The potential—and pitfalls—of the digitalization of America’s food system

Food is a critical good in the American economy. Although the COVID-19 pandemic dramatically restructured food consumption patterns and triggered a 17% drop in food expenditures, the U.S. food service and food retailing industries still sold $1.69 trillion worth of food in 2020. It took 19.7 million workers—10.3% of all U.S. jobs—to grow, process, move, and sell this huge variety of food products. And consuming all those products remains a major part of household budgets: In 2020, food expenditures accounted for 8.6% of the average consumer’s disposable income, and 27% among low-income Americans.

The relationship between food, economic security, and public health is hard to overstate. When food prices change, consumers notice. When restaurant or farm-based employment plummets, the economy suffers. When incomes drop, food insecurity rates rise, affecting health and nutrition. Nutritional concerns are not only a problem in economic downturns, either; in 2019, before the pandemic, more than one-tenth of all U.S. households and 8.3% of households with an elderly individual faced food insecurity.

Like many other parts of the U.S. economy, e-commerce is now rapidly transforming the food system. The pandemic-fueled rise of digital platforms has brought online ordering and rapid last-mile delivery services to consumers around the country, changing how Americans shop for food in the digital age. Unlike any time in human history, food can now meet people where they are—not the other way around.

Scholars, activists, and practitioners have spent decades thinking through the health of our brick-and-mortar food systems. Now it’s time to imagine what a healthy digital food system should be, and ask critical questions about food access, affordability, and quality—as well as market structure, workforce, and labor—in the context of the digital age.

The digitalization of the food system offers a historic opportunity to address food insecurity. But it can only succeed if we reach all people where they are and nurture a system of resilient food providers. This brief explores how digital infrastructure is transforming the food system. We use new food delivery data to measure access to food delivery services across the country and analyze administrative data from the U.S. Department of Agriculture (USDA) to understand how online access to food assistance has expanded over time.

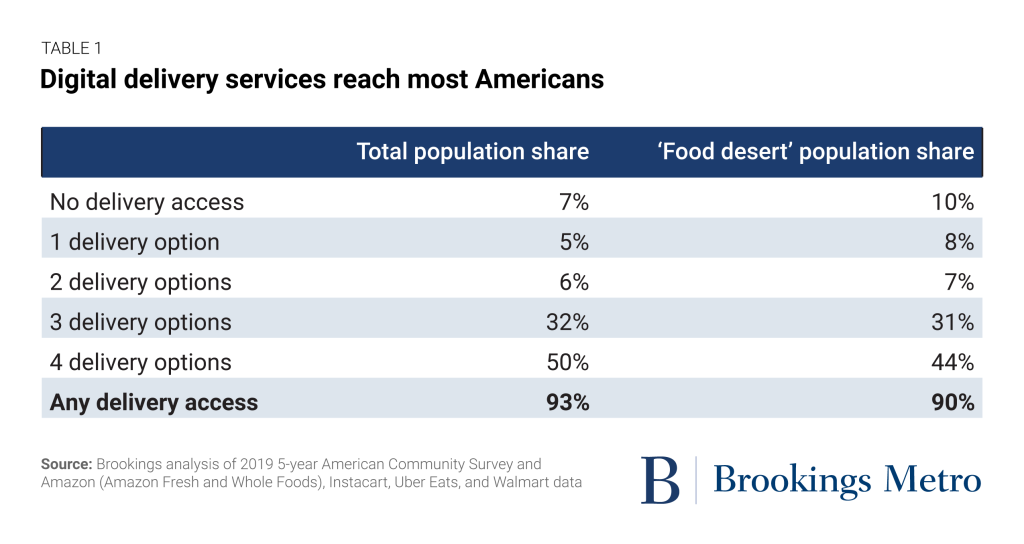

Based on a detailed analysis in a companion brief, we found that digital food delivery services reached 93% of America’s population, including 90% of the population living in traditionally defined “food deserts.” Data from SNAP’s Online Purchasing Pilot also confirms the surging demand for and use of digital food services. However, digital food access is only useful if households have a fixed or mobile broadband connection, a compatible device, digital literacy skills, awareness of the option, and the available income to purchase food this way. Similarly, there are unaddressed gaps in digital food delivery access in many small towns and rural areas.

