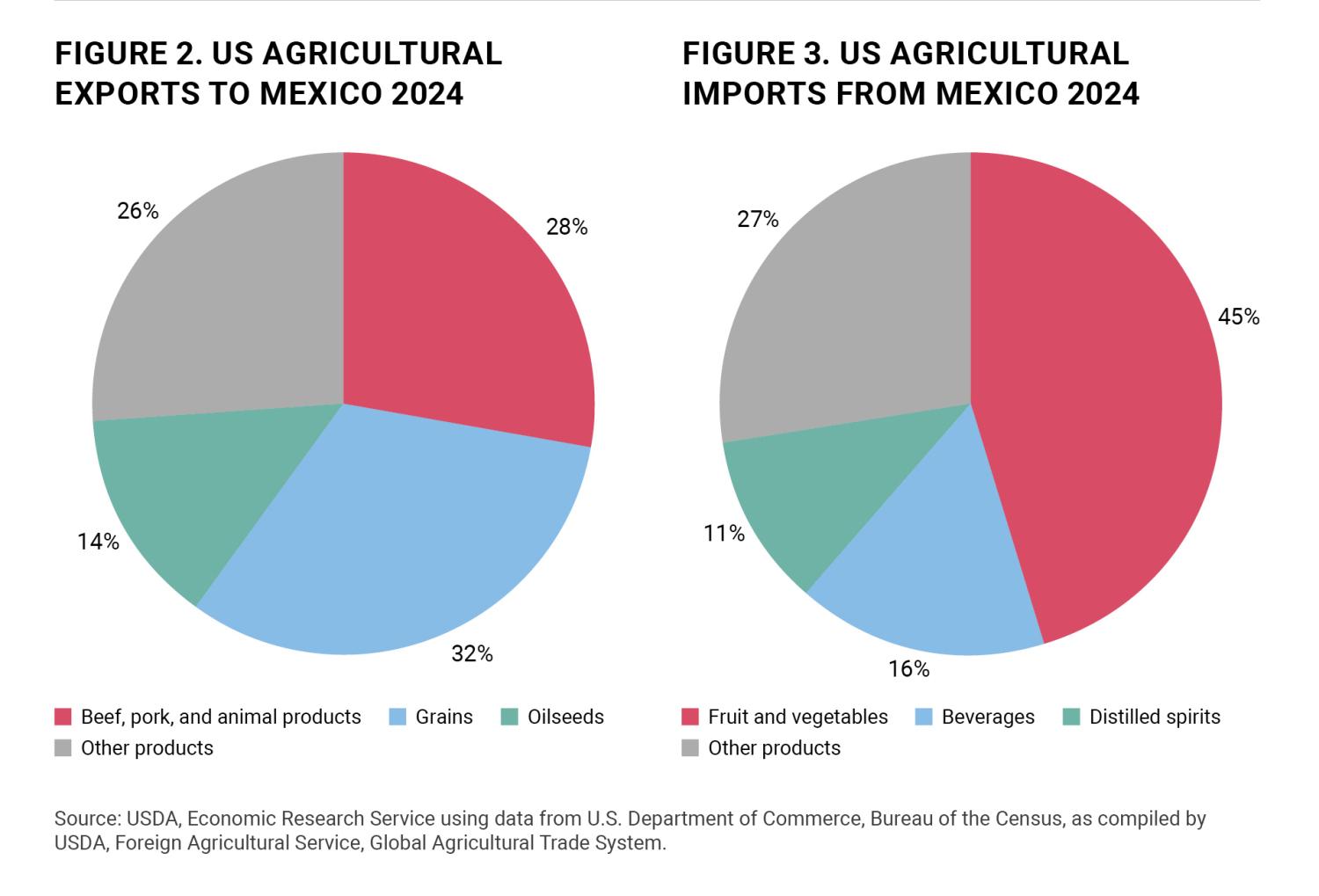

The three North American neighbors are both competitors and complements in agri-food markets. Traditional sources of comparative advantage—climate, land endowments, and consumer tastes—explain much of the trade in final agricultural products. But modern drivers such as innovation and integrated value chains have deepened cross-border interdependence by distributing production stages across the continent, similar to manufacturing systems that locate each step for efficiency. Land-intensive crops such as grains and oilseeds suited for temperate climates move south, while labor-intensive fruit and vegetables production that thrives in warmer regions moves north. In 2024, 73.3% of U.S. agricultural exports to Mexico were grains, oilseeds, meat, and related products, and 73.1% of U.S. agricultural imports from Mexico consisted of fruit, vegetables, beverages, and distilled spirits (see Figures 2 and 3).6

