The sleeper news in President Biden’s announcement to forgive roughly half a trillion dollars in student loans is his proposed changes to Income-Driven Repayment (IDR) plans that are to take effect in January 2023. The changes mean that most undergraduate borrowers will expect to only repay a fraction of the amount they borrow, turning student loans partially into grants. It’s a plan to reduce the cost of college, not by reducing tuition paid, but by offering students loans and then allowing them not to pay them back. In the absence of action from Congress, Biden has no other obvious policy levers to reduce college costs. But using government loans to subsidize college has important disadvantages and will lead to unintended and unfortunate consequences for borrowing, student outcomes, higher education costs, equity, and the federal budget.

The proposed plan is substantially more generous than existing IDR plans. Undergraduate borrowers will pay 5% of any income (down from the current 10%) they earn in excess of about $33,000 per year (225% of the poverty line, up from 150%). If payments are insufficient to cover monthly interest, the government will forgive the remaining interest so balances do not increase. Any remaining loans will be forgiven after 20 years (or 10 years under the Public Service Loan Forgiveness program and for borrowers who borrow $12,000 or less). Borrowers with graduate debt are expected to benefit from all of the above, as well as the more generous treatment on any undergraduate loans. The Department will automatically enroll or reenroll certain students in the plan if they’ve allowed their income data to be used.

These parameters mean that the vast majority of college students will be eligible to make reduced payments (roughly 85% of undergraduates age 25-34) were they to take student loans, and a majority of undergraduate borrowers (perhaps 70%) would expect to have at least some debt forgiven after 20 years. On average, borrowers (current and future) might only expect to repay approximately $0.50 for each dollar they borrow. Again, that’s an average; many borrowers can expect never to make a loan payment, while others should expect to repay the full loan amount.

(These numbers are uncertain because estimating such outcomes requires a detailed model to project future payments plus data on debt levels and earnings of borrowers, neither of which are currently available. It is clear, however, that subsidies will be widespread and substantial.)

This represents a radical change in student lending. In recent years, the Congressional Budget Office has expected the average student loan borrower to repay more than $1 for each $1 they borrowed (because the government charges interest on the loans). Historically, this made loans a less attractive way to pay for college. But under the new plan, loans will be the preferred option for most students, and by a wide margin. Get 50% off the cost of college! But only if you pay with a federal loan, because you don’t have to pay it all back.

The administration’s plan will subject to public comment before it is implemented. There are several dimensions in which it is likely to have significant, unanticipated, negative effects.

- Increased borrowing. In 2016, undergraduate students borrowed $48 billion in federal student loans. But students were eligible to borrow an additional $105 billion that year and chose not to. Graduate students borrowed about $34 billion, but left $79 billion in unused eligibility on the table. Perhaps they didn’t borrow because their parents paid out of pocket or because they chose to save money by living at home—they still were eligible for federal loans. When those students are offered a substantial discount by paying with a federal loan, they will borrow billions more each year. (For more details, see below.)

- It subsidizes low-quality, low-value, low-earning programs and guts existing accountability policies. Because the IDR subsidy is based primarily on post-college earnings, programs that leave students without a degree or that don’t lead to a good job will get a larger subsidy. Students at good schools and high-return programs will be asked to repay their loans nearly in full. Want a free ride to college? You can have one, but only if you study cosmetology, liberal arts, or drama, preferably at a for-profit school. Want to be a nurse, an engineer, or major in computer science or math? You’ll have to pay full price (especially at the best programs in each field). This is a problem because most student outcomes—both bad and good—are highly predictable based on the quality, value, completion rate, and post-graduation earnings of the program attended. IDR can work if designed well, but this IDR imposed on the current U.S. system of higher education means programs and institutions with the worst outcomes and highest debts will accrue the largest subsidies.

- At the same time, the IDR proposal exempts failing programs from existing accountability policies like the Cohort Default Rate rules, which prohibit institutions from participating in federal grant and loan programs if too many of their students default on their loans. Under the proposal, certain students will be auto-enrolled in IDR, which can allow them to cease making payments without defaulting. It would be great to have a system in which default was not an option, but in today’s system, this eliminates the last remaining policy with any teeth that keeps predatory schools out of the loan program.

- High potential for abuse. A large share of student debt is not used to pay tuition, but is given to students in cash for rent, food, and other expenses. At public colleges and for-profits, living expenses represent more than half the estimated cost of attendance (which sets the upper limit on how much students can borrow). At many large for-profit schools (not known to leave money on the table), between 30% to 75% of student loans are returned to students in cash. (Indeed, I think this is a key reason anyone goes to these schools.)

