In the United Kingdom, homeownership has fallen while renting is on the rise

Editor’s note: In case you missed it, watch an event held on April 21 discussing lessons from around the world related to policies to support stable, affordable rental housing.

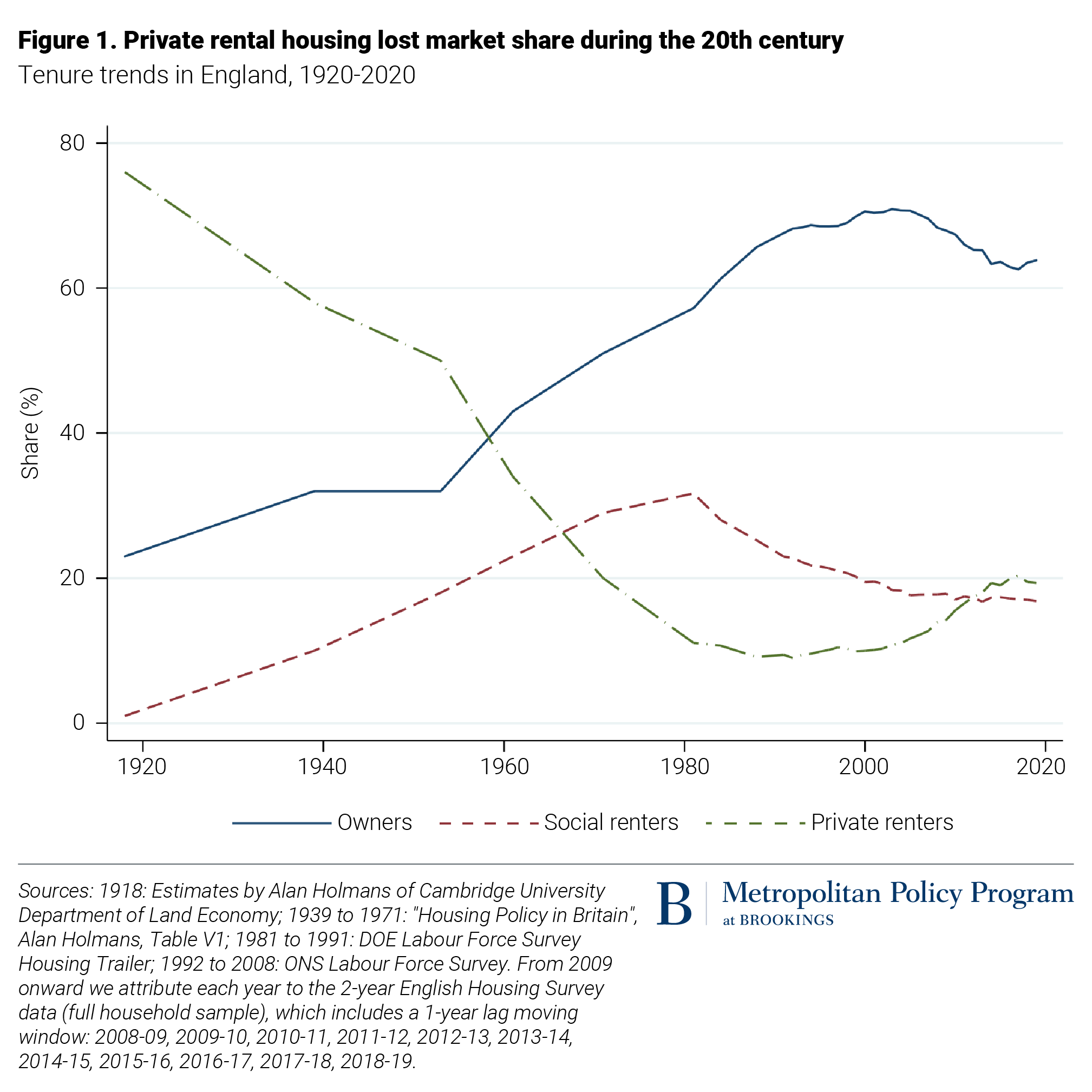

Homeownership has been in decline in the United Kingdom, falling from an all-time high of 70.9% in 2003 to 63.9% in 2018. This decline has coincided with a revival of the private rental market. Due to a lack of moderately priced owner-occupied housing, privately owned and social rental housing is particularly common among young and lower-income households, and in urban areas.

The country’s main political concern is the lack of low- and moderately priced housing (usually referred to as “affordable” housing), which has prompted a flurry of housing policies aimed at improving affordability. However, since the 1980s, the political focus has shifted from providing social rental housing to policies aimed at facilitating access to homeownership. While most of the British government’s policies in response to the COVID-19 pandemic focused on homeownership, some also aimed to protect renters.

