On Thursday, January 11, the Africa Growth Initiative at Brookings launched its annual Foresight Africa report, highlighting key priorities for the region for 2018. Chapter five of the report, Harnessing Africa’s Digital Potential: New tools for a new age looks forward to the potential for digital technologies to propel Africa’s growth in the coming years.

According to Bloomberg, Kenya led all African countries in mobile money transactions—at $45.3 billion—through the year ending June 2017. In his Foresight Africa essay, former Governor of the Central Bank of Kenya Njuguna Ndung’u draws on Kenya’s successes in digital innovations beyond just financial inclusion.

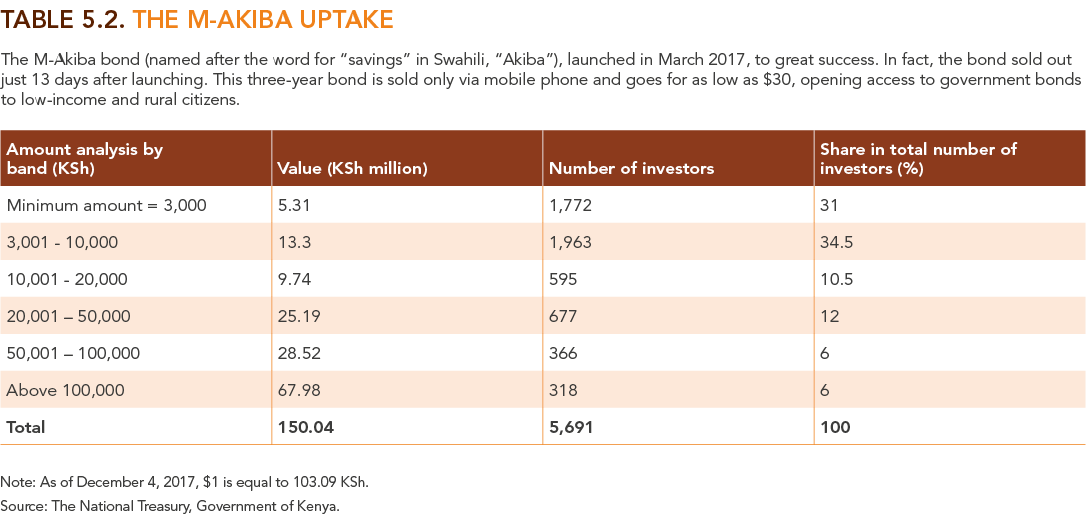

In 2017, Kenya became the first country to launch a mobile-only retail bond, M-Akiba, allowing micro-investments in government securities with investments as low as $30. Table 5.2 shows the success and stratification of the bond sales. As Ndung’u emphasizes, the bond had two major benefits: One, allowing micro-savers to invest efficiently and, two, allowing the government “access to a pool of savings that was out of reach before to finance its projects.”

The widespread digitization of the Kenyan economy has also improved revenue administration through implementation of digital tax systems, which has increased efficiency and reduced interaction between tax officers and taxpayers—creating fewer opportunities for corruption.

The Global Innovation Index has also ranked the country as an innovation achiever for the past seven years, longer than any other African country on the list. The index evaluates countries across several dimensions including infrastructure, human capital and research, market sophistication, institutions, and knowledge and technology outputs. As Figure 5.1 shows, much of East Africa as well as Senegal are leading the way on innovation in Africa.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figures of the week: Digitization and financial inclusion in Kenya

February 15, 2018