Studies in this week’s Hutchins Roundup find that the high school remedial education increases earnings, investors demand dividend-paying assets when interest rates are low, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

High school remedial education programs increase educational attainment and earnings

In 1999, the Israeli government introduced a remedial education program for underperforming high school students (10th to 12th grade). By comparing students at schools that participated in the program in 1999 with similar students at schools that started participating the following year, Victor Lavy of the University of Warwick, Assaf Kott of Brown University, and Genia Rachkovski of Northwestern University show that the program improved long-term outcomes. In particular, it boosted enrollment in post-secondary education by 13.6 percentage points and earnings at age 33 by 4 percent, with larger impacts for students from poorer families. The authors estimate that the Israeli government recouped the $1,100 per participant cost of the program within 7-8 years through higher income tax collections on participants’ increased earnings, meaning that, over time, the program more than paid for itself.

Low interest rates increase demand for high dividend-paying equities

A large body of popular retail investment advice advocates living off investment income while keeping the principal untapped. But in a low interest rate environment, investors following this recommendation may have difficulty sustaining their consumption because interest from bank deposits and bonds is depressed. Analyzing the portfolio holdings of 19,394 brokerage accounts from 1991-2016, Ken Daniel and Kairong Xiao of Columbia University and Lorenzo Garlappi of the University of British Columbia find that, when interest rates are low, investors “reach for income” by reallocating their portfolio toward high-dividend assets. In particular, a 1 percent decrease in the Fed Funds rate leads to a 5 percent increase in investments in high-dividend mutual funds over a period of three years. This reallocation effect is particularly strong for retirees, who rely on investment payouts as their primary source of income. The authors conclude that monetary policy can influence the demand for high-dividend paying assets, potentially distorting asset values and risk-taking behavior.

The Great Recession increased Social Security Disability Insurance applications

Participation in the Social Security Disability Insurance (SSDI) program, which pays a monthly benefit to unemployed adults with severe, long-lasting disabilities, expanded sharply during the Great Recession. Nicole Maestas of Harvard Medical School, Kathleen J. Mullen of the RAND Corporation, and Alexander Strand of the Social Security Administration use variation in the timing and severity of the recession across states to assess whether the growth is due to policy changes or declining labor market opportunities for low-skilled workers. They find that nearly a million people applied for SSDI benefits because of the Great Recession, accounting for 12 percent of all applicants from 2008 to 2012. Nine percent of these applicants were accepted because of severe impairments, 33 percent were accepted despite less severe impairments because they lacked transferable skills to get a new job, and the remaining 58 percent were rejected. On average, people who applied because of the recession were 53 years old and had less severe impairments than other applicants. These findings suggest that labor market opportunities played an important role in increasing SSDI applications and enrollment. Because people on SSDI rarely go back to work full-time, this corresponds to a near permanent decline in the economy’s productive capacity, the authors say.

