This post was updated on March 8, 2021 to clarify that the data include both individuals who completed their degree and undergraduate students who did not complete their degree.

President Biden made headlines recently when he expressed reluctance to forgive large amounts of student debt owed by well-off students at elite schools. “The idea that … I’m going to forgive the debt, the billions of dollars in debt, for people who have gone to Harvard and Yale and Penn …” he said, not finishing the sentence but leaving listeners with no doubt about what he thinks. There are real tradeoffs involved: “[I]s that going to be forgiven, rather than use that money to provide for early education for young children who come from disadvantaged circumstances?”

Biden was right. Even though elite schools represent a small fraction of all undergrads, affluent students at elite schools borrow a lot. In 2014 (the last year for which data was available), Harvard students owed $1.2 billion, Yale students $760 million, and University of Pennsylvania students a whopping $2.1 billion, according to an analysis I produced with Constantine Yannelis. Students at other elite schools, like the University of Southern California, NYU, and Columbia, owed billions more.

According to the Department of Education’s College Scorecard, students who graduated or withdrew in 2017 or 2018 from elite or highly selective colleges and graduate programs (as ranked by Barron’s) owed about 12 percent of all student debt in those years, but account for only four percent of all borrowers.

Students from elite colleges owe a disproportionate share of student debt in part because of the large graduate and professional degree programs at those schools. Harvard, for example, is the country’s largest law school, most of its students borrow, and the average borrower graduates with about $143,000 in student loans. Harvard Law graduates probably owe taxpayers more than half a billion dollars—loans they can and should pay back. And that applies not just at Ivy League schools but at many institutions with advanced degree programs. Nationwide, more than 40 percent of student loans were used to pay for graduate or professional programs. And the degree programs that are the largest sources of student debt are MBA programs and law schools.

Some undergraduate students from elite colleges also accumulate student debt because their institutions are more expensive, they have longer academic careers, and they are more likely to go on to elite graduate and professional programs that pay off handsomely in higher wages. They are often the ones with the largest amounts of student debt but also the ones who gained the most from their education.

In contrast, students at nonselective schools, two-year colleges (mostly community colleges), and for-profit institutions owed about 24 percent of all student debt in the classes graduating or leaving college in 2017 and 2018, but accounted for about 40 percent of all borrowers. On average, they borrow less than their peers at more selective institutions (especially at public institutions). Partly, that’s because their programs are less expensive. Partly, it’s that students at such schools are more likely drop out before completing a degree (and thus borrow for fewer years). Partly, these students are from lower-income households and likely qualify for more grant aid (which reduces the amount they can borrow).

These borrowers are most likely to struggle with their loans and need help. They’re not from as affluent households as students at other institutions. Their post-college earnings are lower. They’re more likely to have student debt without a degree and to fall behind and default on their loans. These borrowers live a world apart in educational attainment, socioeconomic background, and economic success from the students that attend elite public and private non-profit institutions. The only thing they have in common is their student loans.

The right policy is to provide relief to borrowers who are struggling—without providing a windfall to those who are not. That’s why Biden’s stated approach, to base loan relief on the economic circumstances of the students and their families and how and where they accumulated their loans, is the right approach.

One way to understand the differences between borrowers—and the rationale for a targeted approach to loan relief—is to examine the institutions responsible for the largest amounts of student debt and the characteristics of their students.