Competition, by contrast, is most visible in U.S.-Canada trade, where two-way exchange occurs in similar, but differentiated products. U.S. imports from Canada fall largely into categories where the United States is a globally-competitive exporter: In 2024, 61% of U.S. imports from Canada were meat, grains, oilseeds, and related products.7 This overlap reflects firms competing within integrated markets for grains, oilseeds, and animal products, while also benefiting from cross-border value chain efficiencies. In a sector where even modest differences in weather conditions can dramatically affect output and product characteristics, this form of intra-industry trade enhances resilience by providing food manufacturers a wider range of reliable inputs and consumers greater product variety. Differences in crop types and production methods—such as U.S. soybeans and soybean oil alongside Canada’s canola and canola oil—reflect specialization within a common market rather than duplication.

A further dimension of integration operates through cross-border value chains, in which raw materials or processed products from one country are inputs that support downstream industries in another. This dynamic is most clearly seen in cross-border livestock production: Canada exports feeder animals and hogs for slaughter, many of which are finished in U.S. operations concentrated in states such as Iowa and Minnesota.8 These facilities benefit from abundant feed supplies and slaughtering capacity, while processed pork products are exported throughout North America and globally. Mexico accounted for 37% of U.S. pork exports in 2022.9 The North American hog industry is thus a canonical example of a continental value chain, where multiple stages of production add value across borders.10

The North American agri-food system supports millions of jobs across agricultural production, food processing, manufacturing, logistics, and services, while providing consumers with stable, affordable food supplies. Together, the agri-food sectors contribute nearly $2 trillion to GDP and support more than 40 million jobs across the continent.111213 These linkages make North American agriculture more than a collection of national industries—it is a single continental system that delivers stability, global competitiveness and shared prosperity.

Sectoral resilience in the face of global headwinds

As global trade uncertainty, climate shocks, and rising protectionism threaten to disrupt vital food and agricultural markets, North America’s deeply integrated agricultural market is a vital source of stability. Trade is increasingly shaped by political conflict, strategic competition, and a growing emphasis on self-sufficiency. Geopolitics, rather than markets, now often determines access to key commodities and destinations.

Beijing’s recent curbs on agricultural imports from the United States and Canada reflect how geopolitics can shape trading relationships. Both countries have experienced politically motivated disruptions that reveal China’s leverage as a dominant buyer in global agricultural markets. In 2019, following a bilateral diplomatic dispute, China suspended import permits for two Canadian canola exporters, citing quality concerns.14 In 2024, China retaliated against Canada’s implementation of a 100% tariff on Chinese electric vehicles (EVs)15 with a 100% tariff on Canadian canola, followed by a 75.8% anti-dumping duty described as an “unmistakable act of economic coercion.”16

Similarly, the ongoing U.S.–China trade conflict has been damaging to the U.S. farm sector, most notably soybean exports. The loss of market share to Brazil has been compounded by China’s recent lack of soybean purchases from the United States,17 and diversion to other markets is unlikely to offset the loss. These interventions matter because China remains a major agricultural export market for both U.S. and Canada, particularly for grains, oilseeds and meat. In 2022, China was the top destination for U.S. agricultural exports, valued at $36.4 billion for the fiscal year (October 2021-September 2022), accounting for 18% of Chinese imports.18 Canada was China’s 8th largest supplier of agricultural products worth $7.6 billion, or 3% of imports.19

These developments are occurring as the rules that have defined the global trading system weaken. Analysts describe a drift toward fragmented, preferential trade arrangements as the World Trade Organization’s influence wanes and multilateral governance erodes. Economist Richard Baldwin20 characterizes this emerging order as “managed multilateral drift”: The World Trade Organization (WTO) endures with diminished authority, while regional and bilateral agreements take precedence. In this environment, regional frameworks such as the USMCA are becoming the practical anchors of stability, transparency, and rules-based trade for the agri-food sector.

USMCA’s role and achievements

In a world of rising protectionism, the extent of the North American agri-food system’s integration should be reinforced, not relitigated. Under NAFTA, tariffs between the United States and Canada were fully eliminated by 1998, except for select exemptions for dairy, poultry, and egg products, sectors that Canada still governs through supply management. Tariff elimination between the United States and Mexico was completed by 2008, with no exclusions, while Canada-Mexico trade retained limited exemptions for dairy and poultry.