Overview of renter households and rental housing

A century ago, the U.K. was by and large a country of renters. From the beginning of the 20th century up to the 1960s, rental housing accounted for the largest share of the housing market (Figure 1). Households in the private rental market declined until the mid-1990s, while the share of social rental housing rose until 1980. Rising incomes and increased availability of building society mortgages (similar to credit unions in the U.S.) contributed to rising homeownership rates, as well as a variety of policies intended to increase homeownership, especially the Right to Buy program since 1980.

Homeownership in the U.K. peaked around 2003. The decline in homeownership coincided with a revival of the private rental market, with the latter roughly doubling its share from below 10% in the mid-1990s to nearly 20% in 2018.

One important feature of Britain’s contemporaneous private rental market is the absence of any form of rent control. Since the Housing Act of 1980, rents are generally set by landlords. In 2019, the government announced that it will put an end to “no fault” evictions, providing tenants with more stability and protection from frequent moves at short notice.

Renting is widespread among younger households; only about 41% of household heads aged 25 to 34 own their homes. Renting is also the most common tenure (at 59.2%) among those with the lowest incomes (households earning less than 300 GBP/week). Indeed, income strongly varies by housing tenure. Owner-occupiers earn, on average, the highest weekly wages (878 GBP), followed by households in private rental housing (641 GBP) and those in social rental housing (369 GBP). More than half of renters live in “terraced” (attached) single-family houses. Roughly one-third live in “flats” (apartments), with the rest living in detached houses. Rental properties have, on average, fewer rooms and higher overcrowding rates.

