ECB’s purchase of troubled sovereign debt worked primarily by boosting confidence

Michiel De Pooter of the Federal Reserve Board, Rebecca DeSimone of Columbia University, Robert F. Martin of Barclays Capital, and Seth Pruitt of Arizona State University find that the European Central Bank’s purchase of troubled countries’ sovereign debt beginning in 2010 had little to no impact on yields or spreads at the time of purchase, but did have large effects at the time of announcement. This suggests that the ECB’s Securities Market Program impacted yields and spreads by raising confidence, rather than through any direct purchase effect.

Temporary incentives promote longer-term improvements

Pablo Celhay of the University of Chicago, Paul Gertler of the University of California, Berkeley, and Paula Giovagnoli and Christel Vermeersch of The World Bank find that medical clinics that were offered temporary financial incentives to provide first trimester prenatal care were 34% more likely to provide those services, an effect persisting at least 2 years after the incentives expired. This suggests that temporary incentives may be effective in overcoming institutional inertia and improve outcomes at a much lower cost than permanent incentives.

Declining unionization and erosion of minimum wage worsen income inequality

Florence Jaumotte and Carolina Osorio Buitron of the International Monetary Fund find that the decline in unionization and the erosion of minimum wages in advanced economies have been associated with an increase in income inequality. The authors argue that de-unionization can increase inequality by increasing the share of capital income (which tends to be concentrated among higher earners) and by reducing workers’ influence on business decisions, including executive compensation.

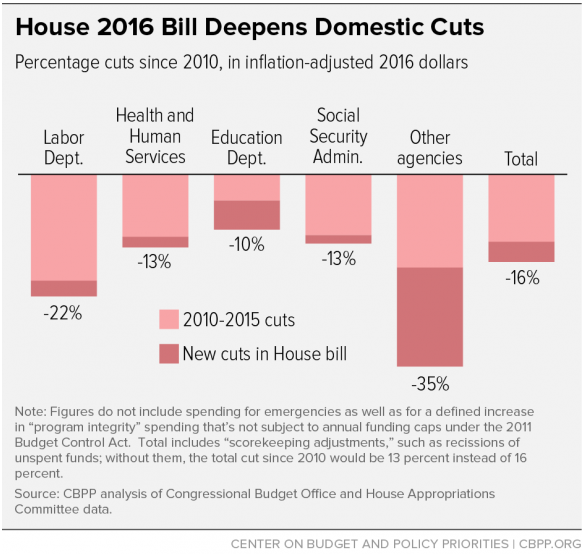

Chart of the week: House Budget

Quote of the week: Cleveland Fed’s Mester: “timing isn’t everything”

While financial market participants are particularly focused on the timing of the first rate increase, when it comes to monetary policy, timing isn’t everything. The FOMC meets eight times a year, and the difference in lifting off from a zero interest rate a meeting or two earlier or later is not significant. More important for macroeconomic performance is the expected path of policy beyond liftoff because expectations about the future path of policy can affect today’s economic decisions.

—Loretta J. Mester, President and CEO of the Federal Reserve Bank of Cleveland

Glenn Hutchins, vice chair of the Brookings board of trustees and a director of the New York Fed, defends the Fed’s structure, including private-sector boards of regional Fed banks, as an “exquisite balance that has served the country so well.”

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: ECB sovereign bond purchases, temporary incentives, and more

July 23, 2015