The U.S. dollar has fallen around 10% on a broad, trade-weighted basis since the start of President Trump’s second term. This fall has come in short, sharp bursts that have been very unnerving. The first of these was in April 2025 in the wake of the chaotic rollout of reciprocal tariffs. The second came more recently in January 2026 during the World Economic Forum summit in Davos, when the U.S. escalated its rhetoric over Greenland.

The sudden and sharp nature of these falls is unusual for a currency that’s traded and used as widely as the dollar. The daily flow of transactions into and out of the dollar is massive, which should rule out sudden, sharp declines. The fact that such declines have taken place nonetheless has sparked debate whether the U.S. is losing its reserve currency status. This post looks at the IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) data, which survey the allocations reserve managers make to different currencies. Remarkably, there is very little indication that reserve managers are exiting the dollar, maybe for lack of obvious alternatives. As a result, the fall in the dollar we’re seeing is more likely of the benign variety, driven by expectations for growth and monetary policy in the U.S. vis-à-vis its trading partners.

No loss of reserve manager allocations to the dollar

Reserve managers are the people who run the official foreign exchange (FX) reserves of countries like China or Japan. Those reserves are built up over time when a country buys dollars to absorb appreciation pressure on its currency. Reserve managers then decide what fraction of these reserves are kept in dollars versus other currencies. This is a pretty secretive business and for good reason. If markets got wind of how reserve managers behave, they’d front-run them, putting them at a severe disadvantage. As a result, reserve managers are unlikely to react to the high-frequency news flow, including erratic Trump administration policies since the inauguration.

