Studies in this week’s Hutchins Roundup find that the expectation of hitting effective lower bound makes achieving the target rate more difficult, loss carryback stimulus does not always increase firm investment, and more.

The expectation of hitting effective lower bound causes inflation to undershoot the target rate

Using an empirical model calibrated to the U.S. economy, Timothy Hills of New York University, Taisuke Nakata of the Federal Reserve Board, and Sebastian Schmidt of the European Central Bank find that the possibility of dropping the policy interest rate to zero or slightly below has consequences for the economy – even when rates are well above zero. Specifically, they find that the risk of hitting the lower bound causes inflation to fall below the 2 percent target by about 20 basis points. Achieving the inflation target may be more difficult now than before the Great Recession if recent experience has led households and firms to view zero interest rates as more likely to occur in the future than previously expected.

Firms’ responses to countercyclical tax breaks vary greatly with macroeconomic conditions

Christine Dobridge of the Federal Reserve Board examines the effects of tax policies enacted in 2002 and 2009 that allowed firms to accelerate tax refunds (by increasing the net operating loss “carryback” window). In the shallow 2002 recession, firms allocated 40 cents of every $1 in additional tax refunds to investment around the world. In the deep 2009 recession, they used 96 cents of every $1 to increase cash holdings, which reduced the risk of bankruptcy. The tax break had no effect on unemployment in either instance, she finds.

Increased spending on education leads to improvements in student achievement

Using nationally representative data, Julien Lafortune and Jesse Rothstein of University of California, Berkeley, and Diane Whitmore Schanzenbach of Northwestern University (and Brookings’ Hamilton Project) find that post-1990 school finance reforms raised spending in low-income districts by over $500 per pupil per year, leading to increases in test scores in low-income districts relative to high-income ones. They also find that the reforms were cost effective, as future earnings increased more than the additional education spending. However, they found that, because the average low-income student does not live in a low-income district, these school reforms were not effective at reducing the achievement gaps between high and low-income students.

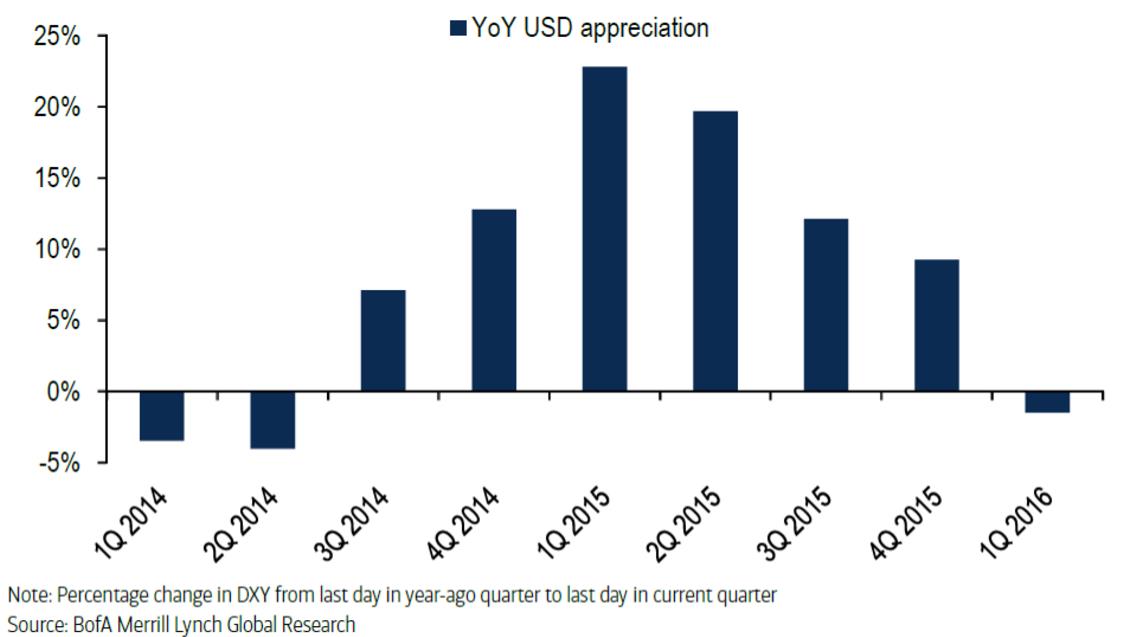

Chart of the week: Appreciation of the US dollar might be coming to an end

DXY is an index that measures the U.S. dollar’s value relative to six currencies: the euro, Japanese yen, Canadian dollar, British pound, Swedish krona and Swiss franc.

Quote of the week: “[I]t is possible for small open economies bordering a large currency area to pursue an independent monetary policy,” says Swiss central banker Thomas Jordan

“[C]an countries bordering a major currency area pursue an independent monetary policy – and have events since the onset of the financial crisis in 2008 affected the answer? And…how have unconventional measures helped these countries in the implementation of an independent monetary policy?…[T]he first question…can essentially be answered with a yes. However, for these countries, managing monetary conditions arising from interest and exchange rate levels has become significantly more difficult in recent years. Regarding the second question…negative interest, foreign exchange market interventions and quantitative easing programs – instruments each tailored to suit a country’s specific needs – have helped these central banks to regain a certain room for maneuver. But…when major disruptions occur, central banks cannot always keep inflation and growth stable within a targeted range.”

— Thomas Jordan, Chairman of the Governing Board, Swiss National Bank

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Hitting inflation target, countercyclical tax breaks, and more

February 25, 2016