In 2016 the Center for Sustainable Economy (CSE) proposed a solution for addressing the market failures associated with construction and operation of fossil fuel infrastructure—fossil fuel risk bond (FFRB) programs. There are two broad categories of market failure associated with fossil fuel infrastructure—climate change, which is driven by the release of greenhouse gases (GHG) from this infrastructure, and the uncompensated physical and economic damages to land, air, and water that communities routinely experience associated with leaks, spills, accidents and abandonment of coal mines, oil and gas wells, pipelines, refineries, oil trains, LNG trains, and fossil fuel export terminals.

Excluding such costs in the retail prices of fossil fuels distorts markets and represents an implicit subsidy that leads to overconsumption relative to renewable forms of energy. The International Monetary Fund estimates that implicit fossil fuel subsidies amount to roughly $5 trillion per year. By 2100, the White House, citing figures from Network for Greening the Financial System, predicts a hit on US GDP in the order of 3 – 10% by the end of the century, from the physical and financial effects of climate change and responsive policies. FFRB programs are tools that regulators can use to begin to address these externalized costs. They consist of two primary approaches operationalized through mandatory terms and conditions appended to existing and new permits for fossil fuel infrastructure. In essence, the two approaches help ensure that infrastructure owners, and not public agencies, bear the brunt of costs associated with catastrophic accidents, abandoned infrastructure, and climate disasters. They are:

- Suites of financial assurance mechanisms (such as surety or performance bonds, trust accounts, letters of credit, or catastrophic insurance) that make fossil fuel infrastructure owners fully responsible for the financial and economic costs associated with explosions, spills, toxic air emissions, abandoned infrastructure, and other discrete risks associated with fossil fuel infrastructure.

- Fossil fuel risk trust funds capitalized by surcharges on all fossil fuel product transactions in a local economy and used to compensate public agencies, businesses, and individuals for more generalized risks of fossil fuel infrastructure in their regions such as earthquake swarms or groundwater pollution as well as the costs of climate disasters, climate adaptation, and mitigation.

These mechanisms will help make energy markets more efficient by shifting a significant share of the costs of climate change away from taxpayers and on to the entities responsible. Pricing fossil fuels at an efficient level will also help level the playing field with solar, wind, and other renewables that are not subsidized as extensively. Forcing fossil fuel infrastructure owners to internalize such costs will also help slow new investments in assets like refineries, pipelines, and export terminals that are likely to be stranded as the world accelerates the transition to a renewable energy platform.

Fossil fuel risk bond programs are rooted in existing policy mechanisms

FFRB mechanisms are not new ideas. Some degree of financial assurance is required for onshore and offshore oil and gas wells and hazardous waste. The Environmental Protection Agency (EPA) maintains a useful typology of these instruments and has detailed fact sheets available for several, including corporate financial test, insurance, letters of credit, surety bonds, and trust funds that summarize regulatory requirements, recommended best practices, frequently asked questions, and sources of additional information. FFRB programs represent a logical extension of these to all classes of fossil fuel infrastructure and for the total economic value (TEV) of damages associated with worst-case scenarios.

For example, an oil terminal with modeled worst-case public damages from a spill or explosion of $400 million would be required to submit evidence of financial assurance for this amount to regulators of that facility. If the owner selects a surety bond, they would negotiate a premium paid to the surety, while the surety would be required to compensate the public via the regulatory body should the owner default on their obligation to pay damages if a catastrophe occurs. As envisioned, FFRB programs would bar self-insurance or self-bonding as an acceptable financial assurance mechanism given the fact that these forms of financial assurance are often lost in corporate ownership shuffles or bankruptcies that plague the fossil fuel industry.

Surcharges to pay for infrastructure improvements are not new either—surcharges on water bills routinely pay for upgrades to wastewater infrastructure. FFRB programs would extend the concept to wholesale trade of fossil fuels to pay for adaptation and other climate costs incurred by public agencies. A number of states, counties, and municipalities have begun to identify financial needs for big ticket climate adaptation measures, and it is fairly straightforward to design a surcharge to capitalize a fossil fuel risk trust fund (FFRTF) to meet those needs at the time the investments are needed. Alternatively, if funds are needed sooner, FFRTFs can be capitalized by bonds at any time and paid back with the surcharge proceeds.

