The Federal Reserve just released the macroeconomic scenarios that banks will use for the stress tests in 2018, as mandated by the Dodd-Frank Act. The stress tests are designed to help ensure that the largest banking institutions would have enough capital to continue to lend even in a severe recession and to avoid a financial crisis.

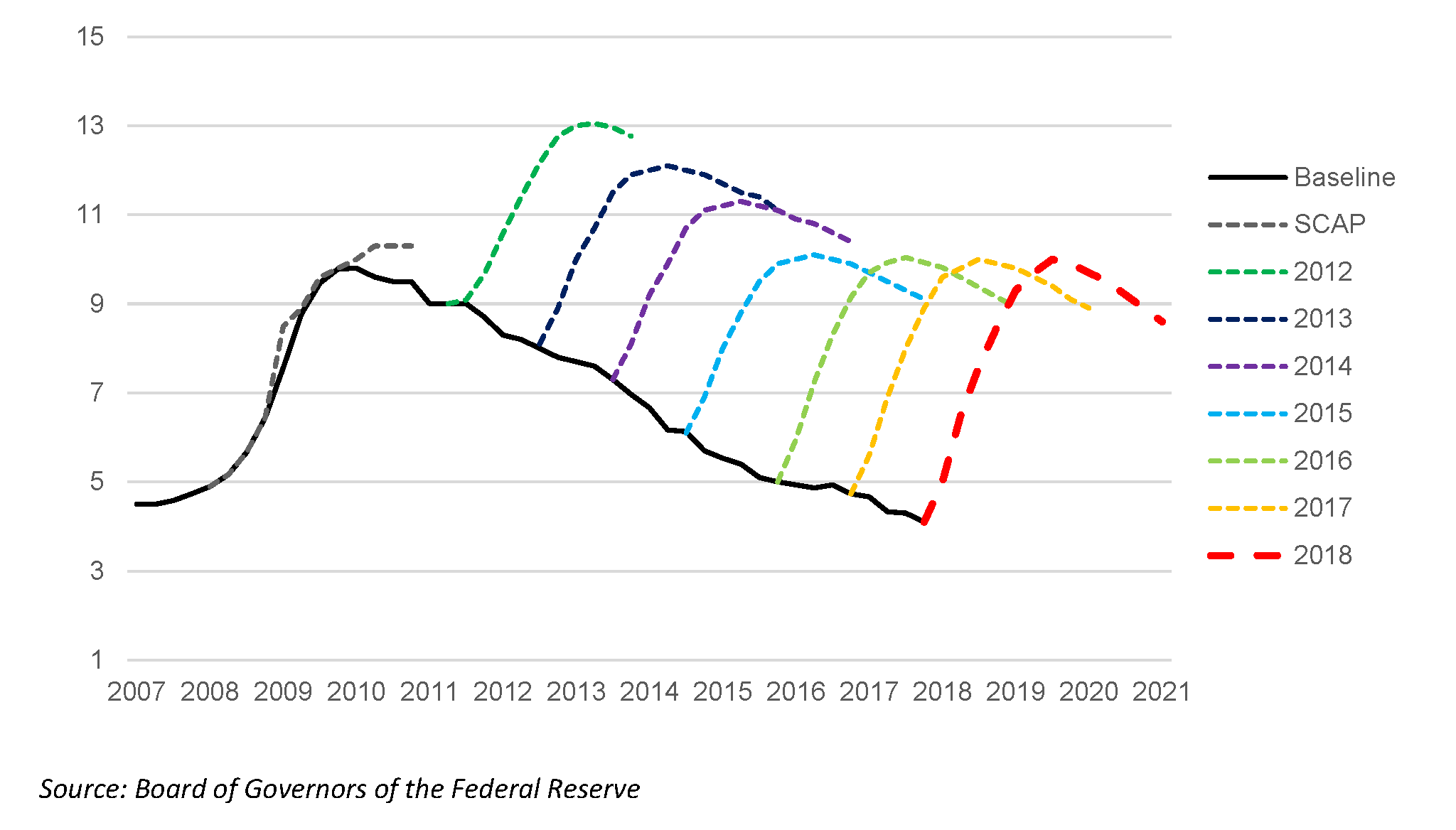

The “severely adverse” scenario for 2018 is appropriate given the strength of the economy, and is consistent with the Fed’s framework to include a sharper downturn when the economy has strengthened.1 This year’s severely adverse scenario includes a rise in the unemployment rate to 10 percent (Chart 1), a steeper yield curve, and a sharp deterioration in corporate bond and real estate prices. Critics will likely argue again that the scenario is implausible. They have argued that the severely adverse scenarios of the past couple of years have been excessive, noting that an increase in the unemployment rate to 10 percent would be close to impossible. Aside from the fact that recessions are hard to predict, this argument misses the point of macro-based stress tests. Moreover, authorities now have less powerful recession-fighting tools than in previous decades.

