In June, we reported that Black and Hispanic Americans faced higher rates of housing hardship than white Americans, and we emphasized the importance of identifying a long-term rather than a “Band-Aid” solution. Now, almost six months later, with COVID-19 cases skyrocketing, no significant efforts have been taken to mitigate the situation. Additionally, a change in administration will bring more delays, making the risk of a major housing crisis even more real. To make matters even worse, data from our recent survey indicates that the impact of COVID-19 on homeowners not only still exists, but it has significantly worsened, especially among Black and Hispanic households and young adults.

We explored how housing hardships changed over time based on nationally representative survey samples from two waves of the Socioeconomic Impacts of COVID-19 Survey, administered by the Social Policy Institute at Washington University in St. Louis. The survey was administered in late April and early May (Wave 1) and late August (Wave 2) to over 5,000 nationally representative samples each time. To understand housing hardships over time, we focused on the following questions:

- Eviction/foreclosure: In the last three months, were you or anyone in your household forced to move by a landlord or bank when you did not want to?

- Rent and mortgage delinquency: In the last three months, did you or someone in your household not pay the full amount of the rent or mortgage because you could not afford it?

- Utility payment: In the last three months, did you or someone in your household skip paying a bill or paid a bill late due to not having enough money?

Data from our recent survey indicates that the impact of COVID-19 on homeowners not only still exists, but it has significantly worsened, especially among Black and Hispanic households and young adults.

