The challenge

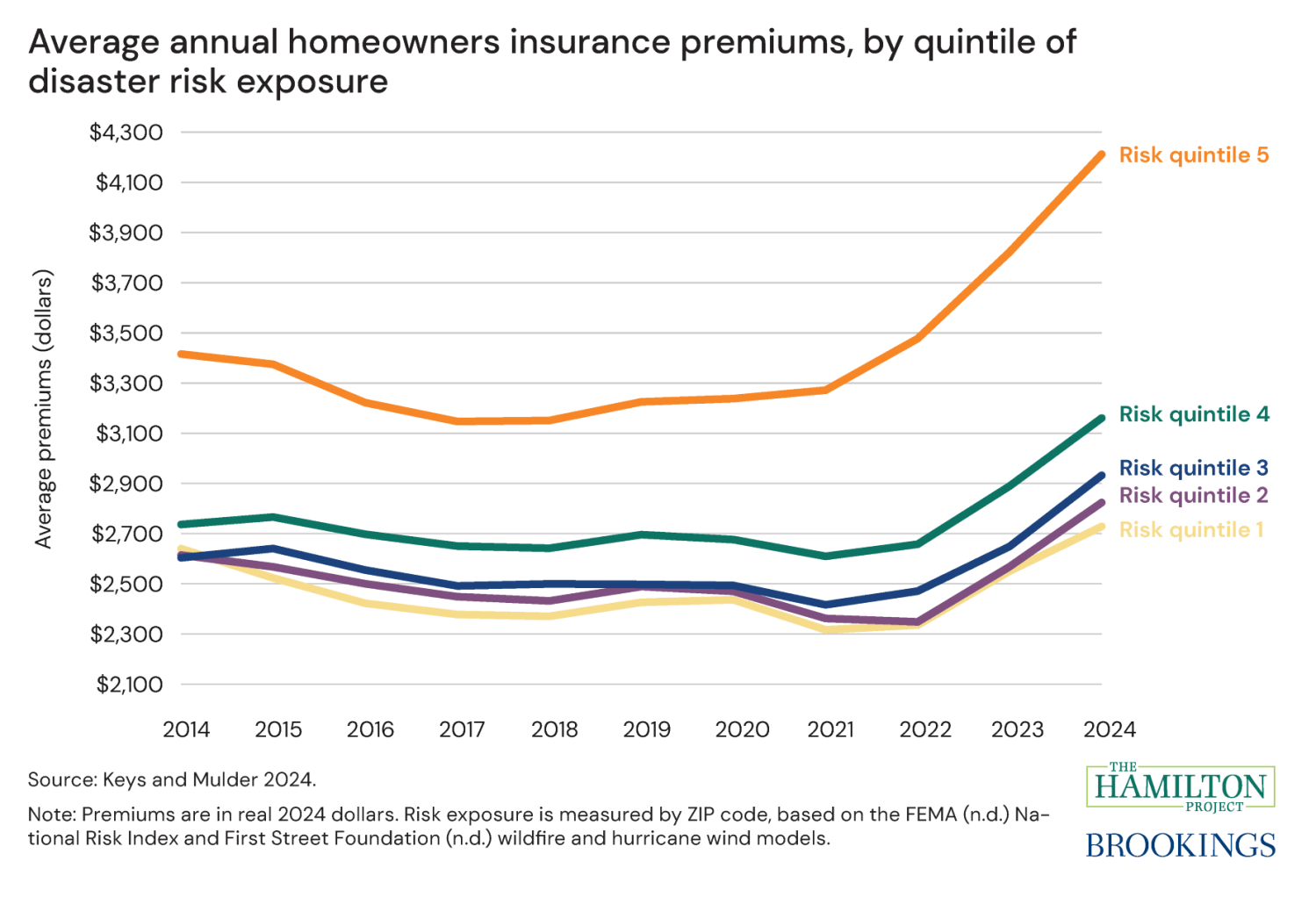

The U.S. homeowners insurance market faces mounting strain from severe climate risk. Inflation-adjusted premiums increased nationally by an average of 28 percent between 2017 and 2024, and even more in high risk areas. Insurers are also canceling policies, exiting markets, and in some cases going insolvent. These trends threaten household financial stability, housing markets, and disaster recovery.

Growing catastrophic risk related to extreme weather events is a central contributor to this problem. Catastrophes such as wildfires and hurricanes impose large, concentrated losses on insurers’ portfolios. Insurers manage this risk by purchasing reinsurance from global markets. However, the cost of reinsurance for U.S. catastrophes is high and volatile.

Looking forward, we can expect more of the same. Disaster risks will continue to worsen, perpetuating the challenges of insuring against catastrophic events and the associated problems: premium increases that exceed the increase in underlying risk, rising premium volatility, and lack of access to insurance coverage.