In this section, we use estimates of climate mitigation costs and damage costs in New Jersey and California to quantify reasonable surcharges and illustrate the logic FFRTF programs (Table 1). According to a study of potential regional resilience trust funds, Harvard researchers find that unmet climate adaptation needs to control coastal flooding, retrofit highways, and harden water infrastructure within the greater New York metropolitan region total roughly $11.3 billion. In California, unmet adaptation needs have not been specified directly, but the state maintains estimates of anticipated climate damages for several sectors. For purposes of the illustrative example in this section, we use these damage estimates as a proxy for the level of funding needed for climate adaption in California. Within similar categories we include for New Jersey, California’s Fourth Climate Change Assessment (CFCCA) estimates costs to be nearly $98 billion by 2050. Assuming these are inflation adjusted and needed no later than 2050, it is relatively straightforward to calculate the amount that needs to be deposited annually to ensure that those funds are available.

As with most other trust funds, FFRTF investments would primarily be invested in public debt securities with a relatively low rate of return. In our example, if the expectation is for a 3% annual return, then annual deposits in New Jersey would need to be in the order of $260 million. California would need deposits of roughly $2.2 billion per year. Dividing these figures by the quantity of fossil fuel trade in each state in CO2 equivalent terms results in a surcharge of $6.31/tCO2-e in California and $2.68/tCO2-e in New Jersey. Using standard emissions factors for various types of fossil fuels, this translates into surcharges per barrel of oil, thousand cubic feet of natural gas, and short ton of coal reported in Table 1. To prevent these surcharges from being passed on to consumers, legislation or ordinances adopted to levy such charges can be accompanied by language prohibiting such a pass on, although the legal authority to do so may be challenged. Either way, the magnitude of owner or consumer cost increases needed to finance major climate adaptation projects via an FFRTF surcharge is not likely to be significant. The surcharges reported in Table 1 are far below EPA’s most recent estimate of the social cost of carbon and most carbon tax or trading schemes (another way to pay for adaptation) now in existence.1 Therefore, such surcharges may be a more attractive option to owners of fossil fuel infrastructure than other market-based approaches to remedy the climate change externality.

Update on Pacific Northwest initiatives

While CSE is working at the national level and in six states with NGOs and elected officials to promote FFRB programs, the most promising developments come from the Pacific Northwest, where three separate processes have been kicked off by the organizing work of CSE and its partners. Here, advocates have been promoting a model of FFRB implementation that unfolds in three distinct phases:

- Phase I: enabling legislation. While authority for implementing FFRB programs may already exist in a given jurisdiction, it is helpful to solidify that authority through enabling legislation. As recommended by CSE and its partners, that legislation should include findings connecting the dots between fossil fuel infrastructure, public health and safety risks, and allocation of funds for an economic risk assessment to establish the legal basis for subsequent regulation.

- Phase II: risk assessment. Once commissioned, the risk assessment quantifies the anticipated public financial costs associated with worst-case accident and disaster scenarios for fossil fuel infrastructure as well as the anticipated costs of climate change, mitigation, and adaptation. A gap analysis looking at the adequacy of financial assurance and adaptation funding is also conducted during this phase as well as recommendations for policy interventions to close this gap.

- Phase III: program implementation. Through rulemaking or ordinance, a jurisdiction adopts new financial assurance requirements for fossil fuel facilities based on the gap analysis and a surcharge for fossil fuel transactions to offset anticipated public financial costs.

The general three-phased approach is common to many forms of regulation (i.e., an initial resolution calling attention to the problem, a study to document the magnitude of local risks, and a rulemaking phase for implementation of recommendations). While a more streamlined approach could be to simply go right to the rulemaking phase—in this case, imposition of financial assurance and FFRTF surcharges—skipping the quantification of actual financial and economic risks on the ground would undermine the credibility, and potential legal footing, of the final regulatory requirements.

Three case studies demonstrate how FFRB initiatives are moving forward in this region. They include Multnomah County, Oregon; King County, Washington; and the State of Washington with respect to oil spill liabilities.

Multnomah County, OR – Portland’s Critical Energy Infrastructure Hub

In 2019, the Multnomah County Commission adopted a Phase I resolution opposing new fossil fuel infrastructure and initiating work on a FFRB program to “require the fossil fuel industry to bear the full cost of damages potentially caused by transporting and storing fossil fuels.” The resolution included findings that made a clear link between the storage, refining, transport, trade, and combustion of fossil fuels and a wide range of local health, safety, environmental, and economic risks. It is important to establish these findings in order to ward off legal challenges based on federal or state preemption (i.e., Interstate Commerce Clause) and keep FFRB program initiatives firmly grounded in a local jurisdiction’s police powers.

The resolution initiated a Phase II analysis of economic risks associated with a worst-case scenario at the Critical Energy Infrastructure (CEI) Hub in Portland along the banks of the Willamette River as a first step towards internalizing those risks through various financial assurance mechanisms or requirements for risk mitigation. The CEI Hub contains 630 tanks of petroleum-based liquids distributed over 220 acres, and over 90% of Oregon’s liquid fuels pass through the hub.