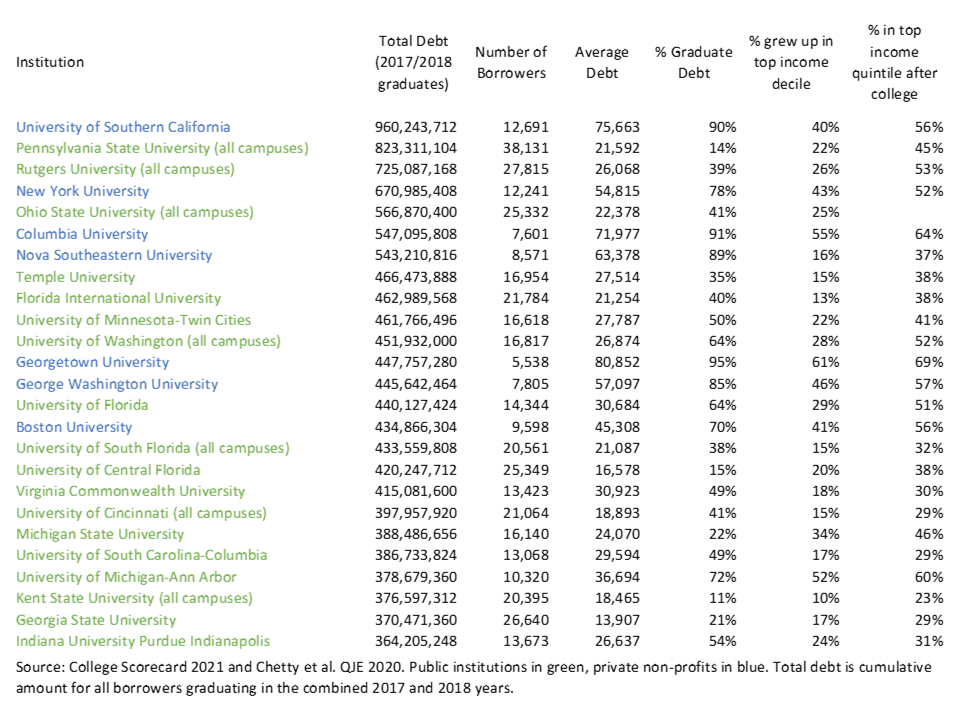

The following table presents the 25 public and private non-profit institutions where students who graduated or withdrew from college in the 2017 or 2018 academic year borrowed the most, as measured by the College Scorecard’s institution and program-level data.[1] (I have removed for-profit and online institutions, which otherwise dominate the list of institutions with the most indebted students.) Public institutions are in green; private non-profits are in blue. For each institution, I provide graduating students’ total debt (which is for a two-year period), the total number of borrowers, the average debt per borrower, and the fraction of total debt that is from graduate programs. Where available, I’ve also provided the fraction of undergraduate students who grew up in families in the top 10 percent of the income distribution and the fraction of undergraduates whose own earnings place them in the top 20 percent of the income distribution after college (based on estimates from Chetty et al 2020).

Click on table to enlarge.

The list shows that the institutions where students borrow the most vary widely in their cost and quality, in the economic backgrounds of their students, and in the success and ability to pay of the graduates after college.

The largest source of student debt is the University of Southern California—the institution at the center of the bribery scandal in which rich parents sought to assure their kids of an admissions slot. In the characteristics of its students, it is representative of many elite schools. Among undergraduates, 40 percent grew up in the top 10 percent of the income distribution. After college, they’re much more likely to end up as a high-earning individual. Most of the debt of USC students is from the school’s highly-ranked graduate and professional programs. The pattern is similar at NYU, Columbia, Georgetown, George Washington, and Boston University.[2]

Many highly selective public colleges, like the University of Michigan’s Ann Arbor campus, look similar to their elite private peers in the affluence of their undergraduate student body, significant graduate programs, and post-college success. But the variation is large: at some schools (like Penn State), most debt is owed by undergraduate students. At VCU, or University of Minnesota, or University of Florida, a large share of debt is owed by graduate and professional degree students. While undergraduate students at public institutions are less likely to have grown up in a high-income family, they are from more affluent backgrounds than the average person, and are more likely to reach the top 20 percent of the income distribution after college.

A surprising fact is that, despite their apparent affluence, undergraduate students at many elite schools do borrow. About a third of undergrads at Georgetown, NYU, George Washington, and USC owe student loans, even though 61 percent of Georgetown students grew up in families in the top 10 percent of the income distribution, as did 43 percent at NYU and 46 percent at George Washington.

