Lessons learned from

support to business

during COVID-19

The United States responded to the recession caused by the COVID-19 pandemic with massive and unprecedented support for businesses. New federal business subsidies over the period 2020Q2–2021Q1, including the Paycheck Protection Program (PPP), Economic Injury Disaster Loan (EIDL) advances, and targeted aid for sectors such as airlines and restaurants, totaled $600 billion, or about 2.7 percent of potential GDP, while expanded EIDL added an additional $200 billion of support. The Federal Reserve authorized purchases of up to $750 billion in corporate bonds through the newly created Corporate Credit Facilities (CCFs) and up to $600 billion in long-term, low interest rate loans to midsize corporations through the new Main Street Lending Program (MSLP).

It is important to try to isolate the role for and effectiveness of direct government support for businesses from the COVID-19 recession circumstances. Both the overall macroeconomy and business survival fared much better during the pandemic than initially feared or historical experience would have predicted. Videoconferencing technologies, testing protocols, and the quick development of vaccines meant that many businesses were able to partially or fully reopen sooner than anticipated. These factors, in addition to the policy response, created a quick economic rebound which allowed businesses to face short-term cash flow shortfalls rather than fundamental insolvency.

Recession Remedies podcast episode: How effective was aid to business during COVID-19?

Evidence on Support to Business

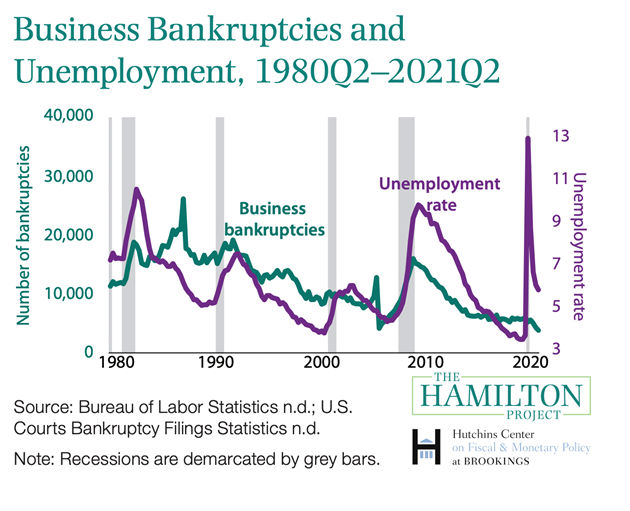

- The business sector overall fared much better during the COVID-19 recession and recovery than previous downturns. Business bankruptcy filings declined during a recession year for the first time since 1980 and remained below their pre-pandemic level into 2021. Sales recovered much faster during the pandemic than during the 2007–09 downturn.

- There is no credible evidence that the largest PPP loans had a substantial positive employment effect in the short or medium run. The evidence for the efficacy of loans to the smallest firms is more mixed.

- While both the Employee Retention Credit and grants to air carriers had features designed to link disbursements to payroll, the fungibility of funds raises the possibility that they may instead have benefited shareholders.

- The EIDL program made 3.6 million loans totaling $194 billion through November 2020 and an additional $124 billion over the following year. Relative to PPP, these loans have the benefit of providing immediate liquidity but at much lower cost to taxpayers. In addition, EIDL were potentially better targeted, as only businesses with an expectation of long-term viability could apply.

- Federal Reserve interventions into the corporate bond market clearly can play a stabilizing role. Although the CCFs used only approximately $15 billion of their $750 billion capacity, evidence suggests that they significantly lowered bond yields in the spring of 2020.

- The Fed’s direct support for bank lending had little direct impact since banks remained in relatively good health. Had banks been balance sheet constrained as they were during the 2007–09 recession, such a policy could have proven useful.

- Large firms initially reacted by raising substantial external financing from private markets. These firms raised debt by drawing down existing credit lines and increasing bond issuance and conserved equity largely by pausing share repurchase programs. This increase in financing allowed these firms to withstand the initial decline in net income.

Lessons learned from support to business during COVID-19

The variety of policy supports enacted during the COVID-19 recession as well as the unusual course of a lockdown-driven recession pose serious confounders to concluding a causal link between the business aid programs and the economic trajectory. The speed at which support programs were deployed during the COVID-19 pandemic was admirable. However, given the rapid rollout, it is not surprising that some of the programs were not well-designed to achieve maximum impact. Policymakers should not automatically interpret the rapid recovery from the pandemic as evidence that business aid programs have strong economic benefits; policymakers should not blindly re-deploy the 2020 tool kit.

Both the overall macroeconomy and business survival fared much better during the pandemic than initially feared or historical experience would have predicted.

Many careful studies found that the programs meant to support business and employment had relatively small effects, suggesting that other factors including the nature of recovery from a temporary lockdown and general support for households likely played a more important role. There may be circumstances in which small business lending programs like the EIDL or bond market stabilization programs like the CCFs could prove useful—for instance, in cases in which other support for households is less generous—but they should be judiciously deployed.

Support for small businesses, like the PPP, could have been restricted to significantly smaller firms. For instance, the employment cap for program eligibility could have been set at 50 or 100 employees, instead of 500, without adversely affecting the program’s overall impact. Support for large firms, such as publicly traded airlines, should be treated skeptically because these firms have access to many forms of financing and can be efficiently processed by the bankruptcy system. While the Federal Reserve clearly can support banks and corporate credit markets, whether it should do so involves careful consideration of the reason for the disruption in credit markets.

For more information or to speak with the authors, contact:

About the Authors