This chapter is part of USMCA Forward 2026.

Over the past three decades, the steel industry across Canada, Mexico, and the U.S. has evolved into a true regional market with high value production, processing, distribution, and consumption throughout the wider North American region. The USMCA and its NAFTA predecessor have been highly important in not only building this regional steel market, but also in sustaining the overall industry. The supply chain serving the construction and manufacturing industry is heavily dependent on free trade across the region. Section 232 tariffs on steel have inhibited this supply chain from operating efficiently. The removal of these tariffs, with appropriate safeguards, will better support the regional economic growth.

From the founding of U.S. Steel, the world’s first billion-dollar corporation, to the pioneering use of the Electric Arc Furnace (EAF) by Nucor, steelmaking has a long and storied history in North America. Today, steel producers in Canada, Mexico, and the U.S. are among the cleanest and most efficient in the world.1 Steelmakers here have continued to invest across the region into high value, low emission steelmaking, predicated on serving the North American market.

Steel, an industrial good and basic material, is a building block of modern society. While the process of steel manufacturing can sound simple, steel is an engineered product deliberately crafted to satisfy a specific end use for each heat of the furnace.

Barriers to entry in this market are initially related to the capital required to build a mill and generally two to five years to construct and start the mill, depending on the size and specific product produced. In the U.S. market, steel producers have enjoyed some of the highest prices across the world.2 This is due to the U.S. and North America positioned as net importers of steel. In these markets, imports are required across key products to satisfy demand, and imports are often the marginal source of supply. Due to this, rather than steel prices being set by the domestic cost curve, market prices are often determined by the cost of imported steel, particularly in stronger periods of demand.

In 2024, Canada, Mexico, and the U.S. imported 49 million tons of finished and semi-finished carbon steel with 32.6% of these imports coming from within the region. Five countries accounted for the next 30% of imports. These countries in order of import market share are: Brazil (10.1%), South Korea (7.2%), Japan (6.0%), Vietnam (3.7%), and China (3.1%).3