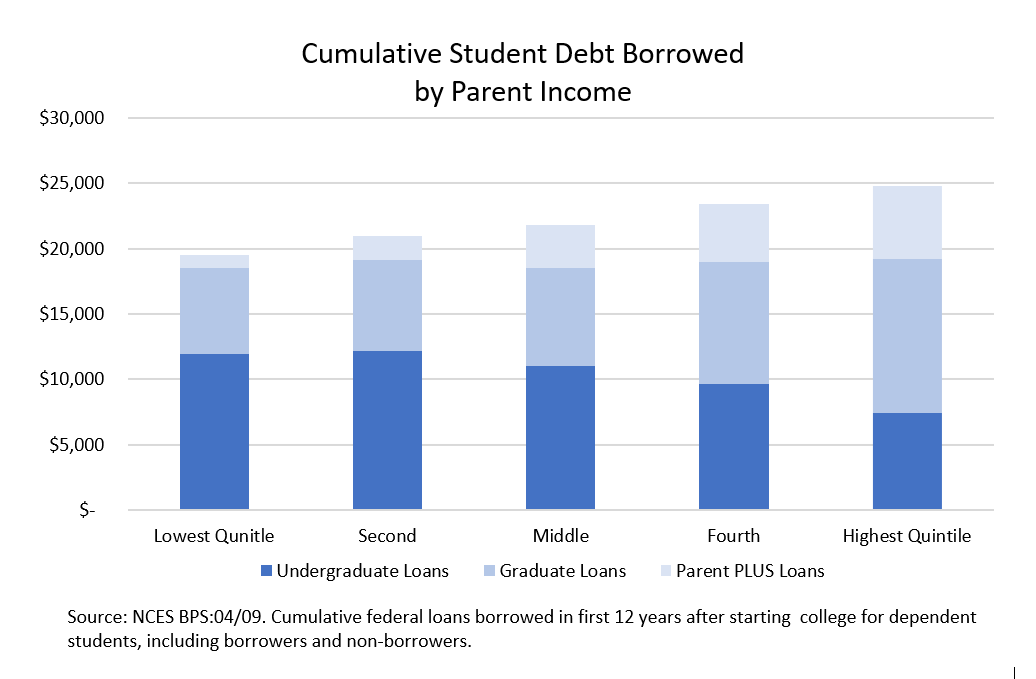

Why do high-income students borrow? One reason is that they go to the most expensive colleges in the country. High-income families borrow to buy a house; many do the same to finance their kids’ elite college education, which can cost just as much.

Another reason they borrow is because they can: there is no income or wealth limit for receiving federal financial aid. Loan eligibility is determined by the cost of attendance minus grant aid, not by family income. A child of millionaires is eligible to borrow the same amount in student loans as a student who grew up in poverty. Indeed, the millionaire is often eligible to borrow more because they do not qualify for grant aid, attend a more expensive college, and are more likely to complete college and go to graduate school.

As a result, students borrow similar amounts for their education regardless of their family income. This chart shows the cumulative amount borrowed over a 12-year period by dependent students who first enrolled in 2004. While students from the highest-income families borrow somewhat less than their low-income peers as undergraduates, they are more likely to borrow in graduate or professional degree programs. On average, that nets out, and there is little difference in the amounts borrowed by high-, middle-, and low-income students. The exception is that high-income parents are much more likely to borrow through the Parent PLUS program to finance their children’s more expensive college degrees. As a result, the total amount of debt borrowed by the families in the highest-income quintile is about 27 percent greater than owed by families in the lowest-income quintile.

Click on chart to enlarge.