Housing hardships increasing significantly among Hispanic and Black households

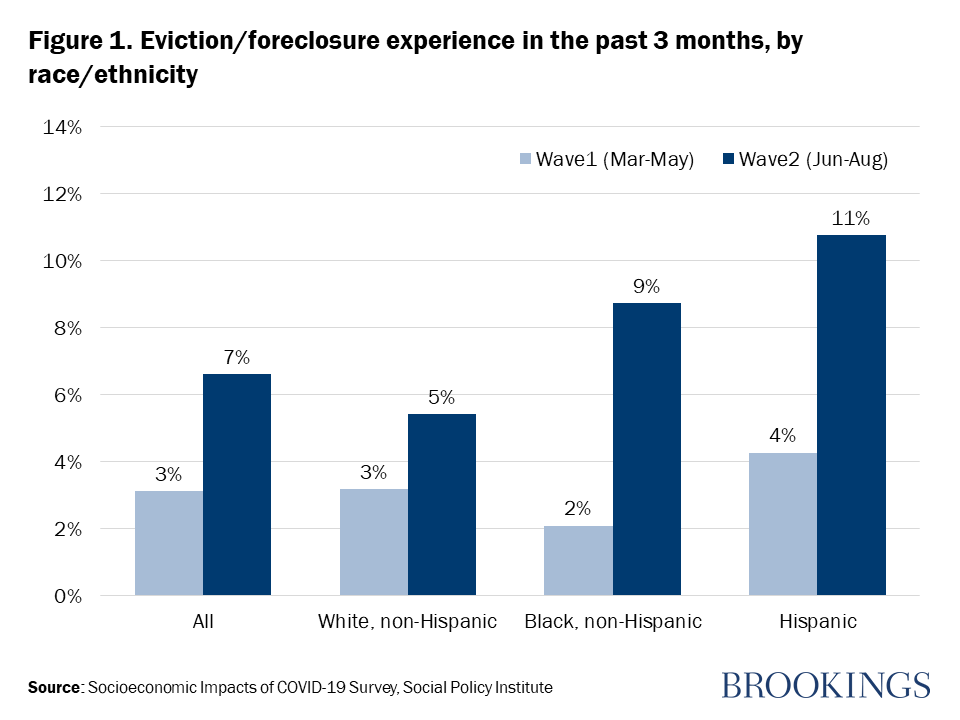

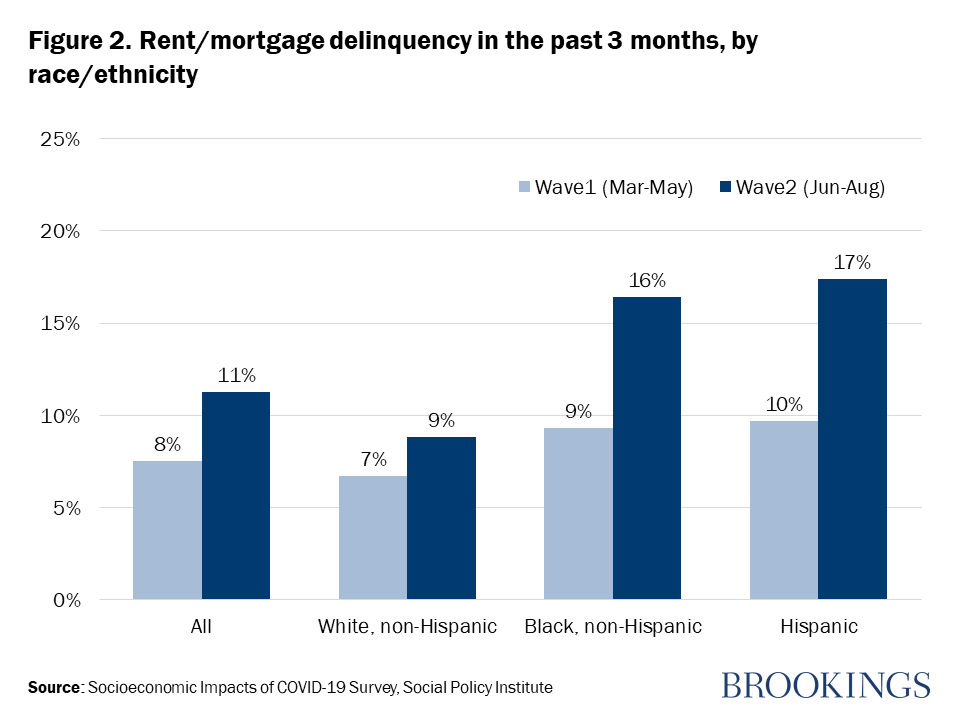

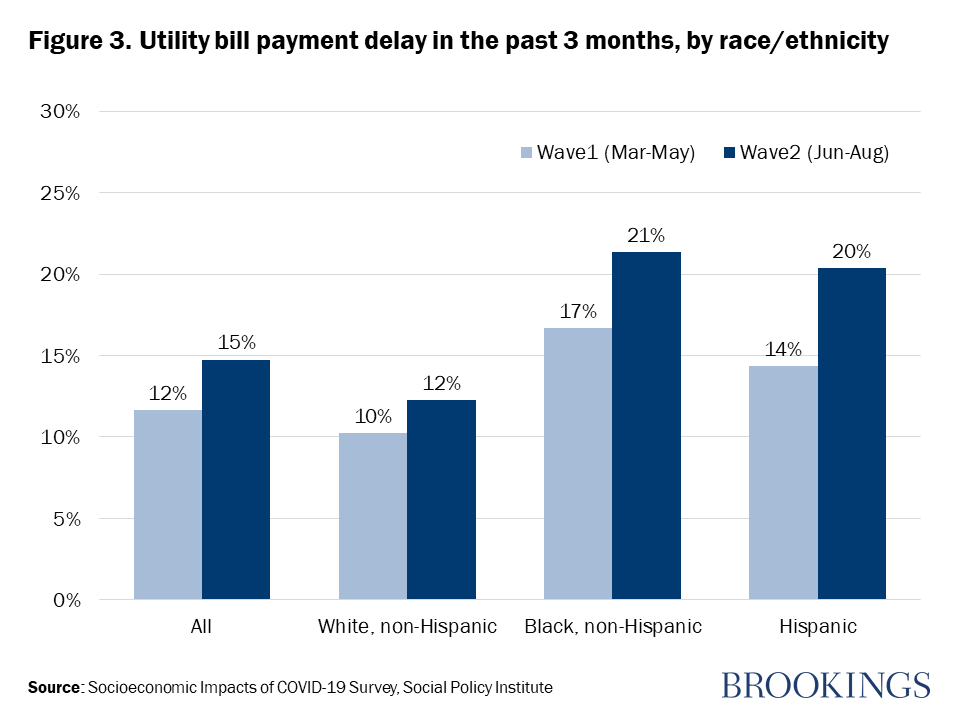

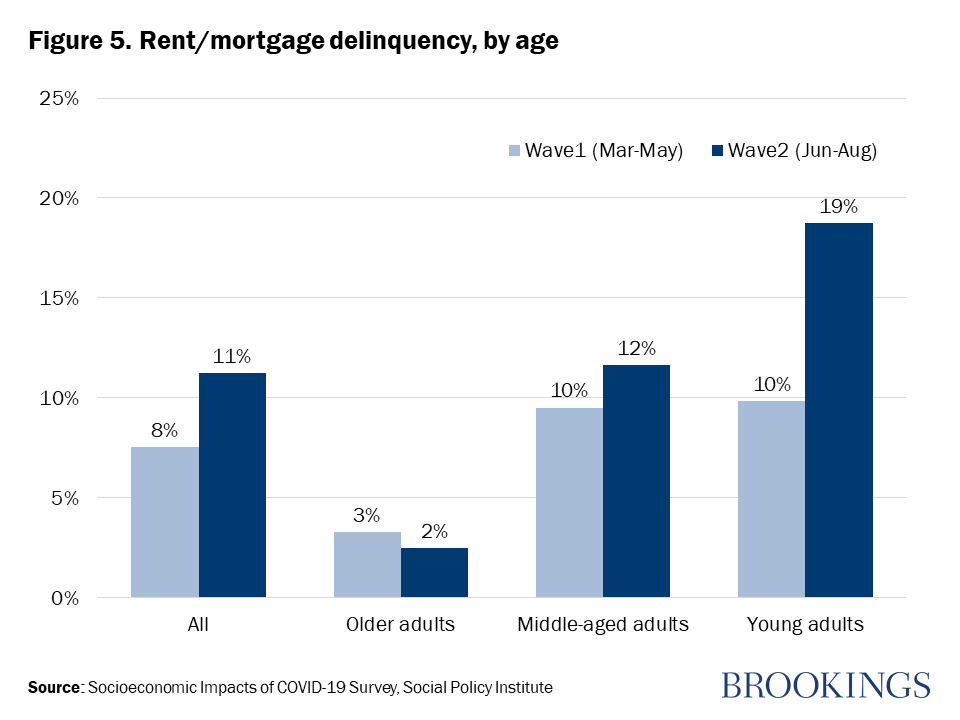

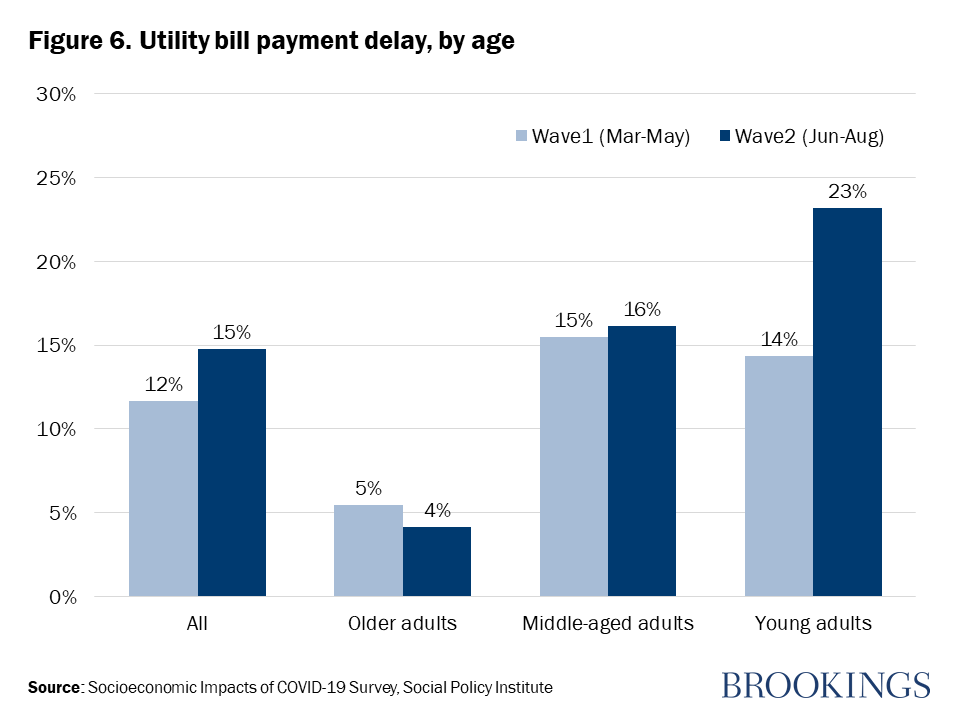

Strikingly, the eviction/foreclosure rates for all respondents doubled in August, mainly driven by Black and Hispanic households reporting higher evictions/foreclosures than white households (Figure 1). For example, the eviction/foreclosure rate of Black and Hispanic respondents increased by 7 percent as compared to only 2 percent among white respondents. Additionally, Black respondents were almost twice as likely to be forced to move than non-Hispanic white respondents in Wave 2, despite being least likely to be forced to move during Wave 1. While the jump in eviction risk among Black households is certainly alarming, Hispanic respondents maintain the highest vulnerability to eviction among the three groups both in Wave 1 and Wave 2. The trends of rent/mortgage delinquency (Figure 2) and other delayed bill payments (Figure 3) were similar to the eviction and/or foreclosure experience. The disproportionate housing-hardships across racial/ethnic groups widened as the pandemic was prolonged and will continue to widen if no action is taken.