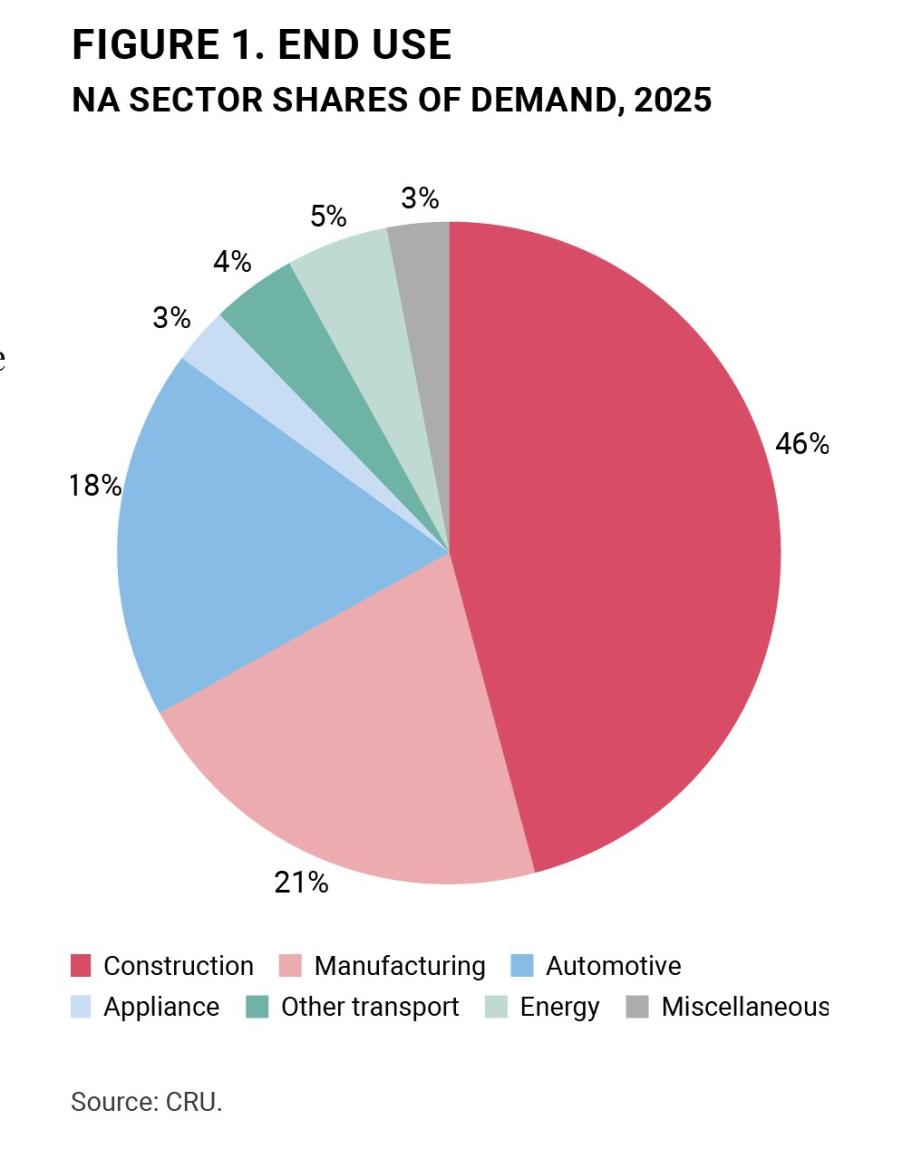

Steel is used across a variety of industries, and as a result, changes in the price of steel can have broad economic effects. The following chart shows the diversity of end use demand. Though these segments can be consolidated into two primary categories: construction, and manufacturing when Appliance, Automotive, and Other transport are included in Manufacturing. When combined, these two categories reflect nearly 90% of steel consumption.4

Construction is the largest source of direct end use steel demand. This category covers uses such as residential buildings, offices, hotels, data centers, and infrastructure, among others. Demand from each of these single categories can be cyclical from others based on underlying trends in each segment. For example, over the past two years, spending on office construction has trended lower while spending on data center construction has surged and is set to overtake spending on traditional offices.5

Manufacturing is the other major segment of steel demand as it includes the creation and assembly of products such as fabricated metal goods, machinery, and light weight vehicles. In construction, steel is used once per project, such as beams on a multi-story hotel or rebar for a highway project. Yet in manufacturing, steel is a consumable that scales alongside overall output. For example, the more vehicles built, the more steel consumed.

Cyclical market and volatile prices

The timeline between the initial order and when steel is placed into final use is measured in months, due to mill lead times as well as downstream processing and distribution. Due to this time frame, seasonal demand changes or sudden shifts in demand can wreak havoc with supply chain inventories as occasional production shortfalls or shifts in trade can suddenly tighten market supply leading to a domestic price surge. The opposite can also happen where demand forecasts are suddenly deemed too optimistic and orders further down the supply chain are cancelled. In this instance, inventories of steel products which were built up to support higher demand expectations are suddenly in a surplus. This surplus can quickly limit new orders placed at the mill, creating recessionary conditions until inventories are more in line with demand.

This often unpredictable behavior between supply and demand as well as the dependence on imports, which have even longer lead times, lead to high levels of price volatility. This dynamic plays out across North American markets as the region is historically interconnected due to the free trade agreements which have led to manufacturers expanding across borders.

Despite this volatility in prices, steel’s role as a primary industrial input results in price inelasticity of demand particularly over short periods. For example, following the pandemic lockdowns benchmark hot rolled (HR) coil steel surged by over 300%,6 yet steel demand remained largely unchanged. Yet over time, higher steel prices have led to some substitution such as lumber taking back share from steel studs, or asphalt shingles replacing steel roofing, as well as declines in demand as the higher prices negatively impacted various industries.