- While students certainly need to pay rent and buy food while in school, under the administration proposal a student can borrow significant amounts for “living expenses,” deposit the check in a bank account, and not pay it all back. Gaming the system like this wasn’t possible when students were asked, on average, to repay loans in full, and it’s not a problem in systems where loans are used exclusively for tuition. But that’s not the system we have. Some people will use loans like an ATM, which will be costly for taxpayers and is certainly not the intended use of the loans.

- Who benefits is arbitrary, unequal, and unfair. As I’ve written in the past, a large share of student debt is owed by well-educated, white, financially successful students from upper-class families, which means that broad debt relief policies are regressive and preserve gaps between more and less advantaged groups instead of closing them. Compared to other federal spending programs intended to reduce poverty or benefit children, broad debt relief programs are more costly and benefit more advantaged Americans.

- Almost all undergraduate and graduate students will be eligible for reduced payments and eventual forgiveness under the proposal, which makes it effectively untargeted. Moreover, the amounts borrowers save (and eventually have forgiven) are based largely on the amounts students borrow, which means the benefits are uncapped and disproportionately flow to borrowers with the largest loans, who are more likely to be graduate students and students who attended more expensive programs. This makes it quite different, for example, from Biden’s recently announced debt relief plan, which focused relief on Pell Grant recipients, capped forgiveness at $20,000, and excluded high-income borrowers from participating.

- Likewise, while the IDR plan will reduce the amounts students ultimately pay for their education, it shouldn’t be confused with a policy to reduce or eliminate tuition and fees at public colleges like we do for public K-12 education. That’s because this IDR plan will cover a much larger range of costs: tuition and fees at for-profit and nonprofit schools, tuition and fees for graduate and professional school, and living expenses for college and graduate students. At many graduate programs, for example, a single graduate student living alone will be able to borrow more than $20,000 per year just for living expenses and never pay it back. For perspective, that is about double what a low-income single mother with two children can expect to get from the Earned Income Tax Credit (EITC) and food stamps combined. (The EITC maximum benefit is $6,164, and the average food stamp benefit for a family of three is $520 per month.)

- College tuition for low-income and most middle-income families is already largely covered by other federal, state and private aid; why is the government making it a priority spend more to cover the cost of expensive colleges, graduate programs, and living expenses for upper-middle-class families instead of on policies that serve the truly disadvantaged?

- Tuition inflation. A common objection to unrestricted tuition subsidies is that it will cause institutions to raise tuition. There’s good evidence for this at for-profit schools. High-price law schools have designed schemes to take advantage of generous debt forgiveness plans called Loan Repayment Assistance Programs (LRAPs), plans under which universities and students effectively shift the cost of tuition to taxpayers by exploiting debt forgiveness programs. It’s plausible that some institutions will change prices to take advantage of the program.

- At the graduate level, it’s clear that many students will never pay their loans at existing tuition levels, and thus will be indifferent if those programs raise tuition. Given the caps that apply to undergraduate loans (which limit the amounts undergraduates can borrow to between $5,500 and $12,500 per year), there is little room for schools to increase revenue by increasing the amount that existing borrowers borrow. Instead, my belief is that increases in undergraduate financial aid increase college costs primarily by increasing the number of (lower-quality) programs and the students who enroll in them. My fear, with regards to overall college costs, is that institutions will have an incentive to create valueless programs and aggressively recruit students into those programs with promises they will be free under an IDR plan.

- Budget cost. While there are huge uncertainties about how many borrowers will enroll in the program and the behavioral responses, it’s plausible that the new IDR proposal will cost as much (or more) as the existing Pell Grant program over the next decade while being much, much worse than the Pell Grant program—for all the incentives described above, plus it isn’t targeted, as Pell is, at lower-income households.

Unfortunately, all the negative effects of the IDR proposal arise because of its generosity—the fact that nearly all borrowers will be asked to repay only a fraction of borrowed amounts.

Indeed, given the existing design of federal lending programs, there is no coherent way to subsidize college with loans expected to be broadly forgiven as the IDR proposal contemplates. In a coherent system, Congress would change the law to:

- Provide more grant aid up front to low- and middle-income households to defray the cost of tuition so that students don’t need to borrow for those costs.

- Restore limits on the amounts that graduate students and parents can borrow to levels borrowers will be able to pay, limiting the taxpayer cost of those programs, reducing the incentive for schools to raise tuition costs above those limits, and ensuring that borrowers themselves don’t end up in financial distress.

- Impose strict accountability measures on schools to prevent the use of federal grants and loans at low-quality, high-cost, poor-outcome programs where students predictably struggle to find employment or where their outcomes don’t justify the costs of the program.

