The Vitals

Housing today consumes a larger share of

Americans’ incomes than 20 years ago, due in part to increasingly strict local

and state regulations and a declining share of eligible households receiving federal housing assistance, which leaves them with less

to cover the costs of food, healthcare, transportation, and other necessities.

-

The poorest 20 percent of American families cannot afford rent on standard apartments without some subsidy from the government.

-

Nearly half of American households that rent spent more than 30 percent of their income on rent in 2017.

-

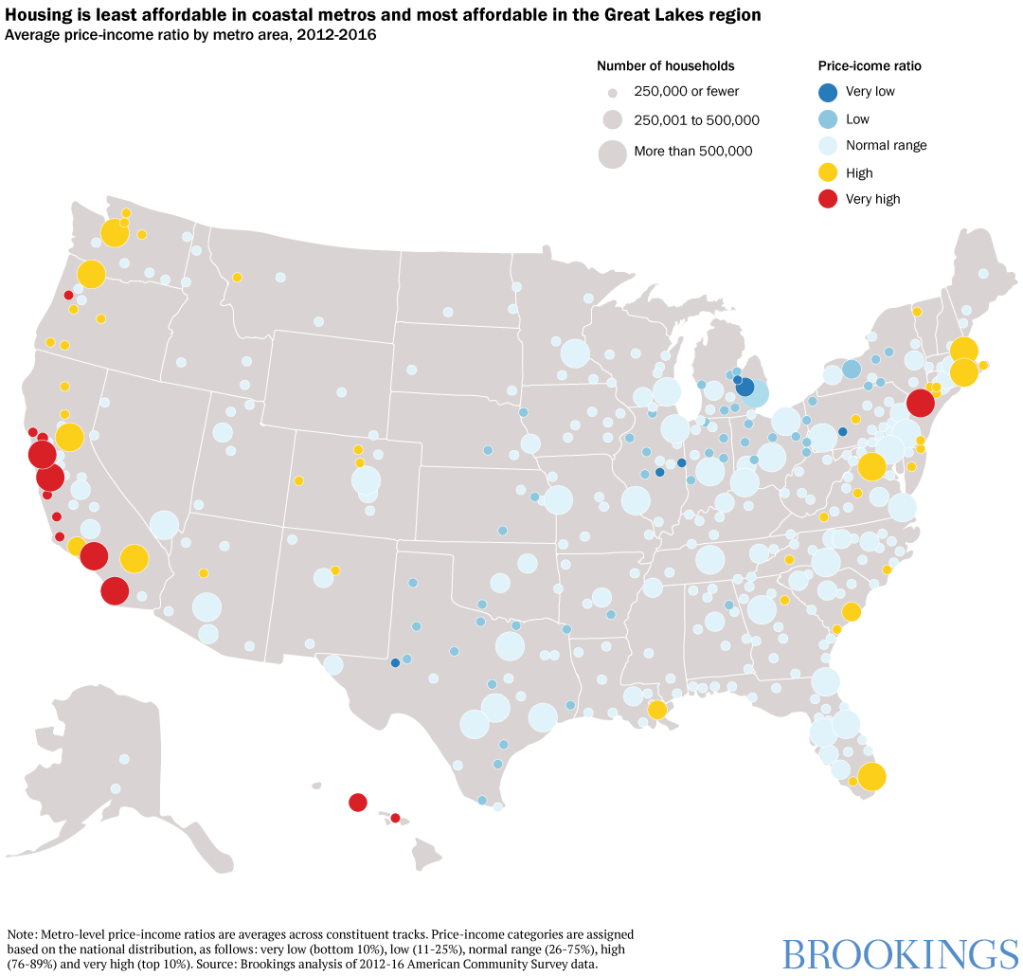

Median home prices are more than six times median incomes for communities in coastal California, much of the Northeast, and South Florida.

A Closer Look

Housing

affordability is shaping up to be one of the kitchen-table issues drawing substantial

attention in the 2020

presidential campaign. So far several Democratic

candidates have proposed plans to address the problem, and the White

House recently

issued an Executive Order to delve into one cause of rising housing

costs.

Q. What’s the problem?

We commonly measure

housing affordability as the share of a person’s income that is spent on

monthly rent or mortgage payments. Based on the U.S. Department of Housing and

Urban Development’s (HUD) definition,

anyone who spends more than 30 percent of household income on housing is “cost

burdened” and anyone who spends more than 50 percent is “severely burdened.” Households

that devote a very large share of income to housing may not have enough

left over to cover the costs of food, healthcare, and

transportation.