Current state: Intensified steel trade protection

In North America, the U.S. steel market is the largest market in the region as well as the most protected market in terms of imports.7 For decades, the U.S. mills have relied on antidumping (AD) and countervailing duties (CVD) as a tool to limit the financial disruption associated with dumped or subsidized imports from foreign steel makers. These cases are often filed during periods of low profitability in the market. This protection typically focuses on antidumping cases, which aim to address imports of steel sold at less than fair value, or where the foreign producers have a lower production cost due to government support. If a case is successful, despite requirements for a sunset review of the tariffs every five years, tariffs can remain in place for decades. Examples of this include an antidumping order placed on certain stainless steel wire rod from India in 19948 as well as carbon steel plate from China in 1997 that both continue to remain in effect today.9

While AD/CVD cases are very specific and target individual countries and producers by product, there are other trade tools used by the U.S. to limit steel imports. The most recent examples are the Section 201 (S201) from the U.S. Trade Act of 1974 and Section 232 (S232) from the U.S. Trade Expansion Act of 1962. Each of these had been used in the past before they were used to protect the steel industry. For example, President Ronald Reagan utilized S201 to impose 45% tariffs on large motorcycles from Japan in the 1980s after a petition from Harley-Davidson.10 The first positive determination of S232 was in 1973 after an investigation found that oil imports threatened national security.11 The remedy in this case was instituting an import license scheme, protection for refineries, and incentives for new refining capacity.