Chart 1: Unemployment rate and projections under severely adverse stress test scenarios

Percent, quarterly

To promote macroeconomic stability, scenarios need to be severe, forward-looking, and dynamic.2 A scenario should provide assurance that banks could withstand a deep recession conditional on a recession occurring, not conditional on whether a recession is likely. The importance of severity for credibility was all too apparent in the initial stress tests (SCAP), when investors became anxious that the actual unemployment rate was rising nearly as quickly as in the stress scenario (Chart 1). Had the actual rate overtaken the scenario rate before the results were released in May 2009, the reaction to the stress test results almost surely would have been less favorable. In the end, the large estimated losses due to the assumed sharp rise in the unemployment rate and steep fall in house prices, and the substantial capital raises by banks, contributed to restoring public confidence in the banking system.

Scenarios also need to be forward-looking, and should not assume that past strong performance is an indicator of future strong performance. Preserving the countercyclicality of the scenarios this year was critical.3 Countercyclical features work to offset natural tendencies of lenders to loosen underwriting standards and accept lower compensation for risk when economic conditions and loan performance have been strong. With current loan loss rates low and loans growing, the public needs to know that banks are doing a careful assessment of new risks they are taking, and are not just looking backwards when assessing risks.

Recent findings by the Bank of England’s Financial Policy Committee highlight the idea that good times lead to over-optimism. Because the banks haven’t been experiencing many losses on consumer loans in the past couple of years, they estimated few losses in their stress tests this past summer. After reviewing the estimates, the FPC decided to provide guidance to banks to use higher loss estimates based on models that were more forward-looking, noting signs in some markets of “excessive weight being placed on recent benign conditions as an indicator of future risks. This behavior encourages greater risk taking, potentially building up greater vulnerabilities.”4

Dynamic scenarios that include new and varied “salient risks” also are important for financial stability. This year’s scenario includes a steeper yield curve and sharp corrections in corporate bond and real estate prices, as well as a steeper recession in Asia than in last year’s scenario. Salient risks in previous scenarios included those arising from commercial real estate, negative interest rates, and disruptions in bond market liquidity. Dynamic scenarios lead to better assessments by banks because of the range of possible risks, and help to prevent static backward-looking assessments.

Despite complaints of ever-increasing severity, the estimated loss rates for loans as well as the implied capital requirements have been declining each year. Table 1 shows that the estimated loss rates on loans under the severely adverse scenario fell sharply from 9.1 percent in 2012 for 19 firms to 5.8 percent in 2017 for 34 firms. Estimated loss rates under severely adverse scenarios of a rise to a 10 percent unemployment rate fell from 6.1 percent in 2015 to 5.8 percent in 2017. The lower estimated loss rates even with the same unemployment peak of 10 percent reflect the better economy and higher asset prices, which provide stronger starting points for estimating losses, and some offset to the sharper deterioration assumed in the stress test scenarios. These effects are seen most clearly in the loss rates for residential first and junior mortgages, which fell sharply especially since 2014. Moreover, with estimated revenues higher in the stress scenarios, most banks have been increasing their proposed dividends and share repurchases in recent years and not hitting a constraint.