While digitalization can unlock efficiencies in powerful ways, it also has the potential to amplify injustices already present in our digital and food systems. As the digital food system matures, now is the time to design policies that harness digitalization for the public good.

Digital technology is revolutionizing the food system

From farm to fork, digitalization now touches every part of the food system. Innovative climate and crop yield modelling can now use machine learning to inform agricultural decisions, while satellite and drone-enabled crop monitoring and precision agricultural techniques facilitate targeted crop treatments. Yet many of these cutting-edge technologies are concentrated in industrial row-crop agriculture, are not tailored to the needs of smaller growers, and are limited by broadband availability in rural areas.

Digitalization also enables more advanced food safety protocols, including the Food and Drug Administration’s recent focus on tech-enabled traceability and smarter food safety systems. However, food processing workers and supervisors may not be widely trained on how to use these new technologies to make their deployment successful.

Warehousing, distribution, inventory management, and routing services are undergoing a watershed transformation toward automation. Grocery stores are increasing the use of automated checkout systems and smart shopping carts, forcing cashiers to learn new skills in troubleshooting automated checkout machines when they break down. In the kitchen, scan-and-search recipes and nutritional information are now commonplace, and increased use of digital routing and logistics services facilitate food rescue—the rapid donation of perishable food from restaurants, cafeterias, and other large kitchens to nearby food banks and pantries.

But the most visible aspect of the digital food system to American households is online food purchasing and food delivery.

COVID-19 dramatically accelerated the use of online food purchasing, whether in grocery stores or from restaurants. Brick Meets Click estimates that monthly online grocery spending grew from $2 billion in August 2019 to $6.5 billion in March 2020, and $8.6 billion in November 2021. Even before the pandemic, established e-commerce actors such as Amazon started edging into the food business through the sale of shelf-stable and pantry goods, and several have since expanded into comprehensive online grocery shopping. Superstores such as Walmart and Target expanded their online food ordering options for pickup and delivery. Meal kit subscriptions are growing in popularity, offering recipes and ingredients to fit a variety of food preferences and dietary restrictions. And digital platform actors, including ride-sharing and task-sharing services (or “delivery aggregators”), now offer last-mile delivery of restaurant meals, convenience foods, and groceries. A Pew Research Center survey from August 2021 found that 37% of U.S. adults used delivery apps to order from a restaurant or store and 24% used an app to order groceries or household items within the past year.

Digital food services may change how Americans access food, but they do not change the fundamental goals of a healthy food system: to provide everyone with reliable and affordable access to nutritious, culturally affirming food while ensuring dignity, sustainability, and justice for the workers and land that make it possible.

The success of the digital food system, then, should not be judged by share of retail sales or company valuations. Instead, the true success of the digital food system will be measured by how well it reduces food insecurity, facilitates environmental stewardship, and advances prosperity among workers and business owners. This brief specifically focuses on the potential food access implications of our digitalizing food system while highlighting key questions on these other critical outcomes.

Delivery services redefine food access in the digital age

Our prior research explored the challenges of measuring food access in the complex and rapidly changing modern food environment. That research identified data gaps around “digital access to food”—the ability to reliably order food (prepared or as groceries) to be delivered to one’s door. Digital access to food may significantly increase overall food access, especially for seniors and individuals with mobility challenges, limited child care, and time constraints.

In-depth analysis in a companion brief reveals the geographic and population-based delivery coverage of four of the most prominent digital food delivery companies: Amazon (Amazon Fresh and Whole Foods), Instacart, Uber Eats, and Walmart. We find that 93% of the country’s population has access to at least one of these four delivery options, while 50% can choose between all four. Critically, delivery zones reach many analog-defined food deserts, bridging the physical barriers to access present in many disinvested communities.

