This post is a summary of a discussion at an event held on February 6, 2024. Watch the full video here.

National Credit Union Administration (NCUA) Chairman Todd Harper came to Brookings on February 6 to outline his agenda in the wake of changes to the NCUA Board that have given Democratic appointees a majority for the first time in the Biden administration. After his speech, Chair Harper and Brookings Senior Fellow Aaron Klein held a fireside chat and took questions from the audience. During that exchange Chair Harper emphasized new reporting requirements requiring some credit unions to publicly disclose their overdraft revenue for the first time. Overdraft was one of three key topics discussed, which are summarized below. The full event can be found here.

1. NCUA’s #1 priority: Protect the share insurance fund

Chairman Harper was crystal clear that his top priority is protecting the insurance fund that protects members’ deposits. Credit unions, like banks, insure customers’ accounts up to $250,000. Among credit unions, over 90% of deposits are fully insured, while that figure is around 60% for banks. This highlights how credit unions focus more on serving middle- and lower-income Americans and are less involved in serving the wealthy, businesses, or other large depositors, as in the banking system. Chair Harper noted that at Silicon Valley Bank (SVB), whose failure in March 2023 caused broader instability in the banking system, was due in part to the fact that more than 90% of SVB’s deposits were uninsured. This creates greater “run risk” at banks than credit unions and is one reason why credit unions can be more stable financial institutions.

2. NCUA’s top regulatory concerns

Protecting depositors and the Share Insurance Fund requires NCUA to monitor credit unions’ safety and soundness, and Chair Harper highlighted three regulatory problems that need immediate attention: credit union service organizations (CUSOs), liquidity, and concerns about loan defaults. He called NCUA’s lack of regulatory authority over CUSOs and third-party service providers, “an Achilles heel for the credit union system.” CUSOs are affiliated, non-bank entities that can blur or even cross the line between traditional banks and commercial activity. For example, PenFed credit union and Berkshire Hathaway jointly operate PenFed Realty, a real estate brokerage that Chair Harper noted a bank would be prohibited from operating. Klein commented that Berkshire Hathaway is a firm traditionally not focused on serving the needs of middle to low-income Americans, while Harper raised the broader point that, “the NCUA’s lack of visibility into these critical industry participants is a major problem that poses a systemic risk to the financial services system and our national security.” Similarly, he raised concerns regarding NCUA’s lack of visibility into third party service providers. Harper called on Congress to “close this regulatory blind spot”– pretty strong words from a regulator.

Harper expressed concern about safety and soundness, stating: “a large and growing share of the credit union system’s assets reside in institutions with potential safety-and-soundness concerns that require immediate remediation.” Harper noted the growth in large, complex credit unions with a CAMELS 3 score that encompass $131.7 billion in assets: a nearly 45% jump in just the last quarter. This sharp increase in credit union assets in CAMELS 3 rated institutions comes while there remains modest increase in assets at credit unions with CAMELS 4 and 5 ratings. Three is the midpoint on the 1-5 CAMELS scale that is not symmetric: 5 indicates almost immediate closure and 4 merits the institution being placed on the “troubled” list, which requires the regulator to set aside money from the insurance fund in case it fails. Falling to 3 is a significant regulatory downgrade for any individual credit union and the broader trend signals a growing presence of unsafe and unsound practices that require immediate action.

Harper’s concern about broader liquidity problems across credit unions (Liquidity is the L in CAMELS) is exacerbated by a statutory lapse of the NCUA’s Central Liquidity Facility. Operating as an emergency liquidity backstop, the NCUA’s liquidity facility is similar to the Federal Reserve’s discount window, providing a crucial safety net in times of stress. However, a statutory lapse has led to a decline in credit union membership in the facility by nearly 90%, with 3,322 small credit unions losing access. Harper reiterated NCUA’s call on Congress to “to allow corporate credit unions to purchase capital stock in the Central Liquidity Facility to help smaller credit unions access liquidity, and to provide other regulatory flexibilities to increase the facility’s accessibility.”