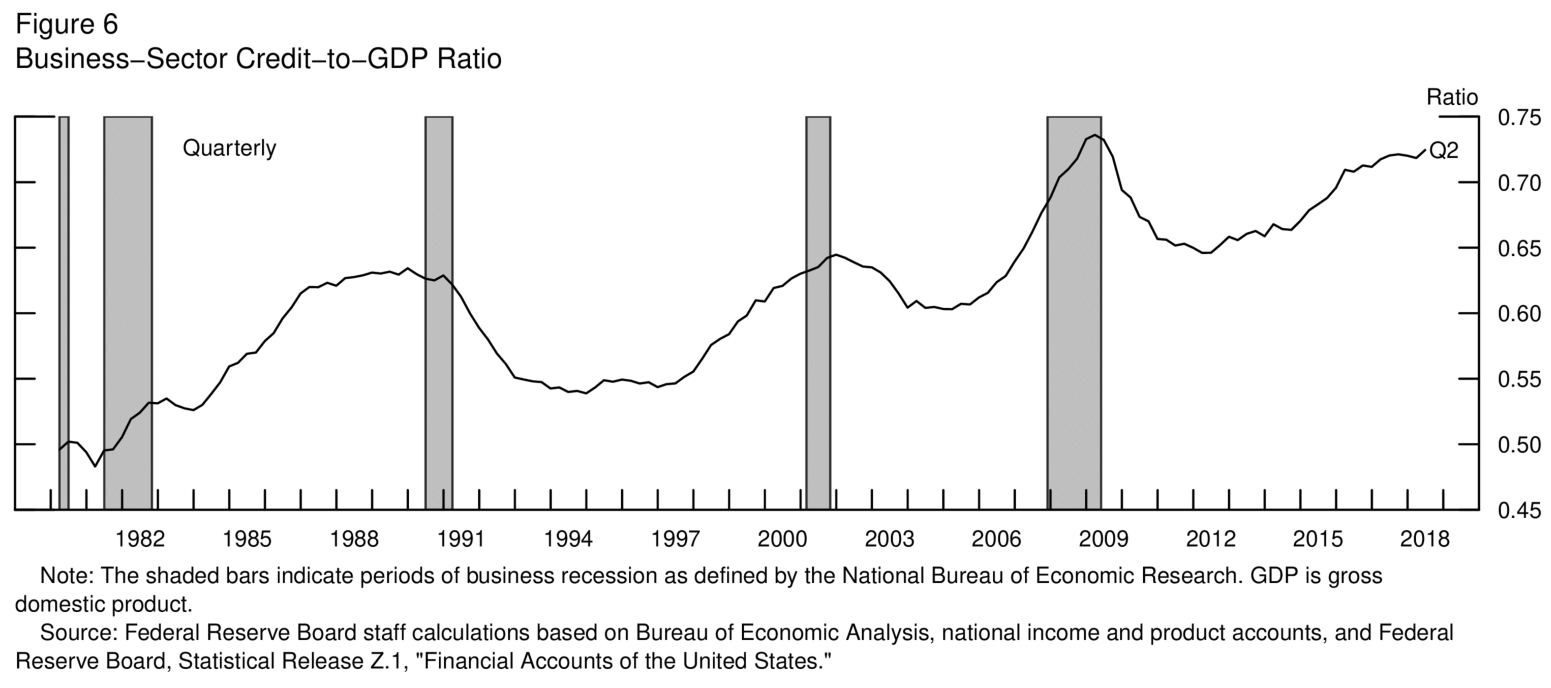

Chart of the week: The ratio of business sector credit-to-GDP almost back to an all-time high

Quote of the week:

“We know the fiscal stimulus, in our projection, is likely to wane. The impact of it is going to wane as we head into 2019. We know the Fed has raised interest rates eight times over the last 2.5 to 3 years, and we know there is some lag effect for that to take hold. We know we’re allowing the balance sheet to run down. We know global growth is decelerating somewhat. We know some interest-rate sensitive sectors, not widespread yet, but some like housing are showing some weakness—too soon to know what to make of it. And by my reading of corporate earnings reports and my discussions with businesses and CEOs, there’s no question that we’re seeing higher input costs, not just tariff-related but also labor-related, other input costs. And the ability of businesses to pass those higher input costs onto their customers is very mixed. Some can and some can’t. So you’re seeing some margin challenges,” says Robert Kaplan, president of the Federal Reserve Bank of Dallas.

“When you wrap all those things up together—and then you’ve got trade tensions and trade uncertainty which we know about. So my own experience over my career is when you see a reasonably long list of some uncertainties, it doesn’t mean those uncertainties won’t get resolved constructively, but it tends to likely create some more [financial market] volatility. The other thing I’d comment on is while this volatility is a lot higher than certainly we experienced last year, I think historically the aberration was how low the volatility was last year. Some higher level of volatility is not unusual, and certainly in my career, it’s not unusual.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

{kind=link}

Commentary

Hutchins Roundup: High school remedial education, demand for dividend-paying assets, and more

December 13, 2018

Studies in this week’s Hutchins Roundup find that the high school remedial education increases earnings, investors demand dividend-paying assets when interest rates are low, and more.