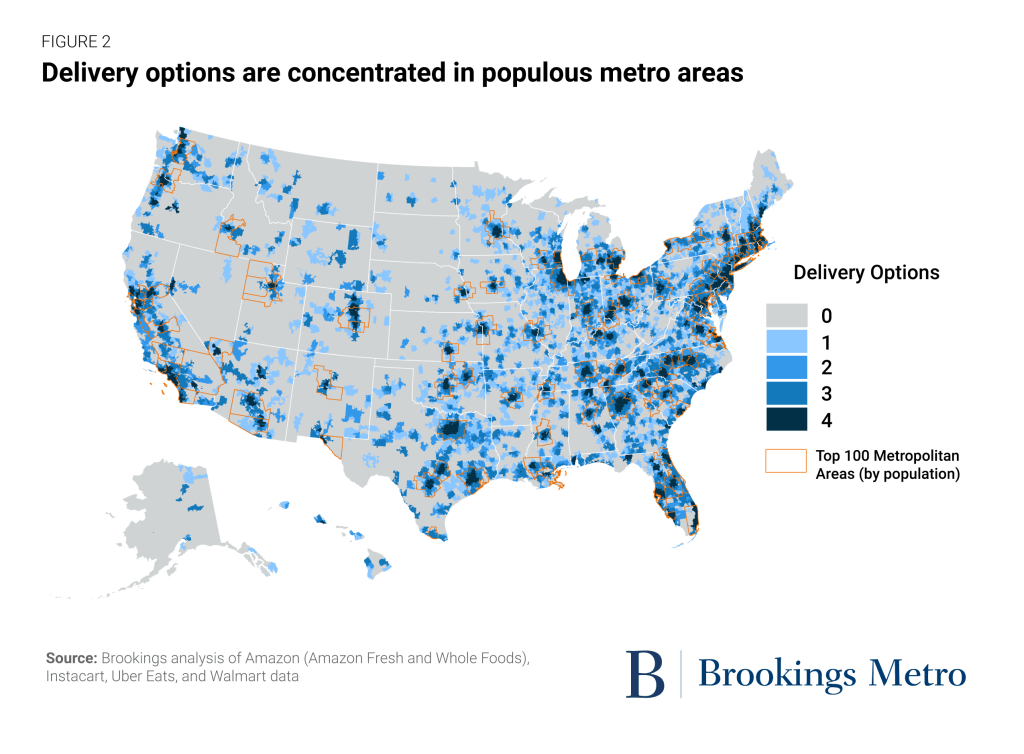

Delivery zones are concentrated where people are; the country’s largest metro areas have the best delivery coverage. Over 99% of people living in very large metro areas (those with populations over 1 million) have access to at least one delivery option. And where there’s one delivery option, there are often more, with 74% of people living in very large metro areas able to choose between all four delivery services we analyzed. However, delivery coverage drops off sharply as population density declines. Only 37% of rural residents have access to any of the digital food delivery services that we analyzed.

Note: Fill color indicates how many (0-4) of the four analyzed platforms completed at least one fresh grocery or prepared food order in each ZIP Code Tabulation Area during Q3 of 2021.

Yet the geography of delivery zones is insufficient to fully understand the geography of digital food access. As we find in our companion brief, many neighborhoods that are technically in delivery zones have low broadband adoption rates due to the lack of infrastructure or access barriers such as price—leaving many residents unable to take advantage of digital food access options. Beyond these measures of access, factors such as food affordability, quality assurance, assortment, awareness, and trust all remain essential as we evaluate the digital food system.

SNAP online purchasing increases online food affordability, but fees and tips add up

Access to food—either digitally or through more traditional brick-and-mortar means—is just one part of the puzzle when it comes to increasing food security. Families also must be able to afford to put food on the table.

Often, affordability is the most critical barrier to food access. The nation’s largest nutritional assistance program, the Supplemental Nutrition Assistance Program (SNAP), provides monthly benefits to eligible individuals and families through Electronic Benefits Transfer (EBT) cards. These cards function similarly to debit cards and can be used at authorized brick-and-mortar food retailers across the country.