While any individual or family with a low income may face challenges, relative to local housing prices, an affordability crisis implies that this is a problem for large numbers of households. In 2017, nearly half of renter households spent more than 30 percent of income on rent, which is an increase from 40 percent of households in 2001. Even among middle-income households, housing consumes a larger share of income than 20 years ago.

Housing affordability varies widely across the United States. The map below shows another measure of affordability for metropolitan areas: the median home price divided by the median household income. For the entire country, median home prices are roughly three times median income. But in coastal California, much of the Northeast, and South Florida, median prices are more than six times median incomes. In the Midwest and many smaller metros in the Heartland, prices are less than twice median incomes.

Q. Why is housing less affordable for many families than was the case 20 years ago?

The United

States has two separate housing affordability problems. First, the poorest 20

percent of families everywhere cannot afford minimum quality housing: their

incomes are too low to cover the rent on standard apartments without

some subsidy from the government. The challenge for poor families has gotten

worse over the past few decades as the share of eligible households receiving federal

housing assistance has declined. Second, increasingly strict local

government regulations have driven up the cost of building new homes

in many large metro areas along both the East and West Coasts. Because of these

regulations, housing supply has not kept pace with demand, leading to

increasingly higher prices.

Q. Isn’t this a local government issue? What’s the federal government’s role?

Decisions over

land use—what types of housing can be built in which locations—are largely made

by state and local governments. One of the most common zoning laws that drives

up housing costs is restricting the development

of apartments. Because apartments use less land per housing unit

than single-family homes, they are the most affordable form of housing. Yet

communities across the United States have effectively banned

apartments from being built in most neighborhoods—even large cities

like Los Angeles and Seattle prohibit apartments on 75 percent of land. Other

zoning tools, like caps on building

height, minimum

lot sizes, and parking

requirements, also increase the cost of housing. The development

process itself has become increasingly long,

complicated, and risky over the past 20 years—all factors that drive

up the cost of newly built housing and limit the market’s ability to respond to

demand.

But federal

policies also influence the cost of construction through several channels. Construction

materials such as lumber and steel are subject to U.S. tariffs and trade

policy. Immigration

policy affects the availability of workers;

about one-quarter of

construction workers are foreign born. The cost and availability of mortgage

loans depends on monetary

policy set by the Federal Reserve, as well as lending

guidelines set by public and quasi-public agencies (Fannie Mae,

Freddie Mac, the Federal Housing Administration).

The most direct

way the federal government could relieve housing cost burdens on low-income

households is by giving them subsidies. Unlike food stamps or Medicaid, federal

housing subsidies are not an entitlement:

currently around one

in five eligible renter households receives federal assistance. Policies

that boost incomes—like the earned

income tax credit, the minimum wage, or a proposed universal

basic income—also help poor families pay for housing.

Q. What are consistent themes in this year’s presidential campaign proposals?

Three common

features have emerged among 2020 presidential candidates’ housing proposals:

alleviating housing cost burdens for low- and middle-income families,

addressing local regulatory barriers to supply, and mitigating the impacts of

past racially discriminatory policies.

Several candidates

have proposed establishing

new federal tax credits for renters. Conceptually similar to the mortgage interest

deduction for homeowners, these credits would refund some income

when renters file their federal taxes. One possible

concern with giving households more money to spend on rent is that, in places

like California with restrictive zoning, subsidies will just drive up rents.

That’s a less likely outcome in cities where housing is abundant or easy to

build, such as Houston or Detroit. The more households that receive subsidies—by

extending them further up the income scale, for example—the greater the likely

impact on housing prices.

There are also novel proposals for the federal government to use a combination of financial carrots and sticks to induce local governments to reform their zoning laws. The likely success depends on how big the financial incentives would be; the most exclusionary local governments tend to be wealthy suburbs that receive little funding directly from HUD. Tying federal transportation funds to zoning reform is potentially a more promising approach.

A number of candidates are explicitly framing their housing plans as responses to racially discriminatory policies of the past. Specifically, black households today have lower homeownership rates and overall wealth than white households due to historic redlining, the federal government’s practice of systematically denying mortgages to black applicants and black neighborhoods. One proposed solution is a new “baby bonds” program, a federal annual grant to families with children, with a sliding scale based on income. Other proposals include downpayment subsidies for people living in historically redlined communities and more rigorous enforcement of federal fair housing laws. These proposals essentially try to remedy racial disparities without explicitly using race. However, neither family income nor geography are perfectly correlated with race, making precise targeting of benefits difficult.

Author

Dig Deeper

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How can government make housing more affordable?

October 15, 2019