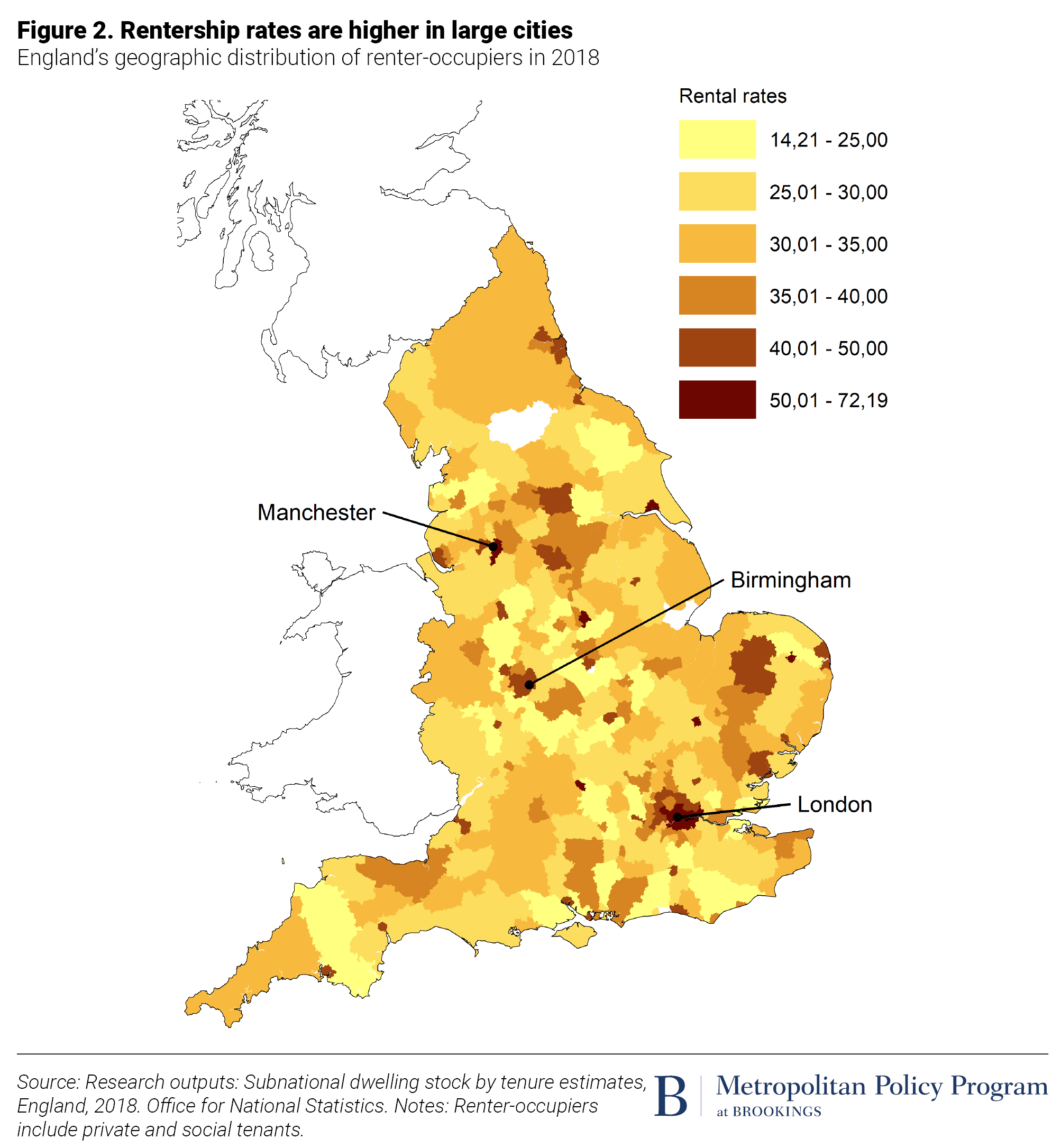

These aggregate statistics hide some important heterogeneity across local areas. Rental housing accounts for a sizable share of the market in major urban areas (such as London, Birmingham, and Manchester) whereas owner-occupation is the most widespread tenure mode in suburban areas and the countryside (Figure 2).

Institutional and policy environment of rental housing

System of land use planning and fiscal centralization

The institutional setting in the U.K. is characterized by two key features, which affect both the owner-occupied and rental markets. First, in contrast to continental European countries, which implemented rule-based planning systems, the U.K. regulates its land use via a rigid “development control” system. In this system, each change of use for any land parcel triggers a public consultation process and must be approved on a case-by-case basis by a local planning authority. The system’s main aim is to limit the spread of urban development into undeveloped “greenfield” areas.

Second, the U.K. has a high degree of fiscal centralization—giving very little weight to local taxes—with the consequence that local authorities have virtually no positive fiscal incentives to permit new residential development. In conjunction with the idiosyncratic development control system that assigns strong political power to local “not-in-my-backyard” residents, the ultimate outcome is that housing supply is extremely unresponsive to rising prices, particularly in major urban agglomerations such as London. In these areas, positive demand shocks have the main effect of increasing land and house prices, leading to a severe housing affordability crisis in large parts of the country, and arguably in part explaining the fall in homeownership attainment since the early 2000s.

Housing in the U.K.—particularly in London and Southeast England—is some of the most expensive and cramped in the world. When considering the buying price per square meter of a “comparable apartment” in a prime central location of a country’s main city, London ranks second, topped only by Hong Kong. U.K. rents are also extraordinarily high. The same comparable apartment in London is also the second-most expensive to rent, again topped only by Hong Kong.

The historic decline of the social rental market

The birth year of social housing in the U.K. goes back to 1919—the year when local authorities (councils) were required by law to provide council housing. The original aim of council housing was to provide decent housing for army recruits; however, the age of social housing only truly arrived after World War II, when the Labour government built more than 1 million homes—80% of which were council homes—largely to replace those destroyed during the war. The house-building boom continued through the 1950s, but, near the end of that decade, the emphasis shifted toward slum clearance. By the early 1970s, the downsides of social housing (lack of investment and maintenance, negative peer effects) became more visible.