Progressive liberalization of agricultural trade in North America created opportunities and prosperity, though not without adjustment. For example, agriculture’s share of total Mexican employment has halved since 199421 and the total number of corn-producing farms declined by 48% between 1991 and 2014.22 This was driven at least in part by the exposure to competition from producers north of the border.

The USMCA built directly on NAFTA’s achievements, preserving tariff-free trade for nearly all agricultural products while introducing targeted improvements to address remaining market-access challenges stemming from regulatory differences and administrative complexities. For U.S. producers, the agreement expanded opportunities in several sensitive Canadian sectors. A salient improvement was the establishment of tariff-rate quotas (TRQs) providing greater market opportunities for U.S. exports of dairy, poultry, and egg products.23 The new TRQs created modest but symbolically important gains for these sectors, though concerns remain about how the TRQs are administered and the effective level of U.S. access to the Canadian dairy market.24

The agreement also enhanced transparency in sanitary and phytosanitary (SPS) measures and reaffirmed that food safety and plant and animal health regulations should be based on scientific evidence.25 These provisions reduce uncertainty and compliance costs while safeguarding consumer safety—crucial for sectors such as livestock, grain, and horticulture, where technical standards often determine market access. By consolidating market access, enhancing regulatory coherence, and reestablishing credible dispute resolution, USMCA has transformed North American agricultural integration from an economic relationship into an institutional framework for competitiveness and resilience.

Managing frictions under USMCA

Disagreements are inevitable, particularly in sensitive sectors and as markets and technologies evolve. One of USMCA’s core institutional achievements has been the establishment of a credible dispute settlement mechanism that allows trade frictions to be managed through predictable processes rather than political escalation. This mechanism has functioned effectively in practice, reinforcing confidence in the agreement’s credibility—and North America’s agricultural resilience.

Since 2022, five disputes have been resolved through USMCA panel investigation—in comparison to only three investigations under NAFTA.26 Of the five cases, three have involved important agricultural issues, including quota allocation under the Canadian dairy TRQ system and Mexico’s proposed ban on imports of genetically modified corn.27 These disputes highlight that friction is not failure—it is evidence of a mature, integrated system operating under enforceable rules.

Longstanding trade frictions that predate USMCA underscore why a credible dispute settlement mechanism remains essential. A prominent example is recurring tension over U.S.-Mexico tomato trade. In 1996, the U.S. Department of Commerce and the Mexican tomato industry reached a suspension agreement halting an anti-dumping investigation and setting a minimum reference price for Mexican tomato imports. This arrangement helped ensure a stable and expanding year-round supply of tomatoes for U.S. buyers. The agreement was subsequently renegotiated in 2002, 2008, 2013, and 2019, but was terminated in April 2025,28 leading to antidumping duties of 17.1% on all Mexican tomato imports.29

The dispute’s re-emergence after nearly three decades highlights a split among U.S. tomato growers: southeastern growers, especially in Florida, have consistently opposed the agreement, while western growers and importers—many of whom are deeply integrated with Mexican tomato suppliers and operating on both sides of the border—have supported it.30 This long history, shaped by political considerations and U.S.-centric anti-dumping rules, reinforces the argument for an established, enforceable dispute settlement mechanism. By providing channels to resolve tensions transparently, USMCA sustains the trust and predictability that cross-border value chains require.

Future-proofing North American agri-food integration

Importantly, the upcoming USMCA review will unfold in a markedly different environment from when the agreement was negotiated. American consumers remain sensitive to food prices—in late 2025 the administration temporarily exempted a range of imported food products from tariffs imposed earlier in the year to ease cost pressures.31 This context underscores the political and economic value of maintaining a predictable, transparent trade regime within North America—ensuring consumers benefit from affordable food supplies even amid global volatility.

The review offers an opportunity to consolidate North America’s agricultural gains and prepare for new challenges. The objective should not be to renegotiate the fundamentals of market access, but to future-proof the framework—reducing transaction costs, improving regulatory coordination, and enhancing the resilience of agricultural value chains. To sustain these gains, the upcoming review should focus on three priorities:

- Preserve tariff-free trade and avoid new border measures: The most immediate priority is to preserve tariff-free trade across the continent. Any new border measures—whether for political leverage or sectoral protection—would undermine the efficiencies and complementarities that define the integrated agri-food market.

- Ensure clear and simple rules of origin: Clear, simple rules of origin are essential so small and medium-sized enterprises can fully participate in cross-border value chains. Excessive administrative complexity risks discouraging smaller producers and processors, weakening the value chains that underpin competitiveness and employment.