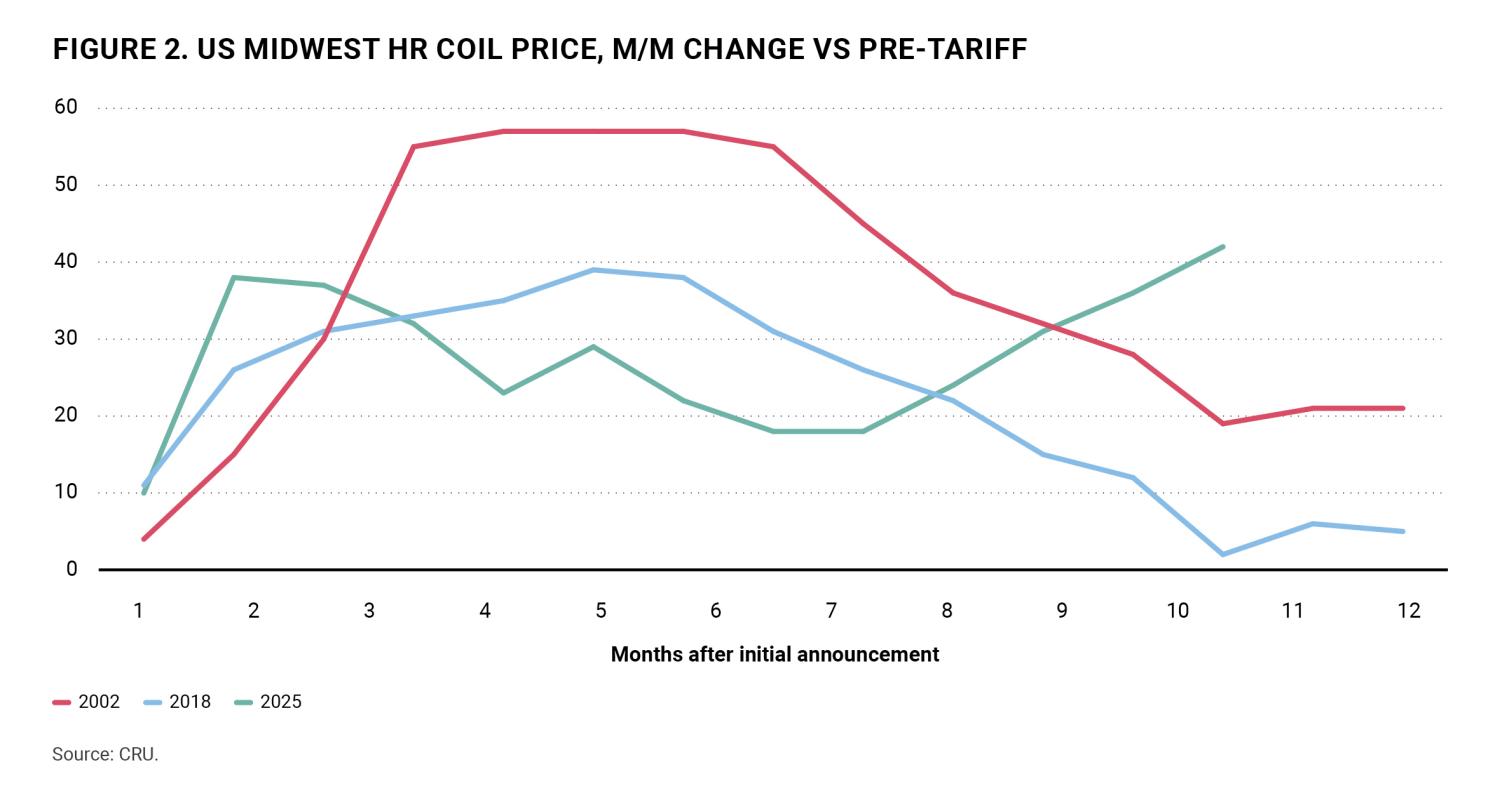

As a response to the bankruptcy of several U.S. steel producers, President George W. Bush turned to S201 to impose a three-year tariff of up to 30% on steel imports against most countries in March 2002. Due to the North American Free Trade Agreement, Canada and Mexico were exempt from these tariffs.12 These global tariffs were officially rescinded 20 months later in December 2003.13

In 2018, President Donald J. Trump turned to S232, which requires a finding that there is a threat to U.S. national security,14 to impose tariffs of 25% on imports of all steel. As part of the 232 investigation, national security was defined in terms of steel used in military products such as tanks and aircraft carriers as well as steel use in bridges, energy transmission, and more. The administration’s goal was to support the U.S. steel industry in achieving a capacity utilization rate of 80% or higher, seen as the minimum rate required for the industry to operate sustainably and support national defense needs in the future.15

Canada and Mexico were granted temporary exemptions from these 232 steel tariffs for nearly three months, and in May of 2019, they were granted a full exemption in the negotiations leading up to the USMCA trade agreement.16 Following President Trump’s first term, President Biden largely kept the S232 steel tariffs in place for most countries. The exception to this was tariff rate quotas put in place for the EU, Japan, and U.K. where a specified level of imports could come in without the S232 tariff.17 Yet, in February 2025, President Trump reinstituted the S232 steel tariffs and eliminated all country-specific exclusions, including for Canada and Mexico.18 Further, in June 2025, the 25% S232 tariff was increased to 50% for all countries. In addition to this 50% tariff rate, the reinstated S232 tariffs allowed for other, derivative products to be included rather than a process to request for exclusions.19 This has led the S232 tariffs to be applied further downstream to the steel content of imported products including bolts, bulldozers, and packaged products such as cans of shaving cream.20

This imposition of steel tariffs on Canada and Mexico has had dramatic effects on the interconnected North American steel supply chain and end users. Perhaps the most visible example of this is the automotive supply chain. High quality steel is produced in all three countries. Some of this is sent to stamping facilities for use in parts of the automotive body such as the hood or doors. Other steel is processed and assembled across multiple vendors to produce small components that traverse the border multiple times and go into larger parts, such as a rear underbody assembly.21 Due to the interconnectedness and overall growth of the North American market since the North American Free Trade Agreement went into effect in January 1994, investment in the production and processing of steel as well as downstream manufacturing of goods have grown across Canada, Mexico, and the U.S. One example for steel is ArcelorMittal’s Calvert mill near Mobile, Alabama. With over 5 million tons of rolling capacity, this facility was built in 2010 to not only support the Southeastern U.S. market, but also automotive steel demand in Mexico.22