| Table: Project loan losses under the severely adverse scenario, by type and year (Percent over nine quarters) | ||||||

|---|---|---|---|---|---|---|

| Projected Loan Losses (%) | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| Total | 9.1 | 7.5 | 6.9 | 6.1 | 6.1 | 5.8 |

| Mortgages, first lien | 7.3 | 6.6 | 5.7 | 3.6 | 3.2 | 2.2 |

| Mortgages, junior and HELOCs | 13.2 | 9.6 | 9.6 | 8.0 | 8.1 | 4.5 |

| Commercial and industrial | 8.2 | 6.8 | 5.4 | 5.4 | 6.3 | 6.4 |

| Commercial real estate, domestic | 5.2 | 8.0 | 8.4 | 8.6 | 7.0 | 7.0 |

| Credit Cards | 17.2 | 16.7 | 15.2 | 13.1 | 13.4 | 13.7 |

| Other | 8.2 | 7.9 | 8.7 | 8.7 | 9.1 | 9.5 |

| Number of firms | 19 | 18 | 30 | 31 | 33 | 34 |

Still some argue that it is much less likely that the unemployment rate would rise again as sharply as in 2008-09, given that banks now have much more capital and liquidity, and the rest of the financial sector is less leveraged. That position has merit, and is an important justification for the more stringent bank regulations that have been put in place since the financial crisis. However, there are some important counterarguments to the “this time is different” proponents, because other policy tools available to cushion a possible recession now are less powerful.

First, monetary policy responses may be more limited. The Fed cut the federal funds rate aggressively in the financial crisis to offset the contractionary effects of bank distress. The FOMC cut rates from above 5 percent at the beginning of 2007 to almost zero by the end of 2009. With the policy rate currently at a target between 1-1/4 and 1-1/2 percent and expected by the FOMC to settle around 2-3/4 percent in the steady state, it could not cut rates as aggressively as it did then to support the economy.

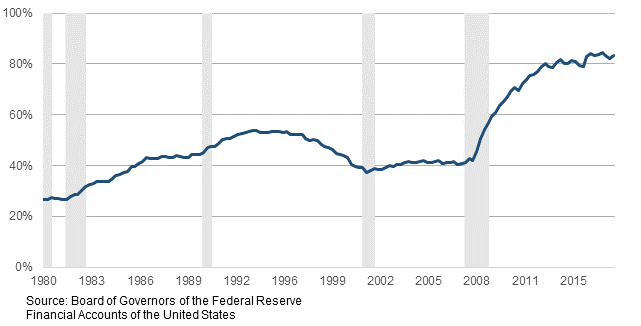

Second, fiscal policy has much less space now than in recent decades to help cushion a downturn. The federal debt-to-GDP ratio has risen from about 40 percent in 2007, just before the height of the crisis, to more than 80 percent in 2017 (Chart 2). This increase took place even before the recent tax bill, which is projected to add at least $1.5 trillion to the federal debt over the next ten years.5Chart 2: Federal Debt

Percent of GDP, quarterly

Third, financial authorities have more constraints on responding to severe disruptions in the financial system in the future. New limits, such as on liquidity provision by the Fed under 13-3 or debt guarantees by the FDIC, suggest that actions taken by authorities to protect the economy might not be as effective in the future as they were in the crisis.

For these three reasons, it is quite plausible that the next recession will be severe for even moderate-sized shocks.

The Fed’s 2018 scenarios with a more severe downturn and new salient risks help to maintain the credibility of the stress tests and support macroeconomic stability. A robust stress testing system helps to ensure that the banking system as a whole is resilient to common macro credit and market risks against which they cannot collectively diversify.

Related Content

Authors

-

Footnotes

- The scenario is consistent with the framework for designing stress test scenarios, as described in 12 CFR 252, Appendix A.

- The proposals that the Fed released for public comment in December 2017 offer some areas for improving scenario design, which are consistent with maintaining severity, countercyclicality, and dynamic risks.

- See Policy Statement on the Scenario Design Framework for Stress Testing http://www.federalreserve.gov/bankinforeg/bcreg20121115a4.pdf, and Liang (2013), Implementing Macroprudential Policies, https://www.financialresearch.gov/conferences/files/implementing_macroprudential_policies_may31-2013.pdf

- Financial Policy Committee statement from its meeting, 20 September 2017. https://www.bankofengland.co.uk/statement/fpc/2017/financial-policy-committee-statement-september-2017

- The estimated addition would be less, $1.1 trillion, when growth effects are incorporated. Source: Joint Committee on Taxation, Estimated Budget Effects of the Conference Agreement for H.R. 1, the “Tax Cuts and Jobs Act,” https://www.jct.gov/publications.html?func=startdown&id=5053, retrieved January 10, 2018.