This week, Senate Budget Committee Chairwoman Patty Murray introduced legislation that would provide tax relief for working families. Her bill would establish a deduction for two-earner families and expand the Earned Income Tax Credit (EITC) for childless individuals. The proposed “secondary earner deduction” would allow married-couple families to deduct a portion of the secondary worker’s earnings from their family’s taxable income, increasing both the return to work and these families’ available resources. If enacted, this bill will immediately allow hard-working American couples to keep more of their earnings and improve the economic security of over 7 million families, according to estimates from the Joint Committee on Taxation.

The proposed legislation closely follows the secondary earner deduction outlined in our December 2013 Hamilton Project paper, which we justified on grounds of both fairness and efficiency. In our paper, we illustrate how the secondary earner penalty arises from the family-based nature of the U.S. federal income tax system. For families headed by a married couple, spousal income is pooled, and the first dollar of earnings by a spouse—or “secondary” earner —is taxed at the marginal tax rate of the last dollar earned by the primary worker. Under the current federal tax and transfer system, and assuming standard child care costs, we estimate that a family headed by a primary earner making $25,000 per year will “take home” less than 30 percent of a secondary worker’s pay. In other words, the effective average tax rate on the secondary worker’s earnings is 70 percent.

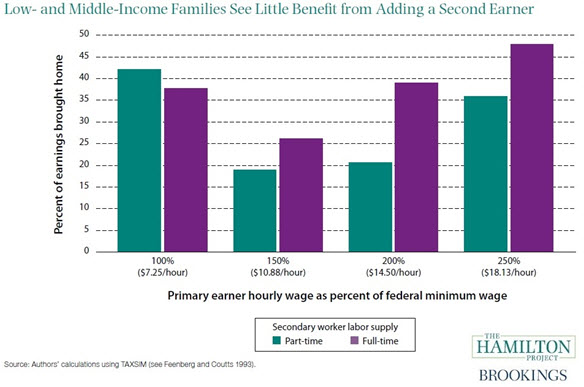

The figure below—taken from our Hamilton Project paper—shows the take-home share of earnings for a secondary earner for four different wage levels:

This makes it especially difficult for low-wage couples to work their way up the economic ladder. Consider a family of four, in which the primary earner makes $25,000 per year (a little over 150 percent of the current federal minimum wage of $7.25). As this family adds a second worker with similar earnings, their payroll taxes double, they lose their entire EITC (approximately $5,000), and they see an increase in federal income taxes (approximately $2,500). This family also loses eligibility for food assistance through the SNAP program (worth over $2,500) and may also incur child care costs. As this example illustrates, working poor families see little economic gain from a spouse’s labor supply.

Senator Murray’s “21st Century Worker Tax Cut Act” would allow low- and middle-income families with young children to deduct a portion of the secondary worker’s earnings from their family’s taxable income. Specifically, married-couple families with at least one child under the age of 12 and adjusted gross income below $130,000 (with phase-out starting at $110,000) could deduct 20 percent of up to $60,000 of the secondary earner’s income. Low-income families would benefit through an increase in their EITC. Middle-income families would benefit from a lower federal income tax bill.

The proposed legislation couples this deduction with an expansion of the EITC for childless workers. The EITC is viewed as the most important source of cash assistance to low-income families in the United States. Furthermore, since receipt of the credit requires positive earnings, the tax credit encourages individuals to work, addressing the enduring criticism that traditional transfer programs discourage work. However, the EITC is less successful at rewarding the work efforts of dual-earner families. As a consequence of our family-based system of income taxation, many dual-earner couples—even those in which both spouses earn the federal minimum wage—bring in a combined income that puts them beyond the income eligibility for the full EITC. The proposed legislation would take an important step toward addressing this shortcoming.

A secondary earner tax deduction becomes even more important once the EITC is expanded for childless individuals. Consider a single mother with two children making $25,000 a year. Under current law, she qualifies for an EITC benefit of approximately $5,000. As we have already pointed out, if she marries someone making $25,000, as a couple they would no longer qualify for an EITC payment. Now consider an expanded EITC program such that the childless individual could also qualify for a sizable EITC payment on his own. Now if the two marry, the increase in taxes they experience upon marriage is even larger because they would lose both EITC payments. For this reason, it is especially important than an expansion of the EITC for childless individuals be paired with a secondary earner tax deduction.

The legislation put forward by Senator Murray recognizes this, and wisely pairs a secondary earner tax deduction for low- and middle-income families with an expanded EITC schedule for single childless individuals. As public finance economists, we consider the coupling of a secondary earner tax deduction with an expansion of the EITC for childless individuals an important and forward-looking proposal.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

New Tax Legislation Would Increase the Return to Work for Low- and Middle-Income Working Families

March 27, 2014