In early 2021, the Phase II risk analysis was completed by the firms ECONorthwest, Salus Resilience, and Enduring Econometrics. The study found that in the event of magnitude 8 or 9 Cascadia Subduction Zone (CSZ) quake—long overdue for the Pacific Northwest—a massive release of about 95–194 million gallons of fuel would likely occur, some of which would catch fire and potentially result in a one or more catastrophic explosions. At the high end, such a spill would be larger than the Deepwater Horizon disaster (~134 million gallons), making it the largest marine spill in U.S. history. In terms of economic damages, the study considered a broad range of both market and non-market effects and assigned monetary values to seven (Table 2). Depending on the size of the spill, failure rate for storage tanks, and utilized capacity at the time of the quake, damages could range from a low of $359 million to a high of $2.6 billion.

With this tally of potential damage in hand, decision makers are now considering options for Phase III in order to shift these financial and economic risks back onto infrastructure owners. One scenario involves assessment of seismic related risks by individual companies (there are about 10 in the CEI), mitigation planning to harden this infrastructure, and (potentially) bonding against mitigation plans. Bonding for decommissioning is also on the table since in the event of a catastrophic quake, abandonment without post-catastrophe clean up and repair is a distinct possibility. In the spring of 2022, the Oregon Legislature passed SB 1567A to jumpstart this process. The state’s Department of Environmental Quality has adopted a rule, and the initial round of facility assessments are expected to be completed by June 1, 2024 as the legislature intended. After this, discussions over bonding against mitigation plans and decommissioning will begin in earnest.

An alternative, more direct pathway to Phase III regulations would require the Multnomah County Commission to enact financial assurance requirements and FFRTF surcharges on a track separate from the seismic risk assessments since SB 1567A does not explicitly call for either. As shown in Table 2, the basis for per gallon surcharges to offset potential public liabilities associated with a worst case CSZ quake exist now, and so there are no real barriers to moving ahead with some form of a levy based on the ECONorthwest et al. analysis. CSE and its partners will be pursuing this approach, continuing to monitor implementation of SB 1567A.

King County, WA – Final phase III regulations now in place

In July of 2020, the King County Council enacted a Phase I ordinance in the form of amendments to its 2019 Comprehensive Plan establishing a new permitting system for fossil fuel facilities and a fossil fuel risk bond evaluation to lay the groundwork for new financial assurance requirements. As with Multnomah County, King County found that “the operation of fossil fuel facilities carries risk of explosion, leaks, spills, and pollution of air and water,” which, in turn, subject nearby communities to a litany of health and safety risks. King County is an interesting case study for FFRB programs because there are no active permits or applications for fossil fuel facilities at this time in the unincorporated portions of the Seattle metropolitan area where the Council has jurisdiction. So enacting a FFRB program here is largely a deterrent strategy against new or expanded facilities.

King County’s Phase II risk assessment was completed in June of 2022. The risk assessment concluded that three types of fossil fuel facilities could present public financial risks to the county in the form of costs related to health, safety, and infrastructure abandonment. These include thermal (gas) electric power plants, liquefied natural gas (LNG) plants, and oil terminals. The assessment found sufficient evidence of past high-cost incidents to propose requiring proof of adequate financial coverage for explosions from any of the three types of facilities. It also recommended that self-bonding not be accepted as a financial assurance mechanism to cover financial risks associated with potential explosions or site contamination and that advance planning around potential onsite hazards and facility decommissioning be required along with financial assurances against these potential public liabilities. Both of these recommendations are well justified based on the financial assurance gaps and issues identified in CSE’s 2016 report.

A draft ordinance was subsequently prepared to enact these recommendations, and in May of 2023 the King County Council adopted a final Phase III ordinance putting these FFRB program recommendations in place. With this, King County has become the first U.S. county to enact a full policy “trifecta” on the FFRB program concept. The Phase I, II, and III materials provide an excellent template to guide development of FFRB programs in jurisdictions across the U.S. with or without significant concentrations of fossil fuel infrastructure.