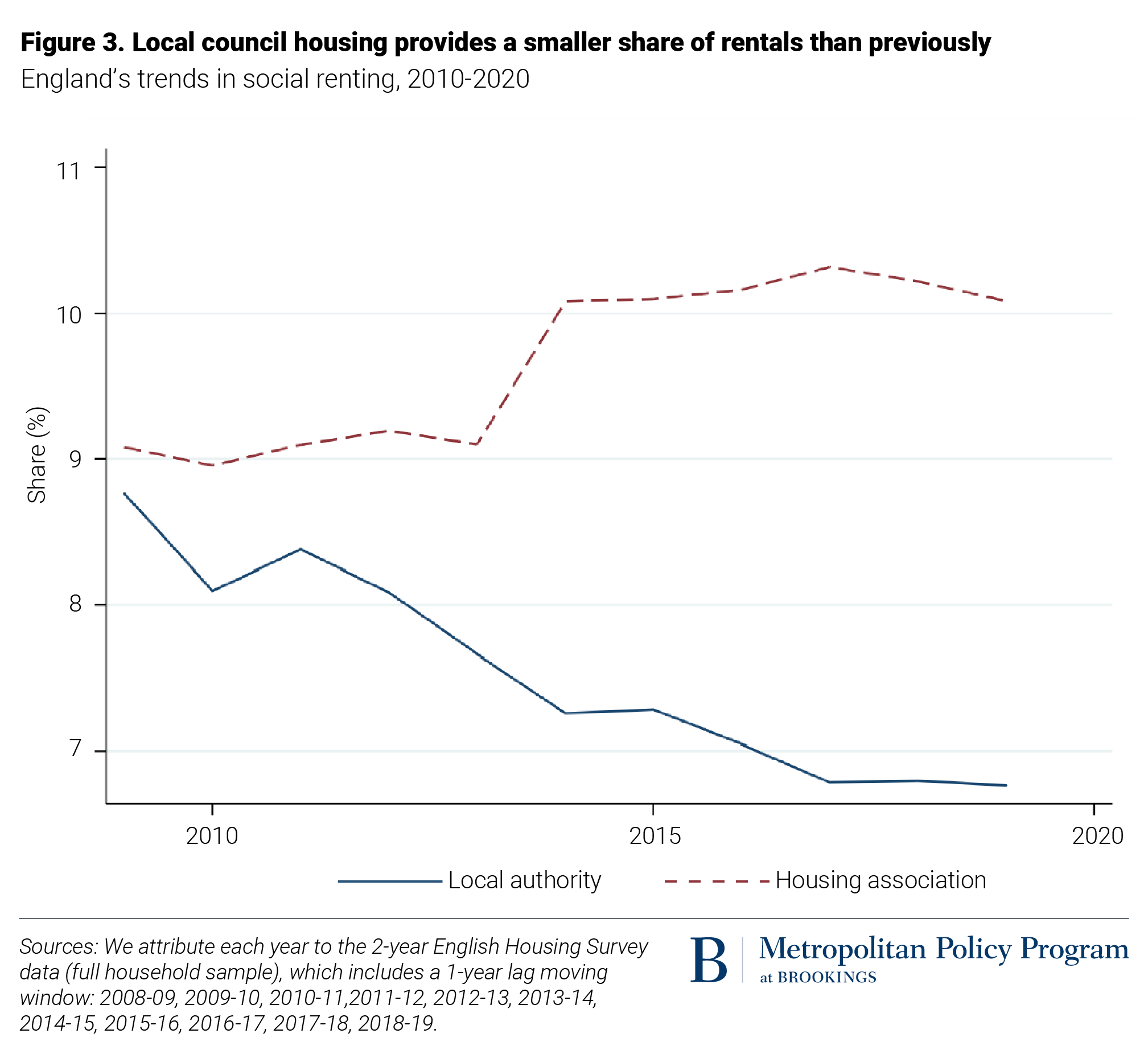

In 2008, housing associations outstripped local councils for the first time in providing the majority of social homes in the U.K. Housing associations are private, nonprofit organizations that provide low-cost housing for households in need of a home. They have been operating an increasing share of social housing properties in the U.K. since the 1970s. Although formally independent of the government, housing associations are regulated by the state and receive public funding. The share of rentals that housing associations provide has remained relatively stable at around 10% over the last decade, whereas the share of council houses has decreased over the same period from nearly 9% to under 7% (Figure 3).

Nowadays, local authorities and housing associations rely on a point (or band) system based on housing needs to allocate social rental properties to households, with each council having its own specific set of rules. Households in critical need of housing—such as the homeless, households living in overcrowded conditions, or those with medical conditions aggravated by their current property—are, in theory at least, more likely to gain access.

One concern with social housing is that because its price is kept significantly below the market price and tenancies are more secure, more households demand social housing than there is supply—leading to significant shortages, long waiting lists, and a corresponding “deadweight loss.” Waiting lists also tend to favor the “clever” and “persistent” among those eligible rather than those most vulnerable, such as those with mental illnesses.

The decline of social housing began in 1980, when Prime Minister Margaret Thatcher introduced the “Right to Buy” policy. In brief, the policy allowed social tenants to purchase their homes at a significantly subsidized price, with the effect that some of the best social housing stock moved from socially rented to privately owned. Right to Buy is a crucial factor in explaining the significant rise in homeownership from 1980 until 2002.

The resurgence of the private rental market

The private rental market has persistently increased its share of the housing stock since the 1990s, displaying a clear upward trend up to around 2017, when it appears to have stabilized (see Figure 1).

The revival of the private rental market has arguably been driven primarily by market forces and innovation. First, the price-to-rent ratio roughly doubled between 1997 and 2018, making owner-occupied housing less and less affordable. Second, the 1996 introduction of “Buy to Let” mortgages—which offer loan terms similar to traditional residential mortgage loans— in conjunction with rising inequality, made it easier for higher-income earners to invest in rental properties.