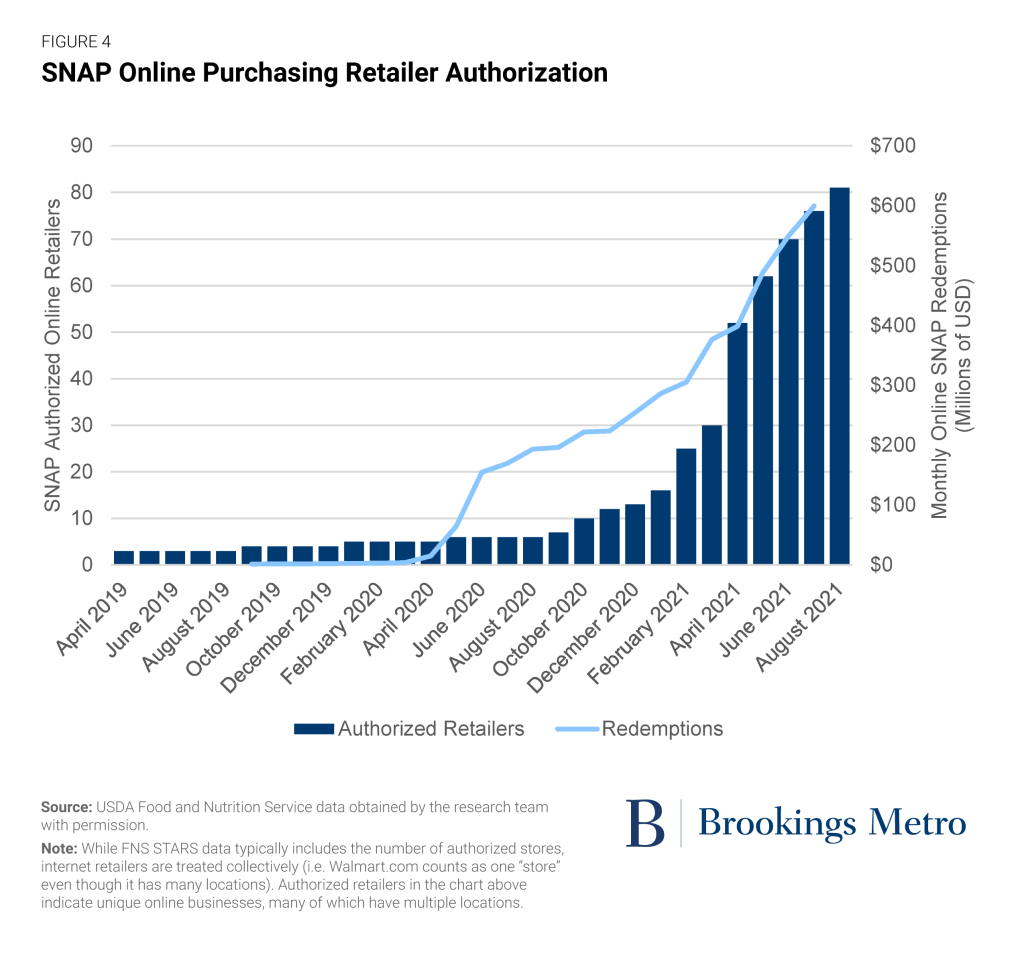

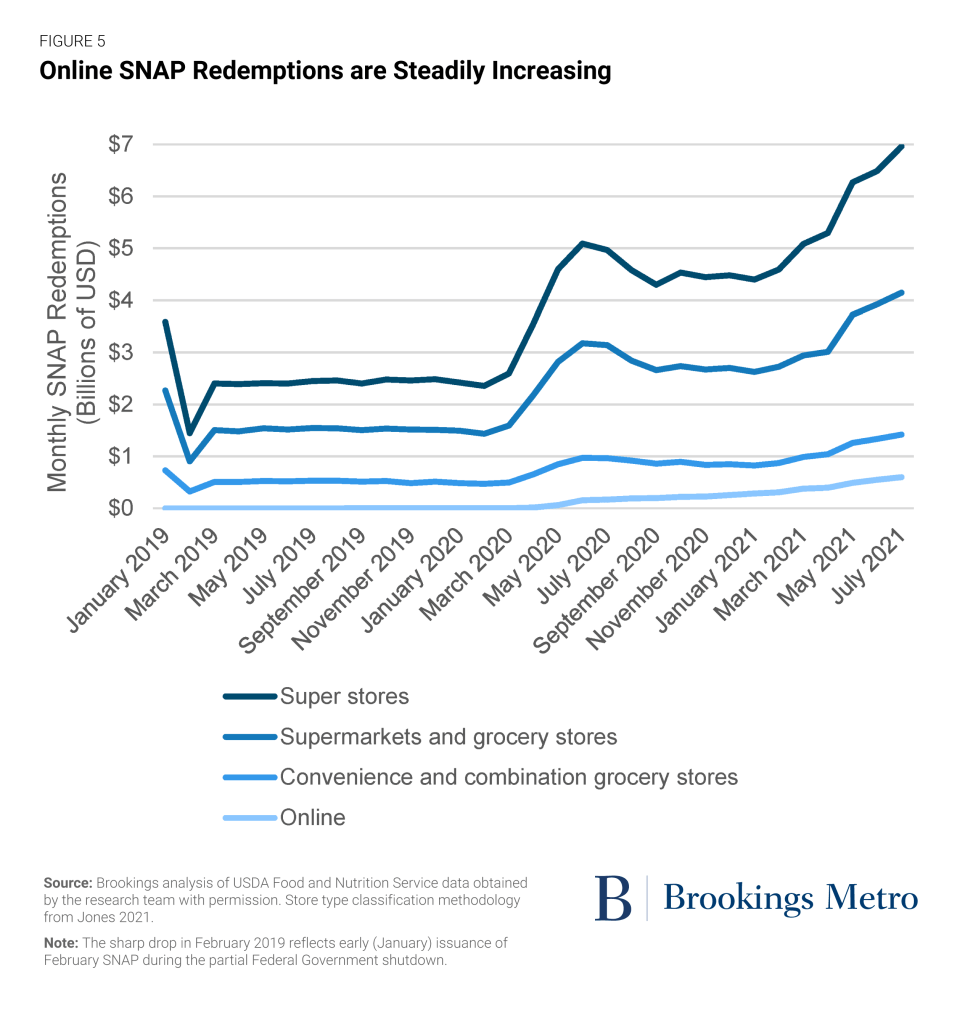

Recognizing the emerging necessity of digital food access, the 2014 Farm Bill established the SNAP Online Purchasing Pilot, allowing select retailers to accept EBT benefits in online food transactions. However, funds could not be used on delivery fees, service fees, or tips. The USDA Food and Nutrition Service initially authorized eight retailers to participate in the pilot across eight states, with New York being the first to go live in April 2019 and Washington joining in January 2020. Four more states went live with the program by April 2020: Alabama, Iowa, Oregon, and Nebraska. In response to the pandemic, the USDA rapidly expanded the pilot beyond its original scope; by June 2020, 29 states were participating. As of May 2022, 49 states and Washington, D.C. offer this purchasing option, allowing SNAP benefits to be used for a mix of pickup and delivery from food retailers across the country.

As with brick-and-mortar food retail, SNAP participation is increasing demand for online food purchasing options. Food retailers across the country have responded to this demand by augmenting existing e-commerce systems to comply with SNAP’s online purchasing protocols, or by creating entirely new e-commerce systems. By September 2021, the program’s eight initially authorized large national retailers (including Walmart and Amazon) had expanded to 81.

SNAP online retailer transactions have been increasing steadily throughout the program’s rollout. A notable increase in transactions in spring 2020 aligns with stay-at-home orders and a concerted effort between the USDA, states, and retailers to expand the program to SNAP participants across the country. The continued growth rate of SNAP transactions at online retailers clearly demonstrates that we are not yet nearing the demand ceiling for SNAP online purchasing. Meanwhile, the program’s demonstrated success has laid the groundwork for the modernization of other nutritional assistance programs, including an online purchasing pilot and task force for the Women, Infants, and Children (WIC) program. The pilot will explore a range of WIC online purchasing frameworks in Nevada, Minnesota, Iowa, Nebraska, South Dakota, the Rosebud Sioux Tribe, Washington, and Massachusetts through July 2023.