Only with the above elements in place can an IDR policy work as intended: as a revenue-neutral insurance policy, expecting the average borrower to repay their loan (eventually, with interest), but providing unlucky borrowers relief during periods of lower earnings, and forgiveness to persistently disadvantaged individuals. A coherent system can’t be delivered by regulatory fiat. Congress needs to act.

The remainder of this post provides additional details on some of the items above.

How much will people borrow under the new rule?

According to data from the Department of Education (NPSAS 2016), undergraduate students borrowed about $48 billion in 2016. That year, however, borrowers were eligible (based on federal loan limits and unmet financial need) to obtain an additional $105 billion in federal Stafford loans. Only 40% of dependent undergraduates took a student loan in 2016; the 60% who did not could have borrowed $35 billion, but chose not to. Dependents with loans came close to maxing them out, but still could have borrowed $3 billion more. Likewise, independent borrowers (those who are not supported by their parents) could have borrowed an additional $11 billion. And independent students who did not take out loans (two thirds of independent students) could have taken up to $56 billion in loans. Graduate students borrowed $34 billion; they could have borrowed $79 billion more. In other words, in 2016 students only borrowed 31% of the amount they were eligible to borrow ($82 billion out of $266 billion).

Clearly, many students did not borrow either because they or their parents paid for college in other ways. Some borrowed for tuition but not for non-tuition expenses (living expenses). Some were eligible for loans despite not having financial need, because their costs were paid for by the GI Bill or other sources that are ignored for purposes of Title IV aid. But such students are eligible for loans and could take them if they wanted. (Even if the GI Bill pays for your all tuition and living expenses, you’re still allowed to borrow against the same expenses.)

In the past it made sense for students to minimize borrowing in most circumstances. As recently as 2017, CBO projected that student loan borrowers would, on average, repay close to $1.11 per dollar they borrowed (including interest). Borrowing was often perceived to be the least favorable way to pay for college.

But under the administration’s IDR proposal (and other regulatory changes), undergraduate borrowers who enroll in the plan might be expected to pay approximately $0.50 for each $1 borrowed—and some can reliably expect to pay zero. As a result, borrowing will be the best way to pay for college.

If there’s a chance you’ll not need to repay all of the loan—and it’s likely that a majority of undergraduate students will be in that boat—it will be a financial no-brainer to take out the maximum student loan. Even borrowers who expect to pay the loan will benefit from subsidized interest rates applied when paying less than the full amount. (For example, because IDR is based on the information in your last available tax return, any student who earned less than 225% of the poverty line while enrolled would not have to make payments for the first one or two years after graduation and would thus benefit from an automatic one- or two-year interest-free loan.)