Policies may also have contributed to the revival and subsequent stabilization of the private rental market. In particular, the persistent decline of the private rental market may have been curbed by the adoption of the 1988 Housing Act, which introduced the Assured Shorthold Tenancy as the default legal residential tenancy in England and Wales. This type of tenancy empowered landlords, making it easier to evict undesirable tenants, thereby reducing the risk of investing and supplying rental units. While the 1988 Housing Act likely had the effect of stimulating the supply of private rental housing, recent policies introduced in 2015 (an additional 3% stamp duty on purchases of Buy to Let properties and the removal of a 10% Wear and Tear Allowance for furnished properties) and 2017 (a reform of how mortgage costs are treated in the income tax system) arguably had the opposite effect. Finally, the stabilization may also have been a consequence of the “Help to Buy” policy, introduced in 2013. The main Help to Buy scheme—Equity Loans—has led to an increase in newly built owner-occupied homes in areas with less binding housing supply constraints. This likely helped counter the persistent increase of the private rental market share at least in those areas.

Key challenges facing rental housing markets

Construction drought

Despite rising real incomes, significant population growth driven by net immigration (at least until the Brexit vote), and strongly growing nominal and real house prices, construction of new permanent dwellings has been decreasing dramatically since the late 1960s, leading to a substantial housing shortfall. According to the Ministry of Housing, Communities and Local Government, the U.K. built nearly 380,000 new homes in 1969, when statistics began. Housing construction subsequently declined to fewer than 200,000 homes from 1990 onward. Residential construction reached a record low in 2012, when fewer than 136,000 new homes were constructed. From 2013, figures started to grow again, partly as a consequence of the economy recovery, reaching about 190,000 new homes in 2017. Housing associations and local authorities built 17% and 1.8% of these new properties, respectively. The continued decline in the importance of council housing is largely due to a lack of adequate public funding.

The COVID-19 pandemic and homelessness

The COVID-19 pandemic has had a dramatic adverse impact on the U.K.’s economy and health system, triggering a flurry of policy interventions that directly targeted or indirectly affected the owner-occupied and renter-occupied housing markets.

The most prominent of these measures has been the introduction of a furlough scheme with the aim to minimize mass layoffs (or worse, corporate insolvencies) and ultimately support the livelihoods of employees and the self-employed. The main effect of this policy on both the owner-occupied and renter-occupied housing markets has been to keep up housing demand; it enabled owners and renters, especially those in vulnerable sectors, to continue paying their mortgages and rents. Perhaps as a consequence of the comparably generous furlough scheme (employees received 80% of their usual income, up to a monthly maximum of 2,500 GBP), the adverse effects of the pandemic on house prices and rents have been largely muted in the short term. The only dramatic short-term effects were on housing transactions, which fell by about 55% from March 2020 until August 2020, and the country’s debt burden.

Most COVID-19-related policy interventions focus on homeowners, in the form of transfer tax and mortgage payment holidays. On the rental side—in addition to the furlough scheme, which may predominately benefit private and social renters, as they tend to be more likely to work in hard-hit sectors such as hospitality, retail, or entertainment—the government implemented a halt on the enforcement of evictions of renters in England until at least the end of May 2021. This is in addition to the government extending the period of notice that a landlord must give to the tenant.

Even before the pandemic hit, the U.K. was facing a significant homelessness problem. To get the homeless into safe shelters and protect them from COVID-19, the British government worked in collaboration with local authorities and charities to devise a plan that involved securing temporary accommodation, and included 6 million GBP of emergency funding by the government to provide relief for frontline homelessness charitable organizations.

Conclusion

The importance of private and social rental housing in Britain has changed dramatically over the last 100 years. Social rental housing has been in decline since 1980, largely as a consequence of the Right to Buy policy and a lack of public funding. While social rental housing has provided affordable and secure housing for those lucky enough to gain access, it has been in chronic undersupply. Moreover, since the mid-1990s, housing has become increasingly unaffordable for the middle classes (which do not qualify for social housing) and the young. As the price of owner-occupied housing has risen even more dramatically than private rents, especially in London and the Southeast of the country, this has led to a recent revival of the private rental market, which is largely unregulated and offers little tenancy security.

Successfully tackling the housing affordability crisis in Britain would require efficiently and effectively helping those most in need (e.g., via housing vouchers or social housing), a reform of the planning and tax system to spur housing construction (which ultimately should lead to lower prices and rents), as well as improving the tenancy security of private renters.

Methodology note: The statistics mentioned in this piece are based on the 2018-19 English Housing Survey (EHS) and on the European Community Household Panel (1994-2001). Unless otherwise noted, the statistics are for England and Wales, as the EHS does not contain information on Scotland and Northern Ireland.

About the Authors