Yet even as the rapid growth of SNAP (and soon WIC) online purchasing holds promise for the modernization of our nutritional safety net, it is not a panacea for digital food affordability. Most importantly, the program does not allow SNAP dollars to be spent on fees or tips related to online purchases. These added fees can be cost-prohibitive for customers, although pickup options are likely to be more affordable than delivery. Other affordability concerns—including broadband subscriptions, internet-connected devices, the volatile algorithmic pricing landscape, and systemic differences between brick-and-mortar and digital food prices—will continue to make affordability a barrier to expanding the reach of digital food services.

Digitalization brings new challenges for awareness, quality assurance, and trust

In addition to access and affordability, food quality and consumer experience take a different shape in the digital world and are particularly important for low-income and food-insecure shoppers. When ordering food on a limited budget, spoiled or damaged groceries and package theft are not just frustrating inconveniences, but substantial financial risks.

Early research on SNAP participant attitudes toward online purchasing provides a glimpse into program awareness, trust, and perception. One recent study found that the program’s rapid rollout left some participants unaware of newly available online benefit redemption options. Student researchers also identified gaps in participant awareness of the program and created SNAP online shopping user guides to fill the gap.

Researchers have found low-income and SNAP participant shoppers have varying levels of interest and trust in online purchasing, citing convenience as a driving motivation to buy food online and trust as a barrier. Participants also perceived online shopping as more expensive than in-person options, both due to higher prices and added fees. One study found a preference for delivery over pickup, as well as less frequent purchases of fruit, vegetables, meats, and seafoods online, noting participant experiences about “rotten” perishables and cumbersome return processes. To make online purchasing a viable option for all shoppers, platforms will need to build consumer trust by ensuring product quality and reliability.

The transition to digital food services also requires a high level of digital literacy. User experiences and ordering interfaces vary based on platform, with some being accessible from both desktop and phone and others built primarily for one or the other. Customers must be able to shop, input multiple forms of payment (EBT and additional payment methods to cover delivery and service fees), and track a digital food order—sometimes even communicating with delivery drivers or shoppers through live chats, phone calls, or other means. Last-mile food delivery services hold special potential for elderly and home-bound individuals, but older individuals tend to have lower digital literacy rates.

Lastly, the digital platform—and more importantly, the data it generates—has the potential to magnify discriminatory and predatory marketing practices already present in brick-and-mortar food retail. While the USDA requires authorized brick-and-mortar and online retailers to treat SNAP participants equally to other customers, a report from the Center for Digital Democracy notes that the general public remains unprotected by specific e-commerce or digital marketing regulations; equal protection in this case is a low bar. In the report, researchers find that SNAP online retailers can collect and share much more nuanced and personal data than their brick-and-mortar counterparts, including geolocation, and that their privacy policies are often “incomplete, confusing, and difficult to decipher.” AI-driven marketing can then sort customers into groups by shared characteristics and target individual customers with ads and products across platforms. These practices disproportionately harm vulnerable shoppers, shoppers of color, and low-income shoppers. In this quickly growing marketplace, regulators have a responsibility to protect consumers from potentially discriminatory and predatory practices.

Critical questions for the digital marketplace

Digitalization unlocks many efficiencies, from app-based services that connect customers to multiple retailers to automation techniques that could increase labor productivity. As we seek to feed more people with healthy food, expanding fresh and prepared food delivery could be a huge benefit. But efficiencies are also a force multiplier unto themself. Since the digital food system is still maturing, now is the ideal time to design policies that harness efficiencies for the public good. Below are several critical questions that policymakers and other stakeholders must address as they set out to harness the digital marketplace for public good.

How will market concentration shape the digital food system?

In the brick-and-mortar food system, 20 companies comprise 65.1% of the market share—a jump from just 35% in 1990. Beyond the more immediately visible impacts on small and midsized retailers, workers, and consumers, this high market concentration has been linked to a decrease in produce purchases. Similar patterns can be traced throughout the food value chain, including the biotechnology-driven consolidation of inputs such as crop seeds, which narrows choices and margins for farmers and increases their own consolidation pressure—raising further concerns about environmental and crop resilience. Traditional food policy—including Farm Bill subsidies for industrial agriculture—has failed to prevent these environmental and economic consequences of a highly consolidated food economy.

