This week, the Africa Growth Initiative at Brookings published a new policy brief, “Taxing mobile phone transactions in Africa: Lessons from Kenya.” The brief discusses the limited ability of increased tax rates on mobile money transactions and mobile phone airtime to raise a significant amount of new tax revenue. According to the brief, these taxes disproportionately affect lower-income residents as those users are more sensitive to transaction costs. Lower-income users may also react to the cost increase by reverting to cash transactions, which could lead to lower financial inclusion, an area in which Kenya has made significant progress over the last decade.

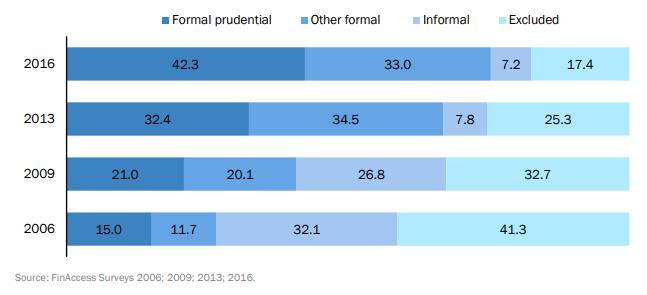

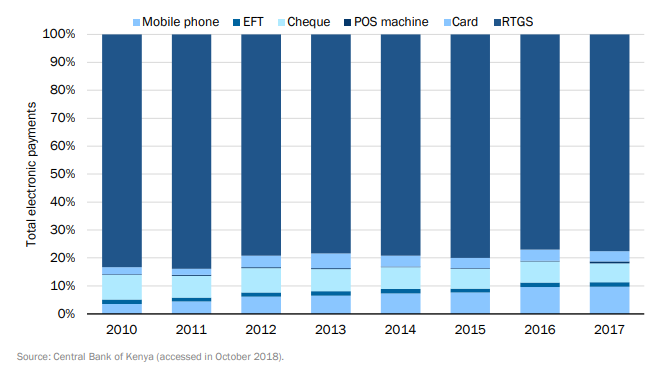

Formal financial inclusion in Kenya has almost tripled from 27.4 percent in 2006 to 75.3 percent in 2016, propelled by the launch of mobile financial services platforms (Figure 1). Mobile phone accounts increased from 1.4 million at the end of 2007 to 44.3 million in 2018. Though the proportion is still small, mobile phone transactions make up an increasingly large share of electronic transactions, rising from 3.6 percent in 2010 to 9.7 percent in 2017 (Figure 2). Notably, while the number of transactions has increased, the average value of mobile phone transactions has been declining steadily since 2011. The author, Njuguna Ndung’u, notes that this trend highlights that the platform is largely used by low-income earners to manage small transactions.

Figure 1: Kenya’s financial inclusion profile, 2006-2016

Figure 2: Composition of electronic payments in Kenya

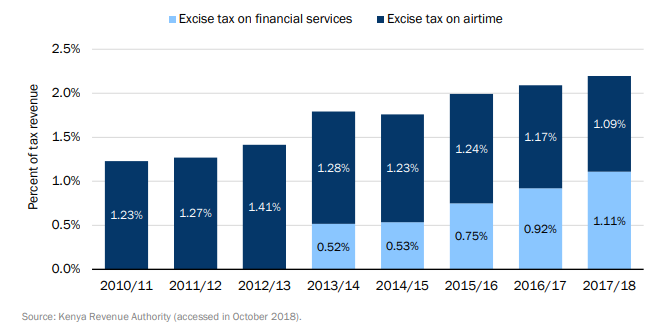

Taxes on mobile phone airtime and related financial services were first introduced in 2003 and 2013, respectively, and then increased in 2018. According to the brief, these taxes have only a limited contribution to overall tax collection: In 2017-2018, the two taxes combined for just over 2 percent of all government revenues (Figure 3). Additionally, the current tax structure actually leads to double taxation, as airtime is required for mobile money transactions. Ndung’u notes that the increasing tax rates and the challenge of double taxation raise concerns about a reversion to cash transactions and increasing financial exclusion for the poor.

Figure 3: Proportion of excise tax on airtime and financial services in total tax

For more on this issue, see the recent AGI policy brief, “Taxing mobile phone transactions in Africa: Lessons from Kenya.”

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figure of the week: Taxing mobile transactions in Kenya

August 7, 2019