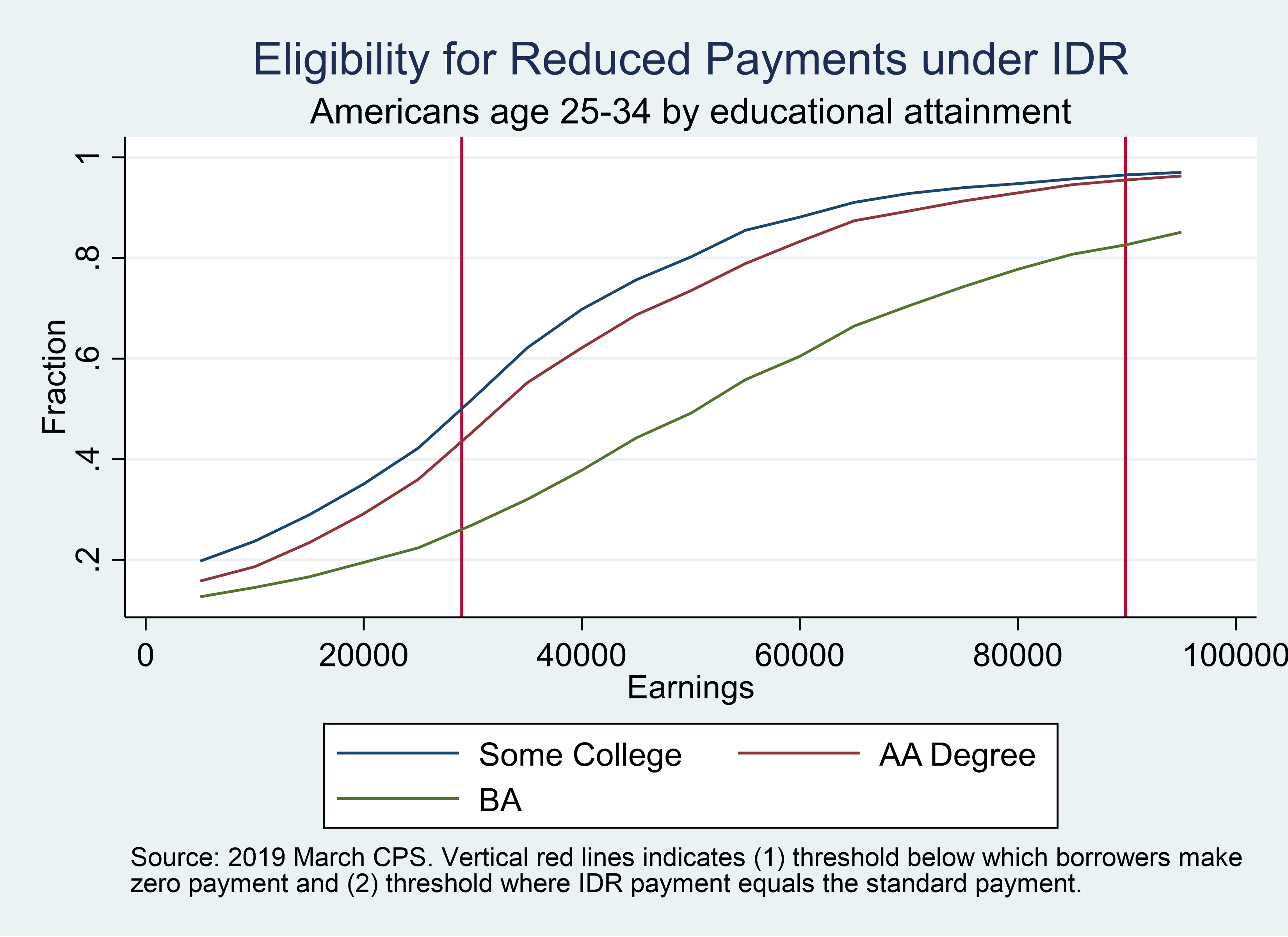

A large share of borrowers will benefit from the potential subsidy. The chart below illustrates the fraction of Americans age 25 to 34 with at least some college experience who may benefit from reduced payments under the IDR policy. The x-axis is income. The y-axis is the fraction of each group of students (those with some college experience but no degree, those with an AA degree, and those with a BA or more) whose earnings are below each income level. For instance, the chart shows that about 40% of recent BA graduates between the ages of 25 and 34 earn less than $40,000, but about 60% of AA degree holders earn less than that.

The first vertical red line indicates the IDR threshold below which borrowers will make zero payments. The second vertical red line indicates the threshold where the IDR payment just equals the standard 10-year payment (assuming the average undergraduate student debt for a BA graduate). In other words, the second vertical line indicates the point at which the borrower no longer benefits from a reduced payment under the IDR proposal.

The data shows that roughly half of Americans with some college experience but not a BA would qualify for zero payments under the proposal, as would about 25% of BA graduates. However, the vast majority of students (including more than 80% of BA recipients) would qualify for reduced payments.[1]

These reduced payments will result in substantial amounts of forgiveness. While the amounts are not clear given the specific parameters of this proposal, in earlier work, Urban Institute economist Sandy Baum estimated potential forgiveness under alternative IDR parameters, which are more generous than existing IDR policies, but nowhere close to being as generous as the IDR plans proposed now. For instance, in a scenario in which undergraduate borrowers paid 5% of income over 150% of poverty, and without the interest subsidy, only half of borrowers would repay a $30,000 loan (which is close to the average undergraduate loan balance). Under the new proposal, the fraction repaying the loan will be dramatically reduced because the threshold is higher and interest payments are subsidized. I suspect that roughly 70% of borrowers could expect eventual loan forgiveness under the new rule. On a net-present value basis (which is the appropriate method to evaluate the value of a loan subsidy), it seems likely that, on average, borrowers might expect to repay only $0.50 on each $1 borrowed. (Hopefully the Department of Education will provide an estimate of this subsidy in their assessment of the economic impact of the proposed rule.)

How much people will change behavior to benefit from this subsidy is, of course, unclear, because we’ve never run this experiment before. CBO expects undergraduates to borrow $382 billion in new loans over the next decade (prior to the proposed change in IDR). But if only a third of loan eligibility is used today, even small increases in the share that elects to borrow imply billions of dollars in additional loans.

Who might these new borrowers be? Surprisingly, the characteristics of people who don’t borrow look a lot like the characteristics of people who do borrow. That’s because the characteristics of people who use student loans mostly reflect who goes to college.