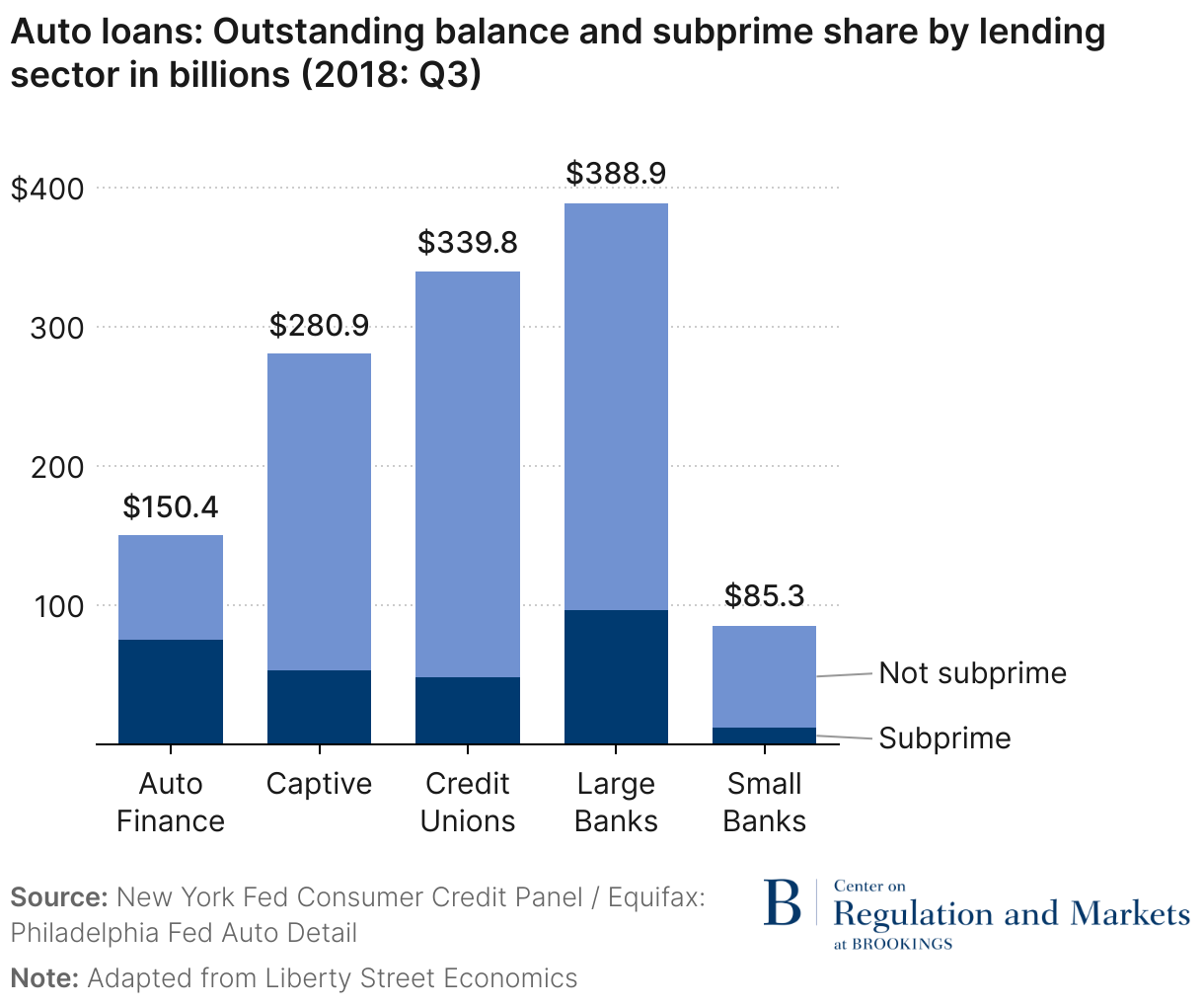

Harper noted a few specific areas of concern in lending credit quality among credit card and auto loans. Credit unions punch above their weight in auto lending; as this data from the New York Fed shows, they accounted for a disproportionate share of auto lending relative to their size and that of banks. As Harper put it: “today’s economic environment requires active—not passive—management by credit union boards and senior leadership.”

3. Consumer protection

Chairman Harper announced new disclosure requirements requiring credit unions with over $1 billion in assets to report overdraft and non-sufficient funds (NSF) fees collected. This will impact around 425 credit unions that combined cover over 90% of the assets of the entire credit union system. This new disclosure requirement is a massive step forward to allow the public, researchers, and credit unions members to understand the level and potential reliance of certain credit unions on overdraft fees. It is something Klein has advocated for, including in testimony before the Senate Banking, Housing, and Urban Affairs Committee in 2022.

Banks of similar size have been required to report overdraft data for years, and a new California law resulted in the first broad disclosure of overdraft profits from credit unions last year. Klein’s analysis of this new data showed 30 California credit unions earning more than 50% of their net profit on overdraft fees alone. Harper was concerned by this, noting that “Overdraft fees are falling disproportionately on people of color and on lower-income families overall.” Harper noted that the “the statutory mission of credit unions is to meet the credit and savings needs of their members, especially those of modest means” and wondered how a credit union that relied too heavily on overdraft fees could be compliant with that mission. What the new overdraft data reveal will shed light on overdraft practices at the nation’s largest credit unions, data that may help to drive reforms similar to what many of America’s largest banks have done with their overdraft practices.

Harper mentioned several other consumer concerns, including a discussion of the Consumer Reinvestment Act (CRA). Bank regulators have recently changed their implementation of CRA, which credit unions are exempt from under federal law. Harper noted that exemption is up to Congress to decide, however a growing number of states are instituting their own CRA-like requirements on credit unions. Harper noted that extending CRA to credit unions would require flexibility given the various ways credit union fields of membership are created. Klein pointed out the growing number of credit unions that functionally are open to anyone, including some that are buying stadium naming rights. Harper responded that if he “were on a credit union board, I would be advocating that rather than spending that money necessarily on naming rights, I’d be pointing in the direction of what can we do to lower the prices of our loans and increase the service to our members.”

One final point Harper made tied many of his themes together. Harper added new reporting information on minority deposit institutions (MDIs) which he found “eye opening.” Harper believes MDIs are hyper focused on serving their members in their communities and are generally very small. MDIs return on average asset—the metric Harper uses for credit union “profit”—was just as strong as the large billion dollar plus credit unions. MDIs achieved similar returns despite higher loan delinquencies. Elevated default levels are expected when lending to lower-income people. MDI’s were able to offset greater default rates by collecting more from people who had defaulted. Harper’s take away is that “a credit union that has a great focus, good leadership, is able to be just as competitive and, in this current environment, achieve the same earnings,” regardless of size.

Authors

-

Acknowledgements and disclosures

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

A conversation with NCUA Chair Harper: Highlights from the Brookings event

February 20, 2024