State of Washington – New financial assurance rules for oil vessels and onshore facilities

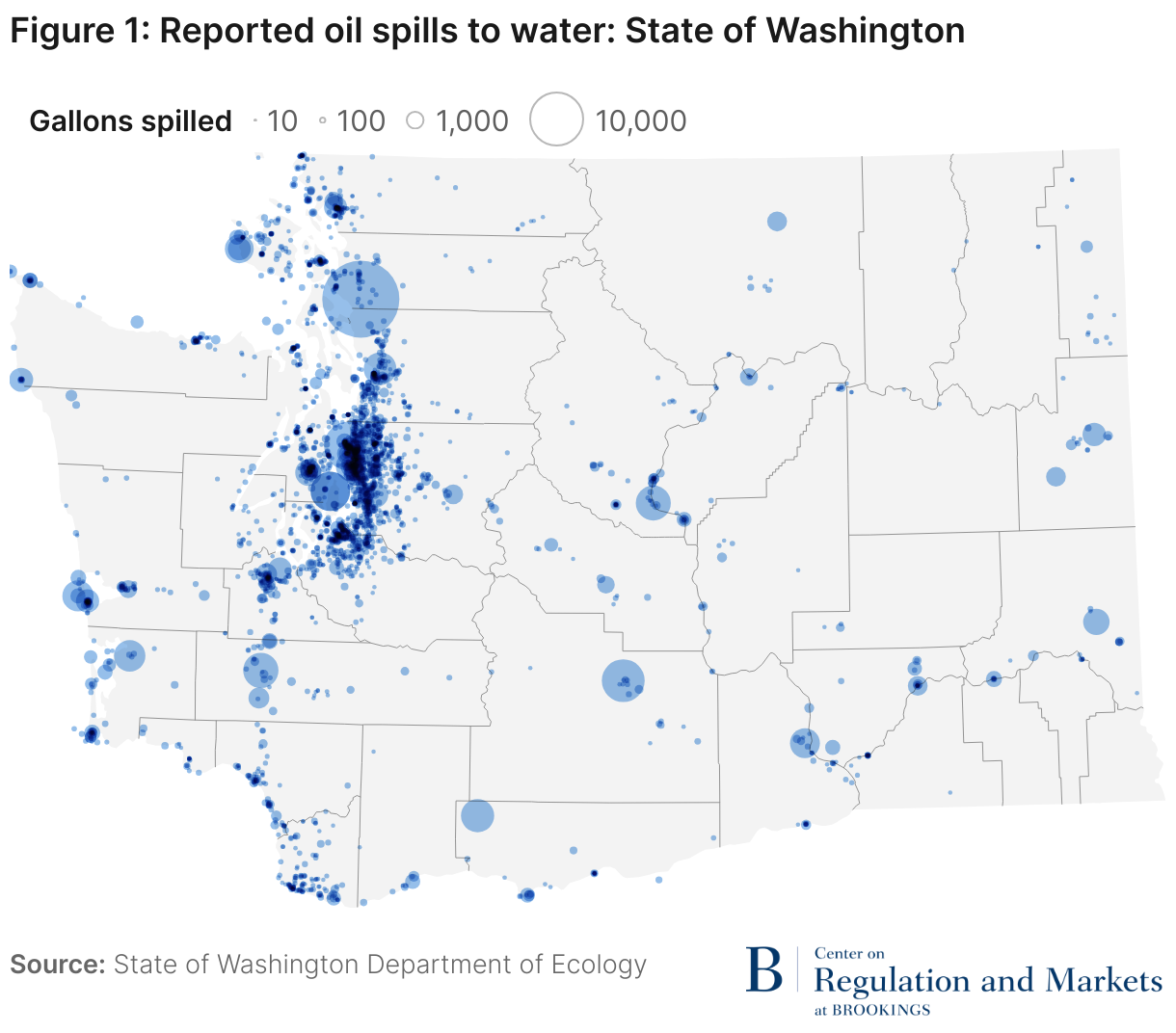

Led by Representative Mia Gregerson (D-33), the Washington legislature passed HB 1691 in the spring of 2022 as a first step towards implementing fossil fuel risk bond programs at the state level. HB 1691 requires the owners or operators of any covered oil vessel or oil facility to obtain a certificate of financial responsibility from the Department of Ecology (DOE) that guarantees such owners fully cover the costs of a worst-case spill. Acceptable forms of financial assurance include insurance, surety bonds, corporate guarantees, letters of credit, certificates of deposit, or protection and indemnity club membership. The legislation does not prohibit self-insurance, but instead imposes specific conditions for companies choosing that option. Oil spills of all sizes are frequent visitors to Washington’s waters (Figure 1), and HB 1691 was seen as a way to start shifting the significant cost burden of monitoring and responding to these spills to fossil fuel infrastructure owners. For the largest oil tankers, financial assurances of at least $1 billion are now required.