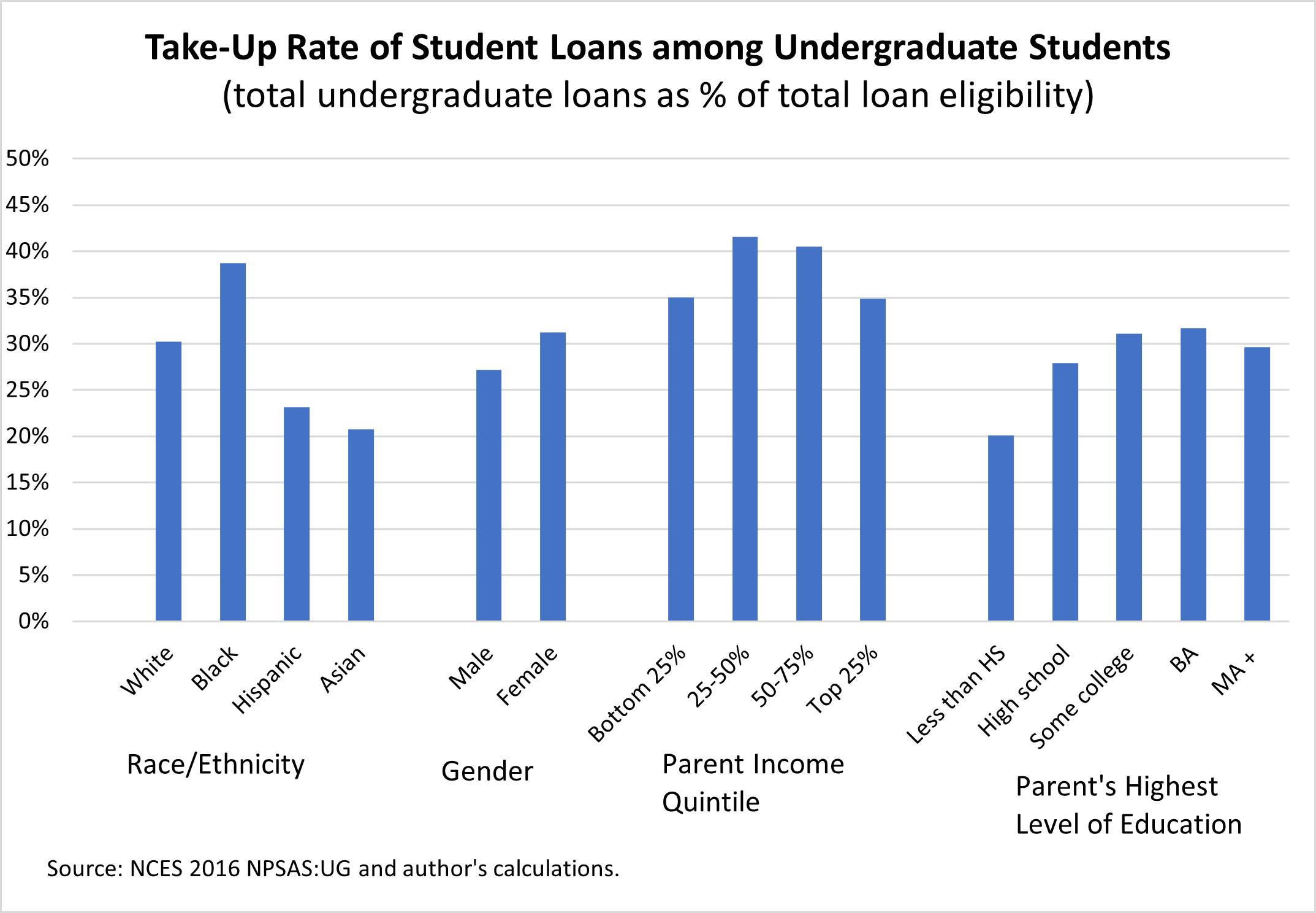

The figure below estimates the take-up rate on student loans. The chart compares the dollar amount of student loans borrowed in 2016 to the dollar amount of loans for which each group is eligible (based on year of study, average cost of attendance, independent or dependent status, and independent and dependent borrowing limits). These amounts are conditional on attendance, and so they ignore the fact that certain groups are under- or over-represented in college.

Take-up rates are, to my eye, low and uniform. Across parent income groups, low- and high-income families borrow slightly less of their capacity than the “middle class.” Children of less educated parents use less of their borrowing authority. Women borrow more than men. Black students borrow more than their white peers, who in turn borrow more than Hispanic and Asian students.

As much as people borrow today, they could borrow a lot more.

Why is this arbitrary, unequal, and unfair?