These reinstituted S232 tariffs have led automotive manufacturers redirecting their network of suppliers to increase sourcing of U.S. produced steel. This shift in sourcing has led to higher compliance and sourcing costs, lower profits, and less diversity of supply.23 A lack of supply diversity is often a key risk for manufacturers as an unexpected outage can quickly disrupt manufacturing output. Steel mills can experience sudden issues with the operation of their furnace or supply of key industrial inputs. In 2005, Hurricane Katrina caused extensive damage to an industrial gas complex which severely limited the supply of liquid hydrogen used in the production of galvanized steel.24 In 2008, a steel mill in Dearborn, Michigan experienced an explosion at a blast furnace.25 Both instances immediately created a shortage of material forcing steel buyers to slow operations until their supply of steel could be restored.

Recommendation: Limit disruptive steel imports from outside the North American market

Growth of manufacturing has been and will remain a key focus of North American political leadership as manufacturing supports domestic jobs on the shop floor, at suppliers, as well as in downstream processing, packaging, and service providers. For manufacturing output to be successful and grow domestically, businesses require an adequate supply of three things: competitively priced energy, labor, and materials. Without any one of these, manufacturing will be incentivized to offshore or outsource noncompetitive components.

Steel prices will also impact construction. At CRU, we estimate that over a variety of construction projects with varying steel intensities, steel represents approximately 15% of the total cost.26 The more competitively priced steel is, the more overall projects can take place, leading to higher economic output. This is particularly apparent with government-funded infrastructure projects which are often used to support economic activity at the local or federal level. This can include the replacement of critical infrastructure such as bridges or the development of new highways, airport terminals, or electrical transmission and distribution systems. In this instance of publicly funded infrastructure spending, once a plan is approved and money allocated, the more that materials such as steel cost, the fewer projects get built.

Construction27 and manufacturing28 in North America are economic multipliers as spending and investment in these sectors generate significantly more economic activity than the initial amount spent. These two categories combined provide nearly $3 per every $1 invested through a combination of direct, indirect, and induced spending. Direct spending includes items such as materials, equipment, and labor to build and run the facility. Indirect spending represents money spent in the downstream supply chain to support the construction and operation of the site or facility. While induced spending is money spent from wages earned from the direct and indirect sectors.

Policymakers today can support economic growth via these industries through ensuring the upstream supply chain that includes steel is profitable for producers yet competitive enough to support the downstream users in construction and manufacturing. Due to the cyclical nature of steel demand, steel producers may not be profitable every quarter, but a profitable base of steel supply in Canada, Mexico, and the U.S. is required to support economic activity as well as national defense.

In the 2026 USMCA Joint Review, policymakers can support domestic steel production across the wider North American market. To do this, the U.S. should unwind the steel tariffs on Canada and Mexico and limit their scope. The current tariffs raise the domestic steel price, which has had negative impacts on investment and the competitiveness of domestic manufacturing, as well as overall construction output.29 A balance must be found that supports not only domestic producers, but also steel consumers across the wider construction and manufacturing industries. Therefore, the S232 steel tariffs should be reformed to ensure a competitive supply of steel is available to North American users with some tariffs remaining on steel imports from hyper competitive markets such as those in and around China that are influenced by over production and government-led financial assistance.30

While limiting imports from markets outside of North America, policymakers should return to a path towards minimal barriers of steel trade within the North American region. This recommendation could take shape in a variety of ways from an initial quota of low to no S232 tariffs to going back to a full regional exclusion from S232. This type of policy would not restrict domestic producers from filing an AD/CVD trade case if there is dumping.

To do this, Canada, Mexico, and the U.S. would need to align trade policy on material inputs such as steel, among other key materials. If this long-term trade support is provided, it will incentivize new technologically advanced steel mill investment across the region. This alignment has already started to come about as both Canada and Mexico have brought about stricter trade restrictions in the past year. These protections include lower quotas on steel imports from non-free trade agreement countries and tariffs on steel-derivative products.