Young adults more likely to face eviction/foreclosure and housing hardship than older adults

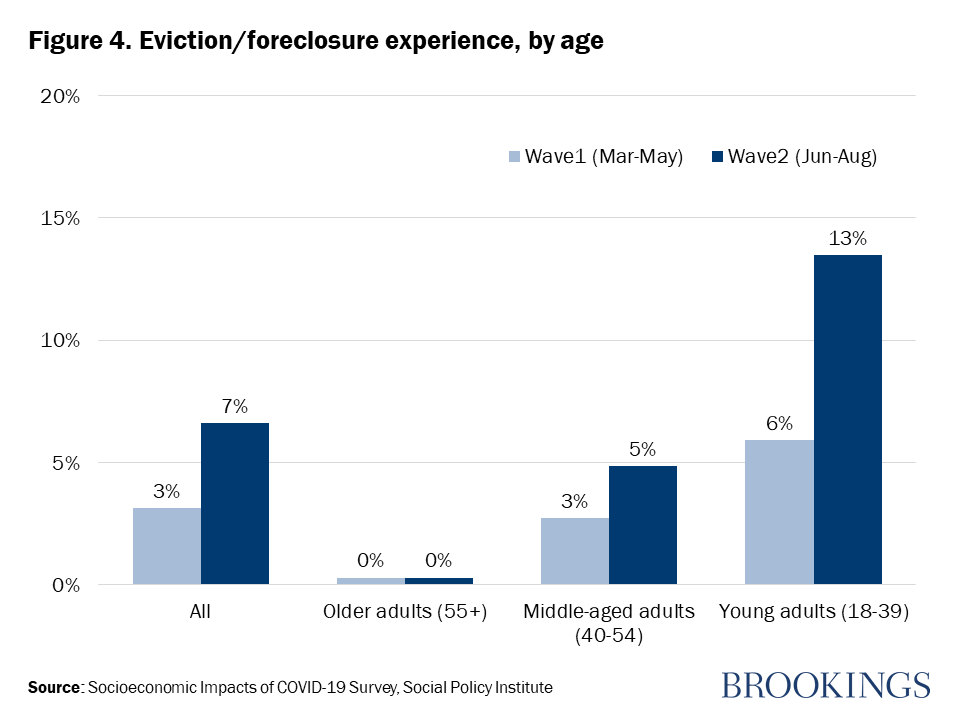

In addition to severe disparities in housing hardships based on race and ethnicity, we found a significant increase in hardship over time among young adults. In both survey waves, young adults (18-39 years old) were the most vulnerable to housing-related hardships, followed by middle-aged adults (40-54 years old), then older adults (55+ years old), and Wave 2 further widens the gap.

While a very small number of older adults reported housing-related hardship experiences during either wave of our survey, both middle-aged- and young adults faced more housing instability as the pandemic persisted. In particular, nearly twice as many young adults reported both eviction/foreclosure and mortgage/rent delinquency (or “payment” delay) in August as compared to May. This is compounding the financial situation of young adults who have had a shorter amount of time to accumulate protective financial assets, making it harder to weather the shock of the pandemic.

Policies must support long-term solutions that address racial and generational disparities

This situation could potentially widen the wealth gap for Black and Hispanic households, as well as young adults, and increase hardship for landlords. Additionally, Aspen Institute estimates that 30 million to 40 million people could lose their shelter when the eviction moratorium ends, exacerbating the situation for emergency shelters.

Despite the alarming trend in housing instability at the onset of the pandemic, the public sector provided short-term, ineffective solutions. Eviction moratoriums provided some relief, yet the current moratorium, which expires on December 31, does little to guarantee protections. Instead, this solution—merely an agreement declaration between tenants and landlords—postpones impending housing and financial disasters rather than eradicate problems renters may confront after the expiration, including paying back missed bills. Furthermore, this measure could exacerbate the risks for “mom and pop” landlords, exposing them to housing hardship, bankruptcy, or foreclosure due to an erosion of liquid assets. And our findings imply that housing resolutions did little to reduce the risks of financially vulnerable groups.

More proactive and sustainable remedies are needed. Solutions should also be oriented not only to highly pronounced groups, such as Black and Hispanic families, but also to obscure and less pronounced groups, including young adults and noncorporate landlords. A universal housing voucher for those with income below a certain level is an effective remedy. This not only secures stable income for landlords, it also drastically reduces evictions and homelessness, as well as widespread discrimination against voucher tenants.

Obviously, universal vouchers have a cost. Though the expenditure seems huge, it is far less than tax benefits for homeowners. The Office of Tax Analysis at the U.S. Department of Treasury estimates that the exclusion of imputed rent in 2020 reduced federal revenues by $126 billion. And we have the money; as of September 2020, the Department of Housing and Urban Development still has $134.5 billion that has not been allocated.

In addition to monetary costs, there’s a public perception challenge, too. Paying for universal vouchers requires public consensus that every member is related to one other, especially in the era of contagion. Every member of society is impacted by this housing situation. If Black and Hispanic families are unable to pay off their rent and mortgage, their financial risks shift to their landlords and mortgage lenders. If young adults are evicted, the coronavirus could spread rapidly to older generations. Indeed, stable shelter is not only a fundamental human need for individuals, but also an imperative tool for society to combat the spread of the coronavirus.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Housing inequality gets worse as the COVID-19 pandemic is prolonged

December 18, 2020