Untargeted student debt relief is not progressive, is more expensive, and benefits more advantaged Americans than do most other important spending programs. Those criticisms are highly relevant to the IDR proposal in question.

One reason is that the IDR policy is not well targeted. It is not based on financial need at the time of enrollment (as Pell Grants are). The total amount of forgiveness is not capped, as undergraduate loans are. And, unlike the administration’s recent retrospective debt forgiveness initiative, forgiveness under IDR is not capped. Indeed, when you consider which debts are projected to be forgiven under IDR plans, a better moniker is “debt-driven repayment” because most of the cost is associated with graduate borrowers and undergraduates with high balances. Such borrowers are better educated, more likely to have grown up in upper income households, not to be members of historically disadvantaged groups, and to earn more as a result of their graduate and professional degrees.

While the policy is based on income, that does not mean the proposed changes are progressive. One reason is that the parameters are set so that the vast majority of borrowers will benefit, even at high levels of income. But another important reason is that we already have a highly progressive IDR plan in place. Borrowers with incomes under 150% of the poverty line are already exempt from monthly payments, and borrowers over that threshold pay 10%. Hence, increases in the threshold from 150% to 225% only help borrowers whose income is over 150% of the poverty line, and then only by a maximum of 5% of their discretionary income (which by definition is greater for higher-income borrowers).

As a result, increases in the generosity of IDR parameters primarily benefit higher-income borrowers with higher levels of debt. Per CBO estimates, reducing the percentage of income borrowers pay (e.g. from 10% to 5%) and increasing the threshold that defines discretionary income (e.g. from 150% to 225% of poverty) benefits graduate borrowers three times as much as it benefits undergraduate borrowers.

Beyond the narrow examination of who benefits from IDR, it is also useful to consider how the proposed IDR plan compares to other federal spending policies. On many dimensions, the IDR proposal is more generous to its college-educated beneficiaries than are programs that are not specifically related to college students, even when they are intended to help substantially more disadvantaged groups.

A graduate student at Columbia University can borrow $30,827 each year for living expenses, personal expenses, and other costs above and beyond how much they borrow for tuition. A significant number of those graduates can expect those borrowed amounts to be forgiven. That means that the federal government will pay twice as much to subsidize the rent of a Columbia graduate student than it will for a low-income individual under the Section 8 housing voucher program (which pays up to $15,012 for a one-bedroom, provided the resident earns less than 200% of the poverty line and contributes 30% of their income in rent).

Likewise, under the IDR plan, a single, childless borrower earning $33,000 whose college or graduate education was paid for by federal loans will repay $0 for that benefit, but is subject to $5,049 in payroll taxes to fund Social Security and Medicare, $2,157 in federal income taxes, and, if they live in New York state, $1,220 in state income taxes. Individuals who benefit from certain programs (like Social Security) are thus asked to contribute much more of their own income than the beneficiaries of student loan programs. Is that fair?

I’m confident that federal support for higher education can achieve progressive goals, like providing opportunities for low- and middle-income households to attend college, using subsidies to reduce the cost of college, and reducing the financial burden of student loans. But support for higher education won’t be progressive unless it is designed to confront the intrinsic challenge that children from higher-income households are disproportionately overrepresented in postsecondary schools, particularly at good-quality 4-year programs and in graduate schools, and are disproportionately represented higher in the income distribution after they graduate. Unless programs are well-targeted based on student need, focus their spending on institutions and programs where students succeed, and pay only reasonable tuition costs, most of the benefits of federal subsidies will accrue to upper-middle-class families who would have gone to college and graduate school (and would have paid for it themselves).

Which academic programs are subsidized the most by IDR?

A disadvantage of using IDR to subsidize college attendance is that the subsidy is determined primarily by the post-college earnings of borrowers and is thus highly predictable based on the quality, value, completion rate, and typical labor market outcomes of students. That might be less of a problem in a system that tightly regulated the quality and cost of programs (as some foreign educational systems do), but in the U.S. there are enormous differences in the outcomes of students across institutions and programs.

The following table derived from the College Scorecard’s program-level debt and earnings data shows the typical payments of program graduates under the IDR plan versus the standard plan two years after graduation. The data are only for graduates, and dropouts are not included (but dropouts earn much less and thus are more subsidized). I calculate the subsidy crudely as the fraction of the original balance that would be forgiven after 20 years of IDR payments assuming the average earnings and debt of students two years after graduation.

The table shows the 12 degrees with the smallest average subsidy among programs with more than 5,000 annual graduates (the top panel) and the 12 with the largest subsidies (the bottom panel).

Despite the generous treatment under the IDR plan, engineers, nurses, computer science majors, economists, and mathematicians are expected to repay all or most of their original balance.