In time, it will lead to more competitive steel supply and costs that can then support construction and manufacturing segments as well as the jobs that go along with these industries.

Author

-

Footnotes

- Ali Hasanbeigi, Steel Climate Impact 2025: An International Benchmarking of Energy and GHG Intensities (Global Efficiency Intelligence, 2025), https://www.globalefficiencyintel.com/steel-climate-impact-2025-an-international-benchmarking-of-energy-and-ghg-intensities/

- Timna Tanners, remarks at the Steel Market Update Steel Summit, August 2025

- ”Global Trade Tracker,” https://www.globaltradetracker.com

- End use share of steel demand in North America: CRU.

- U.S. Census Bureau, “Construction Spending” (Value of Construction Put in Place Survey), https://www.census.gov/construction/c30/c30index.html

- Josh Spoores and Gregor Spilker, “Record Prices Further Enhance Adoption of CME Group’s HRC Steel Futures Contract,” Insight (CRU International Ltd. and CME Group, April 22, 2021), https://www.cmegroup.com/content/dam/cmegroup/education/files/record-prices-further-enhance-adoption-of-hrc-steel-futures-contract.pdf

- Sandy Williams, “Ross Defends 232 While USW Clamors for Action,” Steel Market Update, November 15, 2017, https://www.steelmarketupdate.com/2017/11/15/ross-defends-232-while-usw-clamors-for-action/

- U.S. International Trade Commission, “USITC Makes Determination in Five-Year (Sunset) Reviews Concerning Aluminum Wire and Cable from China,” News Release 25-068, May 29, 2025, https://www.usitc.gov/press_room/news_release/2025/er0529_67064.htm

- U.S. Department of Commerce, International Trade Administration, Enforcement and Compliance, “Certain Cut-to-Length Carbon Steel Plate From the People’s Republic of China: Continuation of Antidumping Duty Order,” Federal Register 86, no. 124 (July 1, 2021): 35064–35065, https://www.federalregister.gov/documents/2021/07/01/2021-14054/certain-cut-to-length-carbon-steel-plate-from-the-peoples-republic-of-china-continuation-of

- “Proclamation 5050—Temporary Duty Increase and Tariff-Rate Quota on the Importation Into the United States of Certain Heavyweight Motorcycles,” April 15, 1983, The American Presidency Project, https://www.presidency.ucsb.edu/documents/proclamation-5050-temporary-duty-increase-and-tariff-rate-quota-the-importation-into-the

- “Proclamation 4210—Modifying Proclamation No. 3279 Relating to Imports of Petroleum and Petroleum Products,” January 23, 1975, The American Presidency Project, https://www.presidency.ucsb.edu/documents/proclamation-4210-modifying-proclamation-no-3279-relating-imports-petroleum-and-petroleum

- “Proclamation 7529—To Facilitate Positive Adjustment to Competition From Imports of Certain Steel Products,” March 5, 2002, The American Presidency Project, https://www.presidency.ucsb.edu/documents/proclamation-7529-facilitate-positive-adjustment-competition-from-imports-certain-steel

- The White House, “President’s Statement on Steel,” December 4, 2003, https://georgewbush-whitehouse.archives.gov/news/releases/2003/12/20031204-5.html

- Kyla H. Kitamura, “Section 232 of the Trade Expansion Act of 1962,” In Focus IF13006 (Congressional Research Service, July 16, 2025), https://www.congress.gov/crs-product/IF13006

- Federal Register, “Adjusting Imports of Steel into the United States,” March 15, 2018, https://www.federalregister.gov/documents/2018/03/15/2018-05478/adjusting-imports-of-steel-into-the-united-states

- Office of the United States Trade Representative, “United States Announces Deal with Canada and Mexico to Lift Retaliatory Tariffs,” May 17, 2019, https://ustr.gov/about-us/policy-offices/press-office/press-releases/2019/may/united-states-announces-deal-canada-and