The proposal

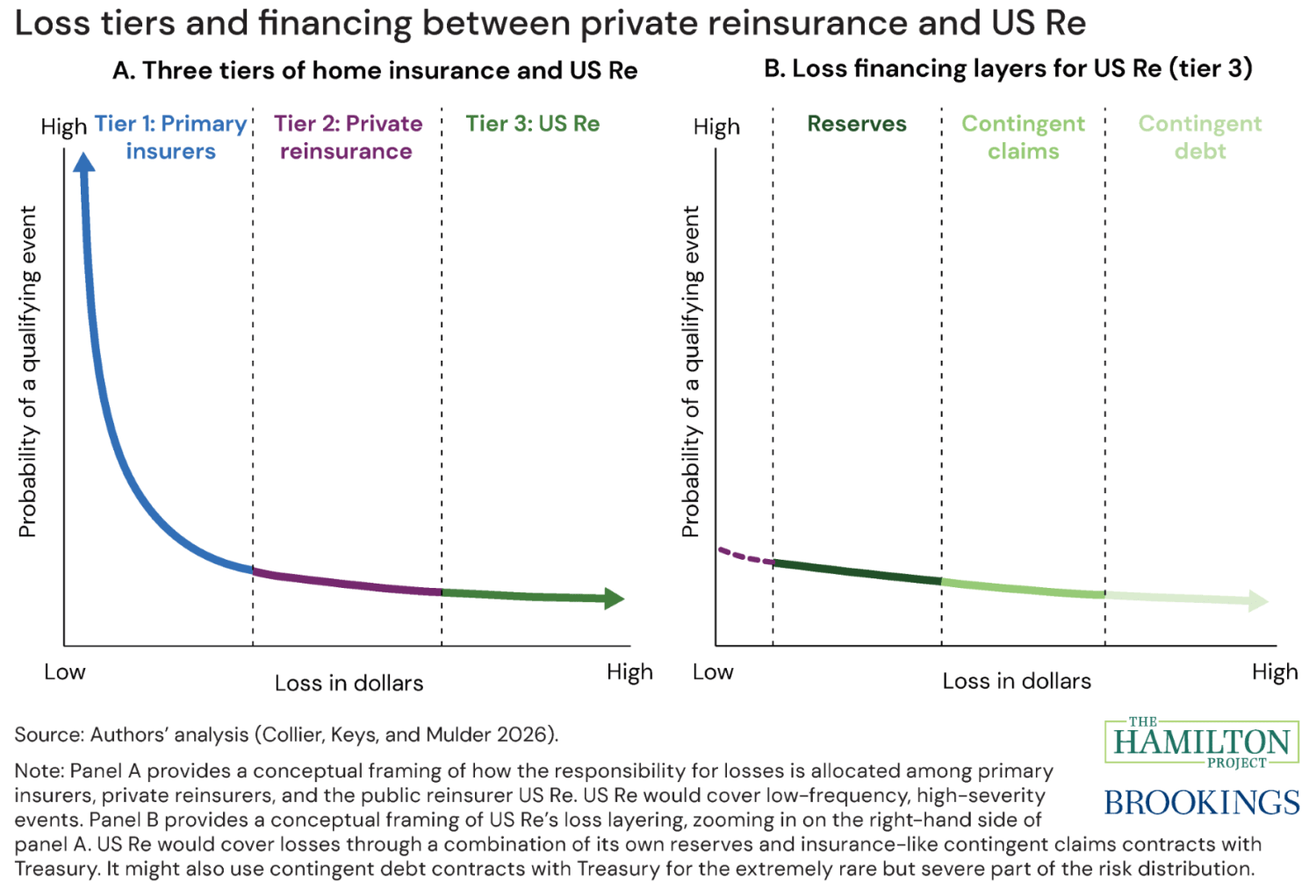

We propose a federal reinsurance entity, “US Re,” that would sell reinsurance contracts to providers of U.S. homeowners insurance and reinsurance to cover the most extreme weather events. Because the federal government can borrow substantially and at attractive rates, US Re could credibly and reliably pay claims without being subject to the same high and volatile costs as the private reinsurance market. As a result, US Re could help households maintain more consistent and affordable coverage, contribute to resilience and disaster recovery, and help stabilize mortgage and housing markets.

Drawing on the experiences of existing public insurance and reinsurance programs, we recommend that US Re should be designed to follow three main principles: 1) price risk, 2) target market failures, and 3) maintain credibility. Rather than subsidizing risk, US Re would set prices according to expected loss and other expenses while lowering costs through its more favorable cost of capital. US Re would maintain a substantial role for private insurers and reinsurers, which provide valuable sources of innovation and market discipline. Finally, US Re should have clear authority to pay claims and political independence in setting prices.

With sound governance and proper coordination across public and private sectors, a well-designed federal reinsurer could serve as a critical step toward restoring stability and resilience in the U.S. homeowners insurance market.

Authors

Related Content

2026

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

A proposal for a US federal property reinsurer

March 18, 2026

Key takeaways: