Two of the major issues in the economic management of the ongoing COVID-19 crisis are how to guarantee financing for emerging and developing countries, and how to manage their outstanding debts. The magnitude of the challenge is immense: Both the IMF Managing Director and UNCTAD have argued that the world needs $2.5 trillion of financing for these countries.

Financing should come from multiple sources. Official financing from multilateral development banks and the IMF is, of course, crucial, as it was during the 2008-09 financial crisis. Official development assistance also plays a fundamental role in poor countries. In relation to debt, there has already been some action on official debts of low-income countries and calls for broader debt standstills. But a crucial issue for emerging economies is private sector financing and debt restructuring.

As the COVID-19 crisis unfolded, the world experienced again a “sudden stop” where the flow of private financing to emerging countries was interrupted. During the early phase of the crisis, the IMF estimates that over $100 billion of private portfolio capital left emerging economies, a much larger outflow than after the collapse of Lehman Brothers in 2008.

But there has also been a recent revival of private financing that has been broadly ignored. The weekly analysis by JPMorgan of capital flows to emerging markets (including investment in local bond markets) indicates that there was a net outflow of $66.1 billion in March. But the net outflows have been smaller since then—$11.3 billion in April and $9.6 billion during the first three weeks of May—and have concentrated in equity flows. In fact, there have net inflows in May into hard-currency bonds.

Indeed, several emerging countries have been able to issue bonds in international markets in recent weeks on fairly good conditions. Focusing on Latin America, this includes Chile, Guatemala, Mexico, Paraguay, Peru, and Panama. Two regional banks have also done so (the Central American Bank for Economic Integration and the Development Bank of Latin America, CAF), as well as two state-owned firms from Chile (Codelco and the Santiago Metro) and two from Colombia (Ecopetrol and the Bogota Electric Energy Company, both with some private shareholders).

From mid-April to mid-May 2020, the total of these bond issues amounted to over $17 billion, much more than multilateral financing to Latin America during this period. Some of the issues achieved relatively good interest rates. The Mexican bond issue of April 22, for a total of $6 billion, was the largest in its history, was oversubscribed 4.75 times, and got an effective interest rate of 5 percent for its 2031 bond. The 2031 Chilean bond issue of May 5 got an even lower rate of around 2.5 percent.

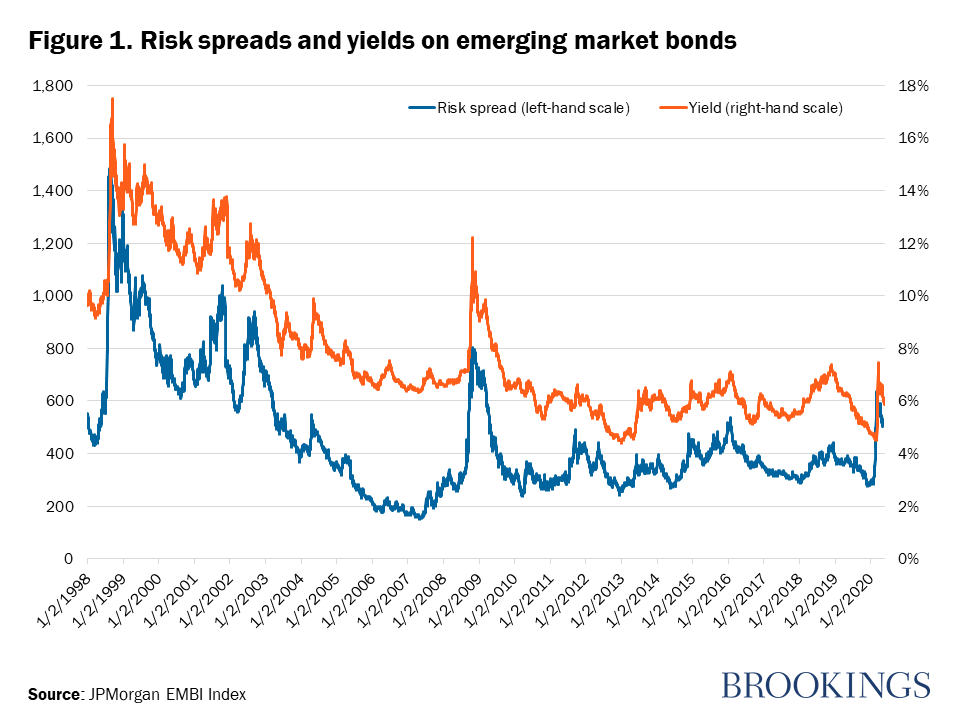

This is consistent with the trends in the risk margins and the yield of emerging market bonds. It is true that emerging markets’ bond spreads remain above pre-crisis levels, but the strong reduction in U.S. Treasury bond yields on which those spreads are added indicate that the yields for emerging markets’ bonds are moderate and falling. Measured by the best-known indicator of those yields, JPMorgan’s EMBI, the peak yield during the current crisis was 6.6 percent and has been falling to less than to 6 percent (Figure 1). As a reference, this is below the levels reached during the emerging markets’ turmoil of 2018 and much below the peak reached after the collapse of Lehman Brothers (when it peaked at 12 percent) and, particularly, after the Russian debt moratoria of August 1998 (when it peaked at 17 percent).

Together with trends in bond yields, this means that some form of “search for yield” seems to have returned. Furthermore, emerging markets have been able to issue bonds only two months after the financial collapse in February, a much shorter period than the 12 months that it took to do so after the collapse of Lehman Brothers in September 2008, and several years after the Russian 1998 debt moratoria.

This has major implications for the management of emerging countries’ debts. After the decision taken by the G-20 and the Paris Club to decree a debt standstill for the poorest countries through 2020, some analysts have argued in favor of a similar standstill for emerging economies.

However, debt conditions and market access are so markedly different among emerging economies that no unique way forward is desirable. In fact, there are three entirely different cases. Focusing again on Latin America, the first is that of countries that require major debt restructurings to guarantee sustainable debt levels (e.g., Argentina and Ecuador). The second case is countries that are already benefiting from accessing international capital markets. They can combine external private financing with borrowing from multilateral development banks and local bond financing.

A third group is countries in between these two extremes who need a voluntary debt standstill (supervised by the World Bank or regional development banks), such as that proposed by Patrick Bolton, Lee Buchheit, and others. According to this proposal, debt amortizations would be postponed and interest payments would be made into a central credit facility that would re-lend those funds to finance countries’ spending needs during the pandemics.

It should be added that the implementation of this proposal should go hand-in-hand with two other multilateral policies, which have been surprisingly absent from the international agenda during the current crisis.

The first is to negotiate a formal institutional mechanism to manage the restructuring of sovereign debts, beyond the market-based mechanism that was agreed in 2015.

The second is a major capitalization of multilateral development banks, similar to the one that took place in 2009-10 and that was essential for these banks to significantly increase lending to emerging and developing countries at the time. An agreement to capitalize the World Bank was reached in 2018 and has allowed it to launch a $160 billion 15-month program. However, regional development banks also need major capitalizations. This is particularly true of the Inter-American Development Bank and the Development Bank of Latin America, the two major multilateral banks serving Latin America.

The way forward should, therefore, be a mix of heterogeneous debt solutions and a major increase of financing from multilateral development banks and, in the case of countries with market access, a return to bond issues in international financial markets.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Financing and debt management for emerging market economies

May 26, 2020