But the major beneficiaries are cosmetologists, borrowers with certificates in health, massage therapists, and music, drama, and art majors. In other words, the subsidies are highly determined by field of study (and within field of study, by quality and cost of the program). I suspect that an analysis of subsidies across institutions, which included non-completers, would show the largest subsidies would flow to institutions with high rates of non-completion, like many for-profit schools.

Using IDR to subsidize college ultimately means the programs and institutions with the worst outcomes and highest debts will accrue the largest subsidies. A neutral policy would give all students the same subsidy, such as with a larger Pell Grant. Or, better, direct greater subsidies to institutions and programs that help students get good-paying jobs.

How can borrowing for “living expenses” be abused?

While tuition and fees are an obvious cost of going to college and a key reason to take federal loans, students are also allowed to borrow for “living expenses,” and usually get that portion of their loan back in cash.

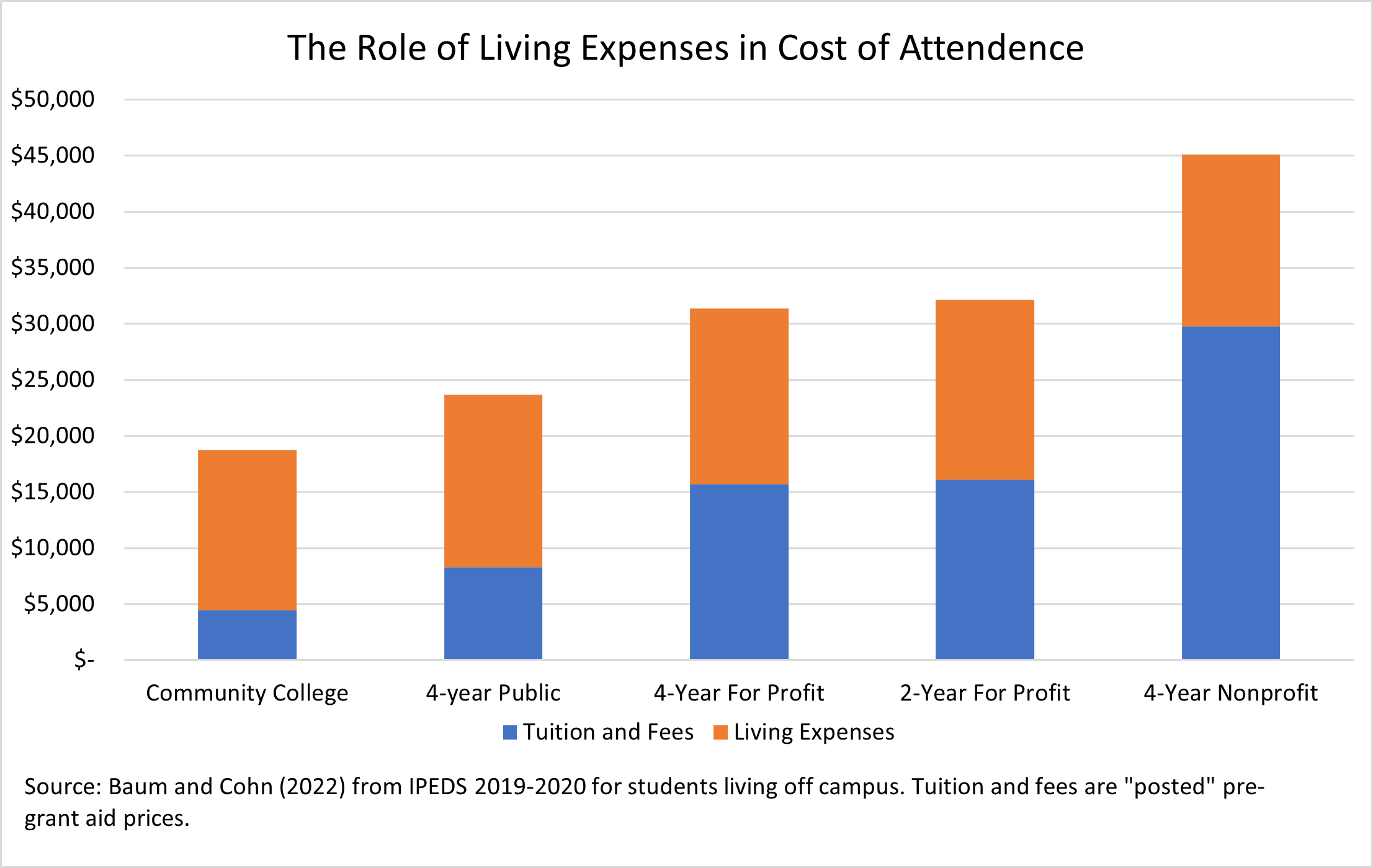

Colleges that participate in federal aid programs are required to estimate the cost of rent, food, travel, a computer, and other spending students are expected to incur while enrolled. As the chart below shows, these living expenses are a large share of the top line cost of attendance and are the largest contributor to the increase in the net cost of college over the last 16 years. In fact, at public colleges and 4-year private nonprofits, net tuition (published tuition minus grants) has been falling over the last 15 years; the entire increase in cost of attendance is due to living expenses. (And state public university systems never paid for room and board, so state disinvestment in education or inflation in university expenses isn’t the cause the of rising nontuition expenses.) At 4-year public colleges in America, living expenses are the largest share of cost of attendance, and they’re about half the cost of attendance at for-profit schools.

To the extent that financial aid (including loans) exceeds tuition (or tuition is paid by scholarship, by the GI Bill, or by a parent, or out of pocket) the student (or the parent, if they borrow PLUS loans) gets a check back for the remaining amount.

In short, a lot of student debt represents borrowing for living expenses, and thus a sizable share of the value of loans forgiven under the IDR proposal will be for such expenses. No doubt that students need room and board. But so do other Americans who aren’t in college, who are not eligible to take out a federal loan for living expenses, and generally don’t expect federal taxpayers to cover those expenses. Is it fair that federal programs help pay the rent of some Americans simply because they are college or graduate students, but not others?

The fact that a student can take a loan for living expenses (or even enroll in a program for purposes of taking out such a loan) makes the loan program easy to abuse. Some borrowers will use the loan system as an ATM, taking out student loans knowing they’ll qualify for forgiveness, and receiving the proceeds in cash, expecting not to repay the loan. Students will be able to do this when their federal loan limit exceeds tuition and fees owed, which can occur not only when tuition is low (e.g. at a for-profit or community college) but also when tuition is paid by parents, the GI Bill, a scholarship, or a Pell Grant. In such cases, undergraduate students can borrow between $5,500 and $12,500 per year, take the proceeds in cash, and, under the IDR proposal, expect to not have to repay it.