Concentration is even more dramatic in the online food retailer market, where Digital Commerce 360 estimates Walmart, Amazon, and Kroger comprise a combined 73.6% of online food sales. In May 2020, The New York Times cited Earnest Research, finding similar figures. These market concentration figures also raise new questions in the digital context, especially in the case of third-party platforms; how does their role impact retail partners of various sizes, and how are those impacts passed along to customers? While not all impacts of this highly concentrated digital food marketplace are visible yet, we know from the brick-and-mortar experience that the food economy’s long-term health is powered by a balance of entrepreneurial dynamism and more established companies’ economies of scale.

Policymakers have a unique and urgent opportunity to think proactively about how to regulate the digital food marketplace as it matures.To benefit diverse industry actors of all sizes, the digital food marketplace will need to meet small and diverse growers where they are—in terms of skills, capacity, and even location. By supporting both farm-to-consumer and business-to-business sales, digitalization could strengthen the networks and logistics facilitating regional food hubs. It should also be easy for smaller and startup restaurants and food retailers to digitally connect with consumers and to accept payment for SNAP-eligible foods online. Policymakers will need to keep a close watch on how digital services continue to build wealth across the food industry.

Will digitalization also transform the charitable food network?

The technology enabling digital food services isn’t limited to the for-profit food retail environment. Food banks and pantries across the country also quickly stood-up delivery and pickup models for donated food as the COVID-19 pandemic took hold and demand for emergency food assistance increased. Feeding America even launched its own app, OrderAhead, which translates client-choice best practices to the digital context. While only in its pilot phase, this app has the potential to transform food access experiences across the country as it scales throughout Feeding America’s network of 200 food banks. Digital platforms could help close last-mile access gaps for beneficiaries of the country’s extensive charitable food network, but questions remain as these innovations develop. Will the charitable food network be able to extend pantry delivery services into rural areas where for-profit platforms have not, or will it face the same limitations? Will nonprofit organizations be able to maintain the necessary capacity to administer complex digital systems? Can food banks and food pantries collaborate with other digital literacy stakeholders to increase awareness and access to these emerging services?

How does the rise of digital food deliveries impact the industry’s environmental footprint?

Purchasing food is already one of the most frequent shopping trips American households make, and it’s often done via private automobile. The transition to more deliveries could reduce the total vehicle miles traveled to get food to people’s residences, but only if delivery actors are able to efficiently bundle trips. There are similar questions about whether a transition to more total deliveries could impact the physical location of retail food establishments, including a switch to more warehouse-like facilities. Like ongoing studies of how digitalization is impacting the broader agriculture industry, academics and policymakers should purposely study the connection between food delivery and environmental impacts.

How will the rise of digital services impact food system workers?

Finally, the digital platform brings similar labor questions to the food industry as it has to other sectors. While questions around gig worker status will likely be answered at a macro scale, food delivery calls particular attention to its complexities. The increased food access these delivery services provide currently relies on workers whose jobs are notably less protected and stable than those of unionized grocery workers. Yet policies protecting these workers will need to be carefully designed to prevent downstream effects that could price out the vulnerable and food-insecure customers who would benefit from delivery services. Other digital trends—such as automation and artificial intelligence—are also already impacting delivery jobs, food industry workers, growers, and processors in uneven ways. These trends are shifting the nature of food systems work, and merit careful consideration by labor experts, advocates, and policymakers.

Recommendations

The surging availability of digital food deliveries creates a clear need to design policies that harness digitalization of the consumer-facing food system for the public good. The following recommendations focus on creating digital food system equity, with a particular emphasis on opportunities for federal and state reforms.

Modernize

The federal government must ensure that in any case where public benefits are delivered or spent through digital platforms, beneficiaries are properly protected from harmful marketing practices and best-in-class privacy standards are developed and enforced. While the Center for Digital Democracy outlines key actions the USDA should take to protect SNAP online purchasing participants, the authority to govern user data currently falls outside the purview of the USDA or any single agency. Depending on broader federal privacy and data rights legislation, partners at the Federal Trade Commission and/or the Federal Communications Commission will likely need to be involved.