- Deepen Regulatory Cooperation and Standards Alignment: Despite tariff-free trade, non-tariff barriers—such as divergent pesticide regulations, labeling requirements, and biotech approvals—continue to create friction. Deeper regulatory cooperation, building on USMCA’s science-based provisions, would reduce compliance costs while maintaining consumer safety and public confidence.32

Strengthening these core provisions would ensure that North American agriculture remains competitive and resilient in an increasingly uncertain global environment. For agriculture, refining—not reopening—the agreement allows USMCA partners to reinforce the sector’s role as a driver of shared prosperity across the continent.

Authors

Related Content

2026

-

Footnotes

- World Trade Organization, “Import and Export Charts: Agricultural Products,” World Trade Organization, n.d., https://www.wto.org/english/tratop_e/agric_e/ag_imp_exp_charts_e.htm#ag_products.

- World Trade Organization, “Import and Export Charts: Agricultural Products,” World Trade Organization, n.d., https://www.wto.org/english/tratop_e/agric_e/ag_imp_exp_charts_e.htm#ag_products.

- U.S. Department of Agriculture, Economic Research Service, “Canada: Trade & FDI,” last updated February 5, 2025, https://www.ers.usda.gov/topics/international-markets-us-trade/countries-regions/usmca-canada-mexico/canada-trade-fdi.

- U.S. Department of Agriculture, Economic Research Service, “Mexico: Trade & FDI,” last updated July 22, 2025, https://www.ers.usda.gov/topics/international-markets-us-trade/countries-regions/usmca-canada-mexico/mexico-trade-fdi.

- Food and Agriculture Organization of the United Nations, “Detailed trade matrix,” FAOSTAT, https://www.fao.org/faostat/en/#data/TM

- U.S. Department of Agriculture, Economic Research Service, “Mexico: Trade & FDI,” last updated July 22, 2025, https://www.ers.usda.gov/topics/international-markets-us-trade/countries-regions/usmca-canada-mexico/mexico-trade-fdi.

- U.S. Department of Agriculture, Economic Research Service, “Canada: Trade & FDI,” last updated February 5, 2025, https://www.ers.usda.gov/topics/international-markets-us-trade/countries-regions/usmca-canada-mexico/canada-trade-fdi

- Steven Zahniser, Sahar Angadjivand, Thomas Hertz, Lindsay Kuberka, and Alexandra Santos, NAFTA at 20: North America’s Free-Trade Area and Its Impact on Agriculture, WRS-15-01 (Washington, DC: U.S. Department of Agriculture, Economic Research Service, February 2015), https://ers.usda.gov/sites/default/files/_laserfiche/outlooks/40485/51265_wrs-15-01.pdf?v=14354.

- U.S. Department of Agriculture, Economic Research Service, “Hogs & Pork: Sector at a Glance,” last updated January 8, 2025, https://www.ers.usda.gov/topics/animal-products/hogs-pork/sector-at-a-glance.

- Pol Antràs, “Conceptual Aspects of Global Value Chains,” The World Bank Economic Review 34, no. 3 (October 2020): 551–74, https://doi.org/10.1093/wber/lhaa006.

- U.S. Department of Agriculture, Economic Research Service, “Ag and Food Sectors and the Economy,” Ag and Food Statistics: Charting the Essentials, updated February 25, 2026, https://www.ers.usda.gov/data-products/ag-and-food-statistics-charting-the-essentials/ag-and-food-sectors-and-the-economy

- Agriculture and Agri-Food Canada, “Overview of Canada’s Agriculture and Agri-Food Sector,” Agriculture and Agri-Food Canada, last modified August 14, 2025, https://agriculture.canada.ca/en/sector/overview

- Prodensa, “Manufacturing in Mexico: the Food & Beverage Industry,” Prodensa Insights Blog, April 28, 2025, https://www.prodensa.com/insights/blog/manufacturing-in-mexico-the-food-beverage-industry

- Shaoyan Sun, China’s Ban on Canadian Canola: Reasons, Impacts, and Policy Perspectives, Occasional Paper (Edmonton: China Institute, University of Alberta, October 2020), https://www.ualberta.ca/en/china-institute/media-library/media-gallery/research/occasional-papers/canola2.pdf.

- “China Surtax Order (2024),” SOR/2024-187, Canada Gazette, Part II, vol. 158, no. 21 (October 9, 2024), https://gazette.gc.ca/rp-pr/p2/2024/2024-10-09/html/sor-dors187-eng.html.