I suspect that such abuses will be facilitated by predatory institutions (if they aren’t doing it already). At for-profit schools, a large share of student loans are passed through to students in cash. According to reports submitted to the Department of Education for purposes of the 90/10 Rule (which caps the percentage of revenue that a proprietary school can receive from federal financial aid sources at 90%; the other 10% of revenue must come from alternative sources), between 30% and 75% of federal loan disbursements appear to be given directly to students, depending on the school. The pass-through of federal aid is clearly key to their business models. When Argosy University, a for-profit institution, suddenly collapsed a few years ago, some students complained they couldn’t finish their degree, but others lamented the fact that their financial aid disbursements would end leaving them “unable to pay rent or anything.” By promising to refund a portion of federal aid directly to students knowing the students won’t have to repay the loans, such institutions will serve as extremely high-cost ATMs, skimming 50% off the top of the loan before passing it along to the student.

Abuse of a loan program like this isn’t possible when the average borrower is required to repay the loan in full. It’s also not a problem when loans are used exclusively for tuition, because students have no incentive to over-borrow. But it will be a problem if people think they can take loans they won’t need to pay back.

What is the budget cost?

Even before any of the behavioral changes described above, the new IDR program will be costly. Borrowers already enrolled in IDR will presumably be switched over to the new plan, and future borrowers who would have enrolled in existing IDR plans will benefit as well. But focusing only on these groups would greatly understate the cost of the plan. As I said in a comment to the Department of Education during the regulatory process, their regulatory impact assessment should include a cost estimate for the new program that includes: (1) The cost of increasing the subsidy to existing IDR borrowers. (2) The cost associated with existing borrowers in non-IDR plans who switch into IDR. (There are probably not that many left after debt forgiveness, but there are some.) (3) The effect of future students taking out more loans and enrolling in IDR. (4) Changes in enrollment or increases in tuition costs. I suspect the Penn Wharton Budget Model high-end cost (up to $520 billion over ten years) exaggerates the cost of the plan, but it gives a sense of the enormous potential magnitude of the changes.

[1] While reduced payments are a good indicator that the borrower is benefiting from the plan, particularly because deferred payments are an interest-free loan under the proposal, the cumulative amount of the subsidy or the degree of forgiveness isn’t clear because that depends on cumulative payments each year for either 10 or 20 years, but those payments will never be more than the nominal (undiscounted) amount paid under the standard plan.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Op-edBiden’s Income-Driven Repayment plan would turn student loans into untargeted grants

September 15, 2022