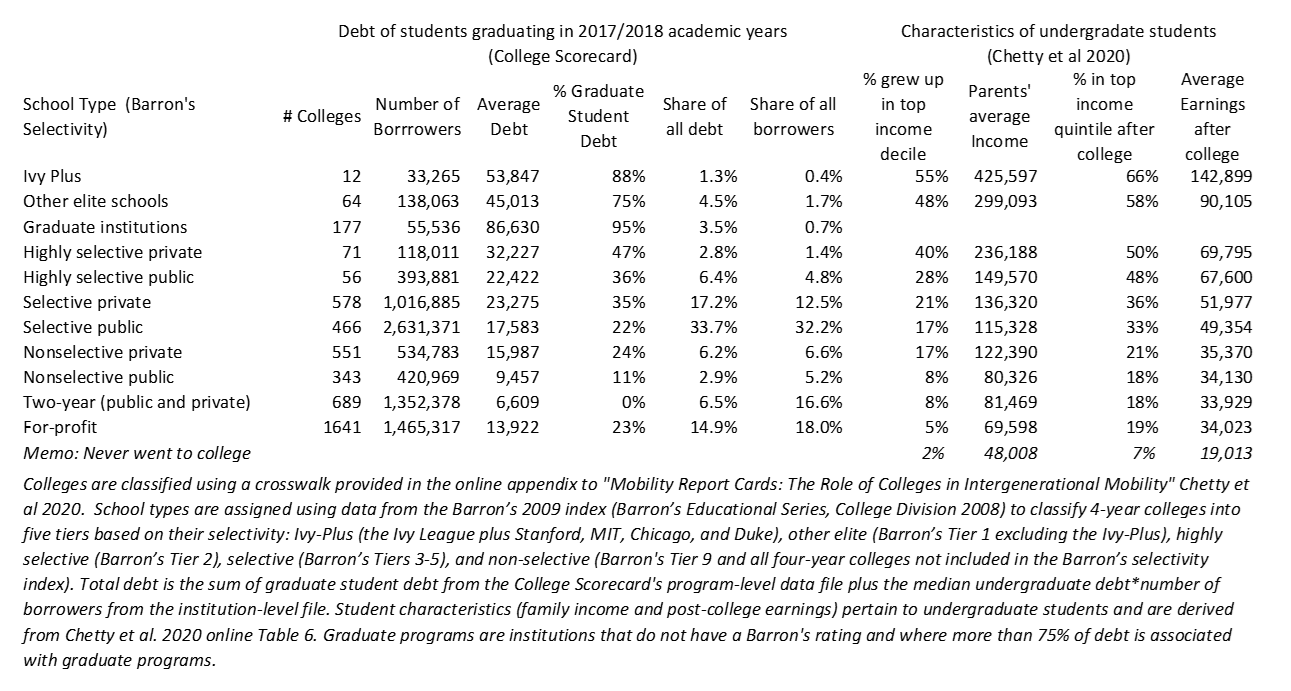

Of course, not all college students are affluent or end up high in the income distribution. Zooming out, the following table categorizes all colleges and graduate programs represented in the College Scorecard by their selectivity using Barron’s college rankings. The left panel of the table describes the debts owed by students at these colleges. The right panel describes their family economic background and their post-college outcomes.

At the top of the list, borrowers at elite schools, graduate-only institutions (like UCSF’s medical programs), and highly selective public and private colleges owe about 12 percent of all student debt—but make up only four percent of students. Many students at elite schools are from affluent backgrounds and are more than 2.5 times more likely to end up in the top quintile than the average American (50 percent versus 20 percent).

Click on table to enlarge.

At the other end of the list, worst off among all these borrowers are those who have attended for-profit colleges (or similar online schools operated by public and private institutions), which would otherwise have occupied half the list of institutions with the most indebted borrowers. For-profit completers owed about 15 percent of all student debt, according to the Scorecard.