As onboarding to the digital marketplace can be challenging, the federal government should provide specialized technical assistance to small businesses. Over time, the USDA should compile best practices for onboarding these smaller businesses to the SNAP online purchasing environment to create an approachable and streamlined pathway. The federal government should also find the ideal agency—the Small Business Administration, USDA, or others—to provide qualifying small businesses with training on digital best practices and how to maintain important community food system connections in the digital environment. It’s similarly important to keep working on business practices and public policies that protect the digital privacy and security of customers.

Experiment

When budgets get tight, individuals and households face impossible tradeoffs: food versus medicine, rent versus gasoline, etc. The end users of food assistance programs like SNAP often also qualify for other forms of support from the government, but they typically need to apply for each program separately, which increases red tape and complicates decisions about what to enroll in (e.g., concern that you will lose eligibility for one program by participating in another). Recognizing broadband’s role as an essential prerequisite for digital food access, the USDA should work with the FCC and the National Telecommunications and Information Administration to pilot integrating eligibility processes for SNAP benefits and other utility assistance programs such as the Affordable Connectivity Fund. Through waivers, federal agencies and willing state partners could collaborate to target neighborhoods that perform well on delivery access but face low physical food access and low broadband adoption. Ideally, this pilot is only a precursor to a new federal affordability program to bundle digital and other essential services like the Low Income Home Energy Assistance Program (LIHEAP).

The federal government is uniquely positioned to study how automation could impact food industry workers. Working with state and local government partners, federal officials within the Department of Labor and other relevant agencies should study how emerging technologies are changing the tasks and employment dynamics of common occupations within the food industry—and where technologies may create new tasks and job growth in the future. Ideally these would include purposeful case work across the growing and processing (USDA), distribution (Department of Transportation), and retail (Department of Commerce) industries. As tasks begin to shift within occupations to add more digital tools, it is also likely that employers and actors along the chain will require some incentives to train and retrain their existing workforce (Department of Labor and Department of Education) as well as additional funds to build a stable pipeline of workers who have the combined experiential knowledge in agro-foods and technical skills (such as biotechnology or robotics) to support growth, security, quality, and innovation. Work-based learning, such as apprenticeships and incumbent worker training, can not only help spur innovation but also reduce the risk of layoffs and long-term unemployment as workers adapt to changing processes and technologies.

Measure

Digital food services also demand researchers, policymakers, and other community advocates reconsider the geography of food access. In just a few short years, it’s become clear that the geography of food access must evolve beyond a traditional “food desert” framing. As digitalization offers new food access strategies, closely watching who benefits from digital deliveries and quickly identifying and addressing barriers to adoption will become critical. Due to their natural intersections, monitoring the parallel changes in brick-and-mortar and online food retail patterns will be essential, with a keen eye for places where either option supersedes or crowds out the alternative and decreases the available access strategies for residents.

Digital food access data should be public and easily accessible, especially for digital food providers participating in SNAP (and eventually WIC) online purchasing. The USDA should steward a public SNAP delivery service area map, showing up-to-date delivery service areas for all SNAP-authorized online retailers. The USDA should also conduct thorough surveys of online SNAP and private digital users to compare their behavior and track barriers to adoption.

Additionally, the USDA should start measuring digital food access in its various research activities, including adding public and private delivery zone data to the Food Access Research Atlas and recalibrating measures of food access for the digital age.

Conclusion

The emergence of digital food delivery services is still in its relative infancy, but it’s already claimed a significant share of food retail sales and upended decades of assumptions built into food access research and policymaking. The goal to physically locate food establishments in underserved and under-resourced neighborhoods may no longer be communities’ only option in the face of access barriers, but there is newfound urgency to bring all people online and make delivery more affordable. Meanwhile, upstream, digital food access and other physical technologies require fresh looks at food industry employment and wealth creation opportunities.

There are reasons to be confident that digital food systems can feed more people, build more wealth, and better protect natural land; the digital platform is that powerful. But the stakes are too high—and the history too fraught—to expect only positive, equitable outcomes if market forces and existing policy structures are left unsupervised. Policymakers, researchers, and their peers need to find ways to harness digital change for public good.

About the Authors