- Joseph R. Biden Jr., “Proclamation 10328 of December 27, 2021: Adjusting Imports of Steel Into the United States,” Federal Register 87, no. 1 (January 3, 2022), https://www.federalregister.gov/documents/2022/01/03/2021-28516/adjusting-imports-of-steel-into-the-united-states; Joseph R. Biden Jr., “Proclamation 10356 of March 31, 2022: Adjusting Imports of Steel Into the United States,” Federal Register 87, no. 63 (April 1, 2022), https://www.federalregister.gov/documents/2022/04/01/2022-07136/adjusting-imports-of-steel-into-the-united-states; Joseph R. Biden Jr., “Proclamation 10406 of May 31, 2022: Adjusting Imports of Steel Into the United States,” Federal Register 87, no. 107 (June 3, 2022): 33591–33606, https://www.govinfo.gov/content/pkg/FR-2022-06-03/pdf/2022-12108.pdf

- “Proclamation 10896—Adjusting Imports of Steel Into the United States,” February 10, 2025, The American Presidency Project, https://www.presidency.ucsb.edu/documents/proclamation-10896-adjusting-imports-steel-into-the-united-states

- “Proclamation 10947—Adjusting Imports of Aluminum and Steel Into the United States,” June 3, 2025, The American Presidency Project, https://www.presidency.ucsb.edu/documents/proclamation-10947-adjusting-imports-aluminum-and-steel-into-the-united-states

- Bureau of Industry and Security, U.S. Department of Commerce, “Department of Commerce Adds 407 Product Categories to Steel and Aluminum Tariffs,” press release, August 19, 2025, https://www.bis.gov/press-release/department-commerce-adds-407-product-categories-steel-aluminum-tariffs

- Sabri Ben-Achour, “When It Comes to NAFTA and Autos, Parts Are Well-Traveled,” Marketplace, March 24, 2017, https://www.marketplace.org/story/2017/03/24/when-it-cones-nafta-and-autos-parts-are-well-traveled/

- Jeff Amy, “Next Challenge for ThyssenKrupp,” AL.com (Press-Register Business), December 2010, https://www.al.com/press-register-business/2010/12/next_challenge_for_thyssenkrup.html

- Michael Wayland, “GM Lowers 2025 Guidance, Citing Up to $5 Billion in Tariff Exposure,” CNBC, May 1, 2025, https://www.cnbc.com/2025/05/01/gm-2025-guidance-tariffs.html

- Steel Dynamics, Inc., “Steel Dynamics Addresses Hydrogen Gas Supply Issues,” press release, September 2, 2005, Exhibit 99.1, U.S. Securities and Exchange Commission (EDGAR), https://www.sec.gov/Archives/edgar/data/1022671/000112528205004669/b408688ex_99-1.htm

- Sean Delaney, “Steel Plant Explosion Injures One,” The News-Herald, January 8, 2008, https://www.thenewsherald.com/2008/01/08/steel-plant-explosion-injures-one/

- CRU estimates.

- Brian Lewandowski, Adam Illig, Ethan Street, and Richard Wobbekind, Economic Impacts of Commercial Real Estate, 2025 U.S. Edition (Herndon, VA: NAIOP Research Foundation, January 2025), https://www.naiop.org/globalassets/research-and-publications/report/economic-impacts-of-commercial-real-estate-2025-us/2025-economic-impacts-of-cre.pdf

- For every $1.00 spent in manufacturing, there is a total impact of $2.64 to the overall economy. National Association of Manufacturers, “Facts About Manufacturing: The Top 18 Facts You Need to Know,” sec. 2, https://nam.org/mfgdata/facts-about-manufacturing-expanded/

- Tim Triplett, “New Infrastructure Spending Bill Could Add 3% to Steel Demand,” Steel Market Update, August 13, 2021, https://www.steelmarketupdate.com/2021/08/13/new-infrastructure-spending-bill-could-add-3-to-steel-demand/

- OECD, OECD Steel Outlook 2025 (Paris: OECD Publishing, 2025), https://doi.org/10.1787/28b61a5e-en

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).