Ethiopia is a net exporter of agriculture commodities. However, the low level of industrialized agriculture means that the country exports very little higher value processed food. Despite strong growth in manufacturing, agriculture remains the biggest export earner. Eighty percent of all export revenues of the country and 21 percent of total government revenues stem from the export of agri-products. However, only 1 percent of exported agri-products are in processed form. Agri-exports are dominated by unprocessed commodities while imports primarily comprise processed foods that are growing faster than exports.

The reason for this imbalance is related to urbanization. Over the last 25 years, populations in cities tripled from less than 8 million in 1995 to around 25 million today—leading to growing demand for processed food that domestic producers cannot supply yet. Urban consumers—a rising middle class—buy imported food products at relatively high prices. To satisfy this growing domestic demand and to diversify exports, one would expect a significant supply reaction with increasing investments in the food industry. However, this has not happened at scale yet. There are three main constraints that the government needs to address to enhance investment into the domestic food industry:

- Unleash the potential of the private sector.

- Promote access to finance and mobile money solutions.

- Promote market integration, commercialization, and scale.

The urgency of reforms shows the rapidly decreasing agri-food trade surplus. Without higher growth in the domestic food industry, the trade surplus will soon fade away even with further growing exports of raw products.

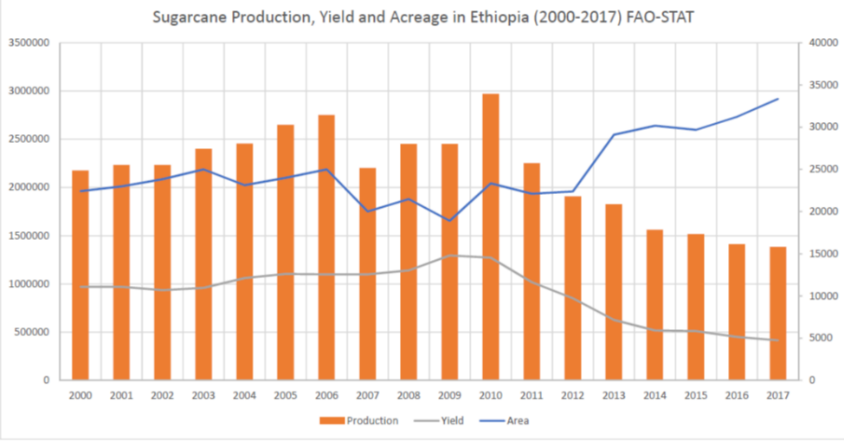

First, Ethiopia needs to unleash the potential of the private sector. The sugar sector is a striking example: While there have been large public investments in sugar processing and cane supply over the last 15 years, sugar production has stagnated and sugar cane yields have declined. The government rightly considers privatization of sugar factories a priority to improve sugar sector performance and prepared a new sugar law to attract international investors.

Figure 2. Performance of the state-dominated sugar sector

Source: FAO-STAT

A dominant presence of state-owned enterprises and state-owned banks led to huge productivity losses and creates distortions for private finance and investments. The financial sector is dominated by two state-owned banks with about half of total banking sector assets. State-owned enterprises have increasingly crowded out the private sector with the share of state-owned credit in total outstanding domestic credit surging from 14 percent in 2007 to almost 60 percent in 2018.

Second, Ethiopia needs to improve access to finance for farmers and agribusinesses. This includes mobile money solutions and the improvement of the digital infrastructure through telecoms privatization. Access to finance constraints is particularly evident in the agriculture sector that is the backbone of the Ethiopian economy. It is estimated that less than 20 percent of smallholder farmers in Ethiopia have access to financial services and according to the National Bank of Ethiopia only 4.9 percent of the total outstanding credit went to the agriculture sector in 2018. At the same time, the International Finance Corporation estimated that financing seasonal working capital for cereals only (barley, maize, teff, wheat) approximately $3 billion is required annually.

Commercial banks are mainly focusing on urban clients with limited knowledge and experience of rural clients. Capacity building for financial institutions trying to offer solutions in primary agriculture and agribusiness would be a precondition for more lending (training of credit officers in assessing sector risks, agri-benchmarking, and IT solutions). To reduce transaction costs, mobile money solutions and enhanced digital infrastructure will be crucial to reach smallholders in remote areas.

Developing the business enabling environment around post-harvest and inventory financing models as private sector processing increases creates interesting opportunities for commercial banks. However, as the finance gap in agriculture and the food industry is large it will be challenging for domestic banks to offer sufficient credit. Selective attraction of foreign banks for agribusiness finance may help to close the finance gap. Opening of the leasing sector is a good example.

Third, Ethiopia needs to promote market integration, commercialization and scale. Current production is primarily for subsistence and small scale with limited incentives for commercialization. A major reason is the tedious and informal land acquisition procedure. Investment promotion in rural areas starts with better and transparent procedures for access to farmland. Investors in the food industry wish to manage at least parts of their raw material supplies internally before they engage in outgrower schemes with smallholder farmers.

To increase the level of productivity in crop and livestock production, private input dealer networks need to be encouraged to enhance competition. This will improve the availability and quality of fertilizer, seeds, plant protection products, and animal feed. The government can support investments with better access to land, land leasing procedures, and industry standards.

For sophisticated value chains in horticulture, attraction of foreign investors to improve scale and competition is crucial. The success of the flower industry is a good example. Also, the opening of food retailing to improve the range of available food products and reduce food inflation will make a difference.

Currently, weak supply chains, particularly for non-export commodities like teff, wheat, and maize need improvement, for example, support of farmers’ groups to improve storage, quality, marketing, and linkage with the food industry. Investment promotion may focus on cold supply chains for the commercialization of perishable horticulture and meat and dairy products complemented by investments in fast growing cereals and oil seeds processing industries.

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Can agriculture be Ethiopia’s growth engine?

February 24, 2021