- Vina Nadjibulla, “China’s Canola Tariffs are a Dangerous Trap,” Asia Pacific Foundation of Canada, September 3, 2025, https://www.asiapacific.ca/publication/chinas-canola-tariffs-are-dangerous-trap.

- Joana Colussi and Michael Langemeier, “U.S.–China Soybean Deal: Comparing Past Export Levels and Global Market Impacts,” farmdoc daily 15, no. 212 (November 17, 2025), https://farmdocdaily.illinois.edu/2025/11/us-china-soybean-deal-comparing-past-export-levels-and-global-market-impacts.html.

- Agriculture and Agri-Food Canada, “Market Overview – China,” last modified July 2, 2025, https://agriculture.canada.ca/en/international-trade/market-intelligence/reports-and-guides/market-overview-china#a.

- Agriculture and Agri-Food Canada, “Market Overview – China,” last modified July 2, 2025, https://agriculture.canada.ca/en/international-trade/market-intelligence/reports-and-guides/market-overview-china#a.

- Richard Baldwin, The Great Trade Hack: How Trump’s Trade War Fails and the World Moves On (Paris: CEPR Press, 2025), https://cepr.org/publications/books-and-reports/great-trade-hack-how-trumps-trade-war-fails-and-world-moves.

- World Bank, “Employment in Agriculture (% of Total Employment) (Modeled ILO Estimate) – Mexico,” World Bank Open Data, https://data.worldbank.org/indicator/SL.AGR.EMPL.ZS?locations=MX.

- Steven Zahniser, Nicolás Fernando López López, Mesbah Motamed, Zully Yazmin Silva Vargas, and Tom Capehart, The Growing Corn Economies of Mexico and the United States, FDS-19F-01 (Washington, DC: U.S. Department of Agriculture, Economic Research Service, August 2019), https://ers.usda.gov/sites/default/files/_laserfiche/outlooks/93633/FDS-19F-01.pdf.

- U.S. Department of Agriculture, Economic Research Service, “Canada: Trade & FDI,” last updated February 5, 2025, https://www.ers.usda.gov/topics/international-markets-us-trade/countries-regions/usmca-canada-mexico/canada-trade-fdi.

- Office of the United States Trade Representative, 2025 National Trade Estimate Report on Foreign Trade Barriers (Washington, DC, March 2025), https://ustr.gov/sites/default/files/files/Press/Reports/2025NTE.pdf.

- Julieta Contreras, Gary Clyde Hufbauer, Jeffrey J. Schott, and Ye Zhang, “The Future of the USMCA,” Peterson Institute for International Economics, updated April 25, 2025, https://www.piie.com/microsites/2025/future-usmca.

- [1] Ian Sheldon and Daniel C. K. Chow, “The Future of Dispute Resolution in International Trade,” Applied Economic Perspectives and Policy (2025): 1–21, https://doi.org/10.1002/aepp.13518.

- Julieta Contreras, Gary Clyde Hufbauer, Jeffrey J. Schott, and Ye Zhang, “The Future of the USMCA,” Peterson Institute for International Economics, updated April 25, 2025, https://www.piie.com/microsites/2025/future-usmca.

- Andrew I. Rudman, “Rotten Tomatoes: Implications of the Termination of the U.S.-Mexico Tomato Suspension Agreement,” Center for Strategic and International Studies, August 19, 2025, https://www.csis.org/analysis/rotten-tomatoes-implications-termination-us-mexico-tomato-suspension-agreement.

- U.S. Department of Commerce, International Trade Administration, “U.S. Department of Commerce Announces Withdrawal from 2019 Suspension Agreement on Fresh Tomatoes from Mexico,” July 14, 2025, https://www.trade.gov/feature-article/us-department-commerce-announces-withdrawal-2019-suspension-agreement-fresh.

- Andrew I. Rudman, “Rotten Tomatoes: Implications of the Termination of the U.S.-Mexico Tomato Suspension Agreement,” Center for Strategic and International Studies, August 19, 2025, https://www.csis.org/analysis/rotten-tomatoes-implications-termination-us-mexico-tomato-suspension-agreement.

- White House, “Modifying the Scope of the Reciprocal Tariff with Respect to Certain Agricultural Products,” Presidential Actions, November 14, 2025, https://www.whitehouse.gov/presidential-actions/2025/11/modifying-the-scope-of-the-reciprocal-tariff-with-respect-to-certain-agricultural-products/.

- Office of the United States Trade Representative, 2025 National Trade Estimate Report on Foreign Trade Barriers (Washington, DC, March 2025), https://ustr.gov/sites/default/files/files/Press/Reports/2025NTE.pdf.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).