The largest single source of student debt in America is the University of Phoenix, the gigantic online for-profit chain. Students who graduated or dropped out in 2017-2018 owed about $2.6 billion in student loans; two years after graduation, 93 percent of borrowers have fallen behind on their loans. A large number of borrowers attended other notorious for-profit chains, including Argosy (whose graduates owed $430 million), which collapsed into federal receivership in 2019; Grand Canyon University ($1.1 billion), which is currently ensnared in a legal battle with the Department of Education over its attempts to become a non-profit; DeVry ($700 million), which recently paid $100 million to students it defrauded as part of a settlement with the Federal Trade Commission; and Walden University ($712 million), the nation’s largest producer of indebted African American PhDs, whose students owe an average of about $131,000 at graduation. More than one in ten PhDs awarded to African Americans between 2015-2019 got their degree online from Walden. That is more than four times as many as from the second largest institution, Howard University. There is no doubt that many of the students from for-profit colleges struggle with their loans, particularly many low-income, Black and Hispanic, and first-generation students that are disproportionately recruited into such schools.

Between the extremes of elite Ivy League colleges and notorious for-profit chains are students who went to selective (but not “highly selective”) public and private institutions. These students owe about half of all student debt. Many are from upper middle-class backgrounds and work in middle-class jobs after college. These students are clearly better off than their for-profit and community college peers in the degrees they earned, their family background, and their earnings after college, but not to the degree of students at more selective institutions.

Finally, when thinking about how to help student loan borrowers, it is important to remember that Americans who have never gone to college are vastly more disadvantaged. Only two percent of those who didn’t go to college grew up in the top 10 percent of the income distribution. Their average family income was $48,000. As adults, they earn an average of $19,000 a year.

Biden’s complicated answer to the question of whether he should forgive tens of thousands of dollars per student in debt reflects a complicated situation. Borrowers differ in their family circumstances, the degree they earned (or failed to earn), the quality of the school they attended, and how much they earn after college. Policymakers can base loan relief on these characteristics. The best approach is to use (and improve on) income-based repayment plans, which reduce or suspend loan payments and provide eventual forgiveness to students whose incomes are too low and debts too high. In effect, that policy funds postsecondary education with a progressive tax paid by affluent, successful students that subsidizes their more disadvantaged peers.

In addition, policymakers could provide relief based on where students went to school or the degree they pursued, or their family income at the time they enrolled. Indeed, looking forward, Biden and many progressive policymakers have made it clear what they think the federal government should—and should not—pay for when advocating for doubling the Pell Grant, making public undergraduate education tuition-free for low- and middle-income students, or increasing support for minority-serving institutions. In short: means-tested grants in measured amounts for undergraduate students at good-quality institutions. That seems like a reasonable template for how to help existing borrowers, too. But the parameters of those policies deliberately avoid using taxpayer dollars to pay for graduate and professional degree programs, costs at expensive private institutions, and tuition for the children of high-income families. If policymakers are unwilling to pay those expenses in the future, Biden is right to question whether to forgive those debts from the past.

Note: All figures and their underlying data are available for download here.

[1] Debt data is derived from the College Scorecard, which provides measures of the cumulative debt accrued by program completers over the course of their educational careers. For each institution, I measure total debt as the sum of the median undergraduate balance times the number of borrowers from the institution-level file plus the sum of the average debt per graduate program times the number of graduate borrowers from the program-level file. The institution-level file provides debt balances of undergraduate borrowers who completed their degree or withdrew. The program-level file includes only the balances of borrowers who completed their degree. This results in an unavoidable underestimate of the total debt because some graduate programs have too few students to be included and because average debt per undergraduate is not available. Ideally, the Department of Education would tabulate the total balance of borrowers based on where loans were originated, as we did in 2015.

[2] While the table presents data only for the 2017 and 2018 graduating classes, they mirror the comprehensive accounting we provided through 2014 available here. For instance, in 2014, students from NYU owed about $6.1B; at USC, $5.1 billion; Columbia, $2.8B; Cornell, $1.2B; Georgetown $2.4B; George Washington $2.4B; Boston University $3.0B; University of Michigan Ann Arbor $2.9B.

Related Content

Authors

Commentary

Op-edBiden is right: A lot of students at elite schools have student debt

March 3, 2021