Initially, Rep. Gregerson drafted a more comprehensive statewide Phase I bill that would have expanded the Department of Ecology’s existing financial assurance requirements for hazardous facilities to include fossil fuel infrastructure. The first step in this statewide approach would have been a Phase II DOE report to the legislature evaluating the financial and economic costs and risks associated with fossil fuels and climate change, a gap analysis of existing financial assurance requirements, and recommendations to the legislature of how to close those gaps. DOE reviewed the legislative proposal and concluded that the analysis would cost about $1 million to complete 2—a price tag a bit too high to avoid political pushback. However this cost estimate assumed an original analysis of climate change costs would be needed when, in fact, the intent was for DOE to rely on the wealth of information already in existence. Regardless, investing $1 million to avoid potentially billions of dollars of economic costs is a great bargain for public finance, but in a political climate of fiscal austerity such a price tag for the Phase II study was enough to derail the more comprehensive approach. As an alternative, HB 1691 is viewed as an incremental, but important, step forward.

The law is a bit complex, and DOE is now charged with initiating a host of new rules to comply. These include (a) a rule governing the effective date for owners and operators of covered vessels or facilities to obtain the required certificates of financial responsibility; (b) a rule limiting use of a self-insurance option provided that such a rule must require the applicant to thoroughly demonstrate the security of the applicant’s financial position; (c) a rule governing the suspension, revocation, and re-issuance of certificates of financial responsibility; (d) a rule to evaluate whether an applicant for a financial responsibility certificate for an onshore or offshore facility has demonstrated an ability to compensate the state and other governmental entities for damages that might occur during a worst case oil spill; and, optionally (e) a rule to update the hazardous substances currently covered by the state’s existing financial responsibility requirements to maintain consistency with the Comprehensive Environmental Response, Compensation and Liability Act (CERCLA).

Conclusions

Lord Stern famously stated that climate change is the greatest and widest-ranging market failure ever seen. As the foregoing demonstrates, fossil fuel risk bond programs provide states, counties, and cities with an option for taking this market failure head on by shifting the public cost burden of both fossil fuel infrastructure and climate change back to where it belongs—on the polluters. By forcing fossil fuel infrastructure owners to internalize costs that are currently passed on to taxpayers, FFRB programs have the potential to disincentivize applications for new or expanded facilities and relieve fiscally stressed governments from the ever-growing costs associated with climate disasters, climate adaptation, and mitigation of greenhouse gases.

The Pacific Northwest case studies illuminate both the promise and complexities of enacting FFRB programs at the state and local levels. In this region, FFRB advocates have suggested a three phased approach to implementing the program, consisting of (1) an initial resolution or piece of enabling legislation to empower regulators to take action, (2) an assessment of fossil fuel infrastructure risks, and (3) a rulemaking process to impose financial assurance requirements and surcharges. In Multnomah County, Oregon, the key motivation for pursuing a FFRB program is the specter of a CEI Hub oil spill even larger than Deepwater Horizon and public financial costs that could top $2.6 billion. Given the urgency of avoiding such costs in the event of a magnitude 9.0 Cascadia Subduction Zone quake, decision-makers here opted for a Phase III process that accelerates adoption of seismic risk mitigation measures by individual companies rather than a program of financial assurances or a fossil fuel risk trust fund to offset a wider range of climate related costs. It remains to be seen whether the process adopted represents a delay tactic or a step towards full cost internalization, but either way the political pressure that came out of fossil fuel risk bond organizing efforts has borne fruit.

In King County, Washington, the key driver was deterrence—i.e., helping to make it cost-prohibitive to build new fossil fuel infrastructure. The Pacific Northwest has been in the crosshairs of the fossil fuel industry—50 large coal, oil or gas projects proposed since 2012—and having a FFRB program in place in the region provides an expensive regulatory hurdle that may prove too high to overcome. The absence of new applications for fossil fuel infrastructure permits allowed the full policy trifecta to be embraced and enacted without major opposition. At the state level in Washington, the cost of the Phase II risk assessment was deemed too high and forced legislators to revert to a less comprehensive approach focused on financial assurance requirements for oil vessels and onshore oil facilities. Despite the normal twists and turns of taking policy interventions from concept to on-the-ground reality, the Pacific Northwest experience with FFRB programs could provide a workable model for other states, counties, and cities across the U.S. where fossil fuel infrastructure is now concentrated or where new applications are on the rise.

Authors

-

Footnotes

- The World Bank estimates a current price corridor of 2023 USD 61—122 per t/CO2e. See: The World Bank. State and Trends of Carbon Pricing 2023. Washington DC: International Bank for Reconstruction and Development, The World Bank.

- Washington Department of Ecology. 2020. Department of Ecology’s Draft Bill Summary – Risk Bonding Bill, Representative Mia Gregerson. Olympia, WA: Washington DOE.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).