Source: Haver Analytics

Source: Haver Analytics

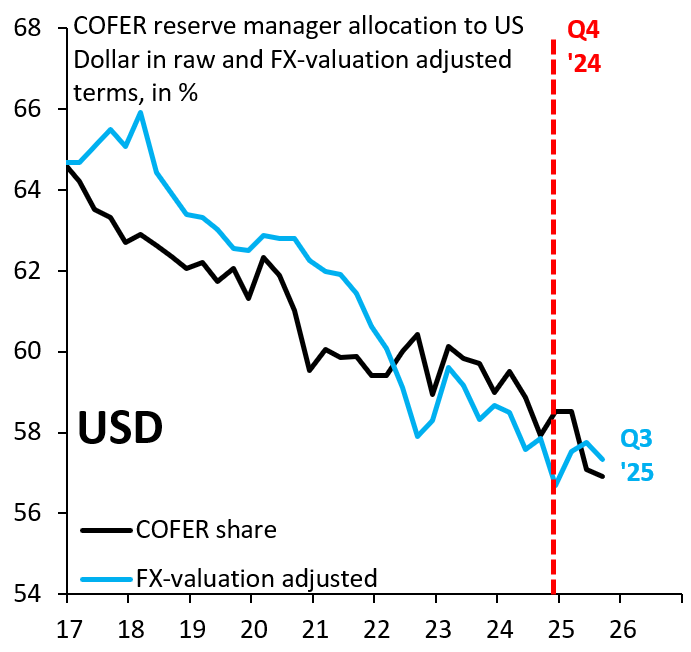

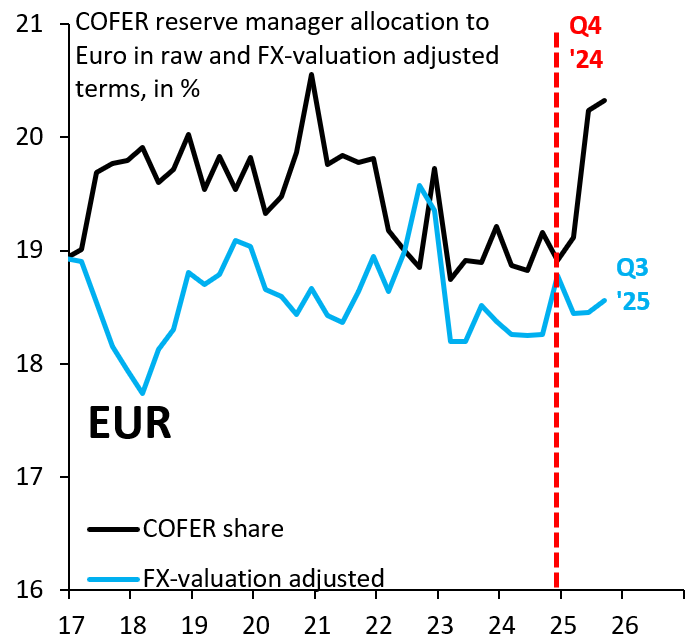

The IMF runs a quarterly survey (COFER) on how official foreign exchange reserves are allocated across currencies. The last data point in this survey is Q3 2025 and therefore covers the most turbulent quarter for the dollar so far (Q2 2025). The black lines in the two charts above show the raw COFER data for the U.S. (Figure 1) and the eurozone (Figure 2). Since reserve managers hold euros and other currencies, a sharp fall in the dollar—like in Q2 2025—can cause what looks like a sharp drop in allocations to the dollar, but this is just an FX-valuation effect. The blue lines above take out this valuation effect and thus provide a cleaner perspective on what reserve managers are doing. The remarkable conclusion from these charts is that—while there is a longer-term decline in allocations to the U.S. dollar, it does not look like—based on the available data—that there is a decline since the start of President Trump’s second term. Similarly, the euro should have been the main beneficiary in the policy turmoil over the past year, but it has failed to make any meaningful inroads into dollar dominance. This suggests that the hurdle to loss of reserve currency status is very high, maybe for lack of any viable alternative to the dollar.

Source: Haver Analytics

Source: Haver Analytics

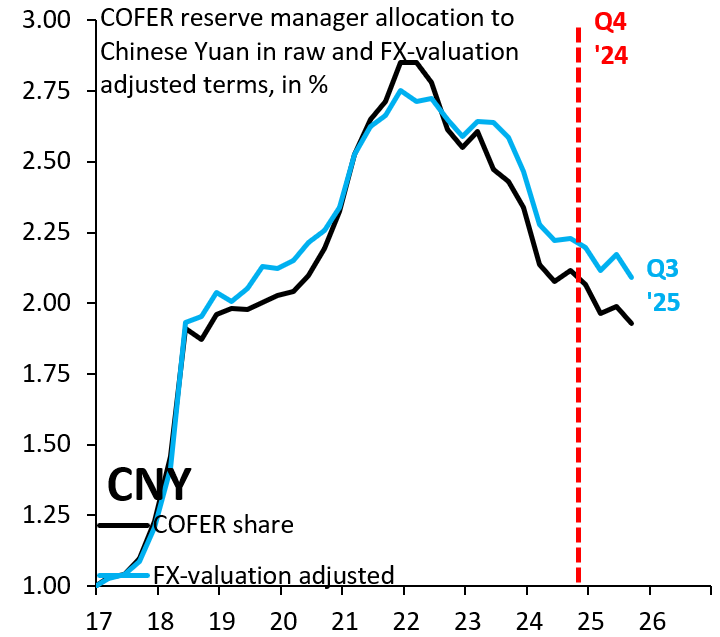

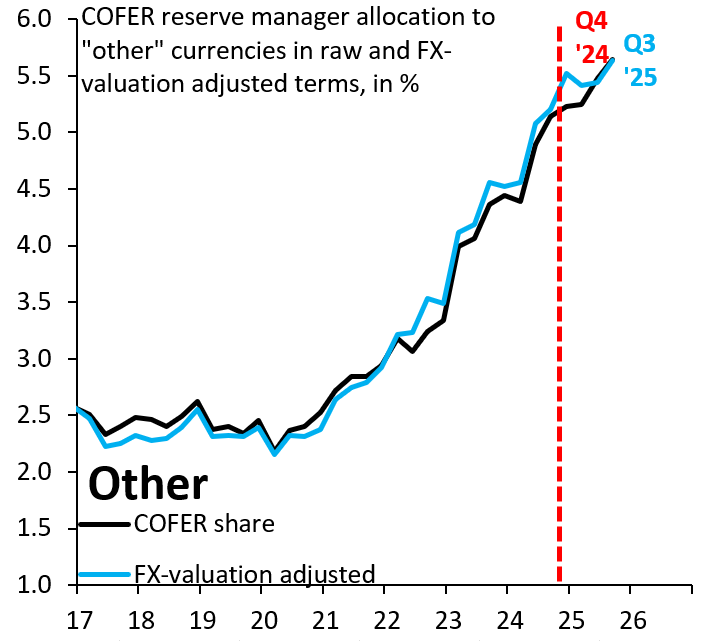

Figures 3 and 4 complement this perspective with a look at the Chinese yuan and a catchall category called “other,” which includes the Swedish krona, Korean won and Singaporean dollar among others. It’s notable that the Chinese yuan actually lost allocations since the start of the second Trump term, while the main beneficiary—recently and over the medium term—has been the “other” category. Reserve managers are certainly shifting their allocations, but this is happening into smaller currencies and at the margins. The hurdle to erosion of reserve currency status looks to be very high.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Is the US dollar’s reserve currency status eroding?

February 26, 2026