This post was updated on June 27, 2022.

Why are inflation expectations important?

Inflation expectations are simply the rate at which people—consumers, businesses, investors—expect prices to rise in the future. They matter because actual inflation depends, in part, on what we expect it to be. If everyone expects prices to rise, say, 3 percent over the next year, businesses will want to raise prices by (at least) 3 percent, and workers and their unions will want similar-sized raises. All else equal, if inflation expectations rise by one percentage point, actual inflation will tend to rise by one percentage point as well.

Why does the Federal Reserve care about inflation expectations?

The Fed’s mandate is to achieve maximum sustainable employment and price stability. It defines the latter as an annual inflation rate of 2 percent on average. To help achieve that goal, it strives to “anchor” inflation expectations at roughly 2 percent.

Here’s how former Fed Chair Ben Bernanke explained what central bankers call “anchoring,” in an address given in 2022: “[T]the extent to which [inflation expectations] are anchored can change, depending on economic developments and (most important) the current and past conduct of monetary policy. In this context, I use the term ‘anchored’ to mean relatively insensitive to incoming data. So, for example, if the public experiences a spell of inflation higher than their long-run expectation, but their long-run expectation of inflation changes little as a result, then inflation expectations are well anchored. If, on the other hand, the public reacts to a short period of higher-than-expected inflation by marking up their long-run expectation considerably, then expectations are poorly anchored.”

If everyone expects the Fed to achieve an inflation rate of 2 percent, then consumers and businesses are less likely to react when inflation climbs temporarily above that level (say, because of an oil price hike) or falls below it temporarily (say, because of a recession). This makes it easier for the Fed to meet its price stability mandate. In an address given in 2022, Bernanke elaborated on the role inflation expectations play in monetary policy: “The conventional story, which is dominant in central banks around the world, rests on two key premises. First, that inflation expectations… are an important determinant of realized inflation…. The second key premise is that central bank behavior and possibly central bank communications can influence inflation expectations and through them macroeconomic outcomes…. If inflation expectations are well-anchored in the sense that they don’t respond very much to short-term movements in realized inflation and other variables, then policymakers can respond more aggressively to recessionary demand shocks and less aggressively to inflationary supply shocks, leading to better dual mandate outcomes.”

When inflation fell below the Fed’s 2 percent objective in the 2010s, some Fed officials worried that inflation expectations might move below its long-run target; when inflation soared in 2021 and 2022, some Fed officials worried that inflation expectations might move above that long-run target.

Central bankers’ focus on inflation expectations reflects the emphasis that academic economists, beginning in the late 1960s (including Nobel laureates Edmund Phelps and Milton Friedman), put on inflation expectations as key to the relationship that ties inflation to unemployment. As a result of the persistently high inflation in the 1970s and 1980s, inflation expectations became unanchored and rose with actual inflation—a phenomenon known at the time as a wage-price spiral. This cycle plays out as follows: high inflation drives up inflation expectations, causing workers to demand wage increases to make up for the expected loss of purchasing power. When workers win wage increases, businesses raise their prices to accommodate the increase in wage costs, driving up inflation. The wage-price spiral means that when inflation expectations rise, it is difficult to bring down inflation, even if unemployment is high.

How are inflation expectations measured?

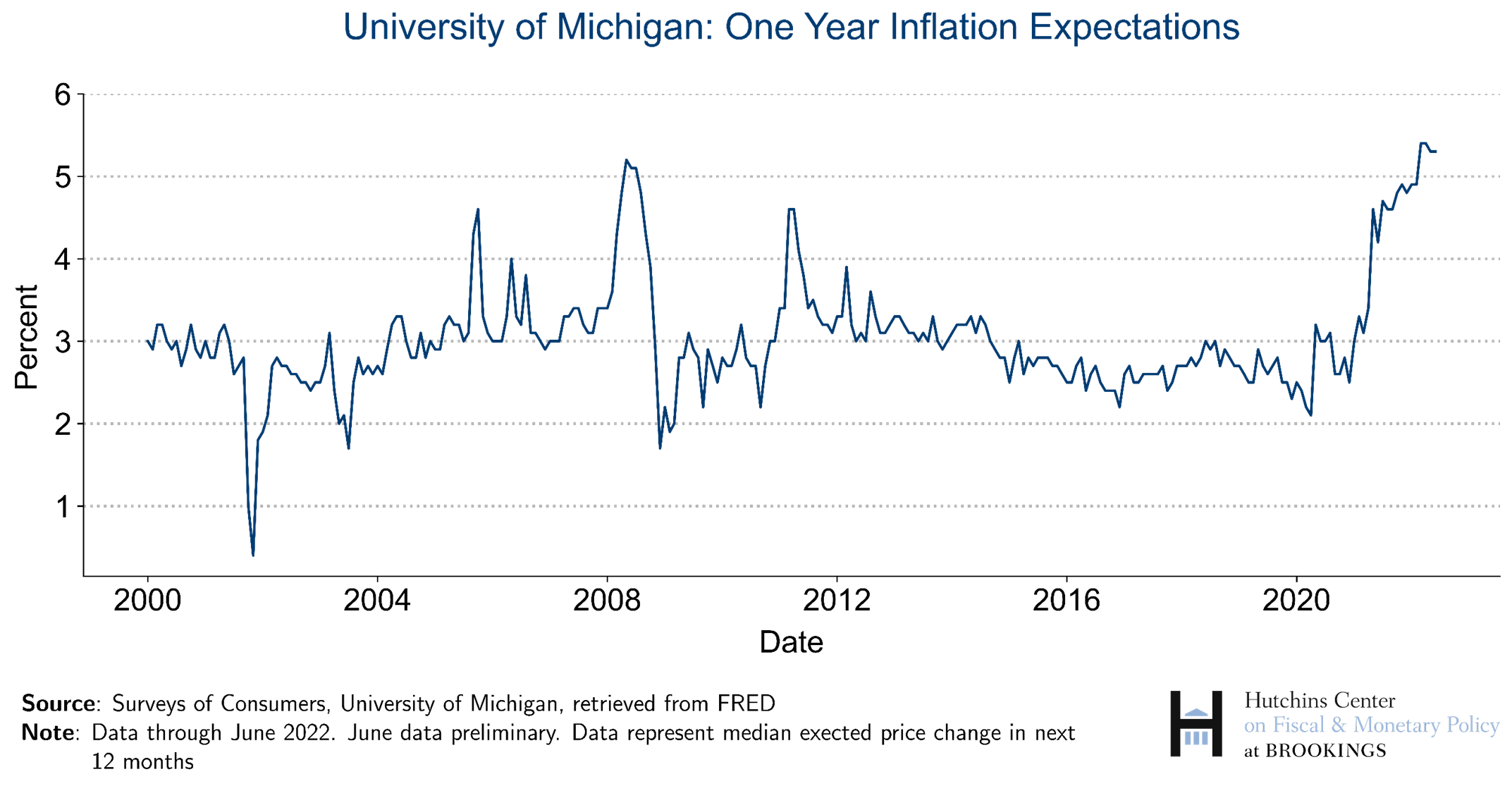

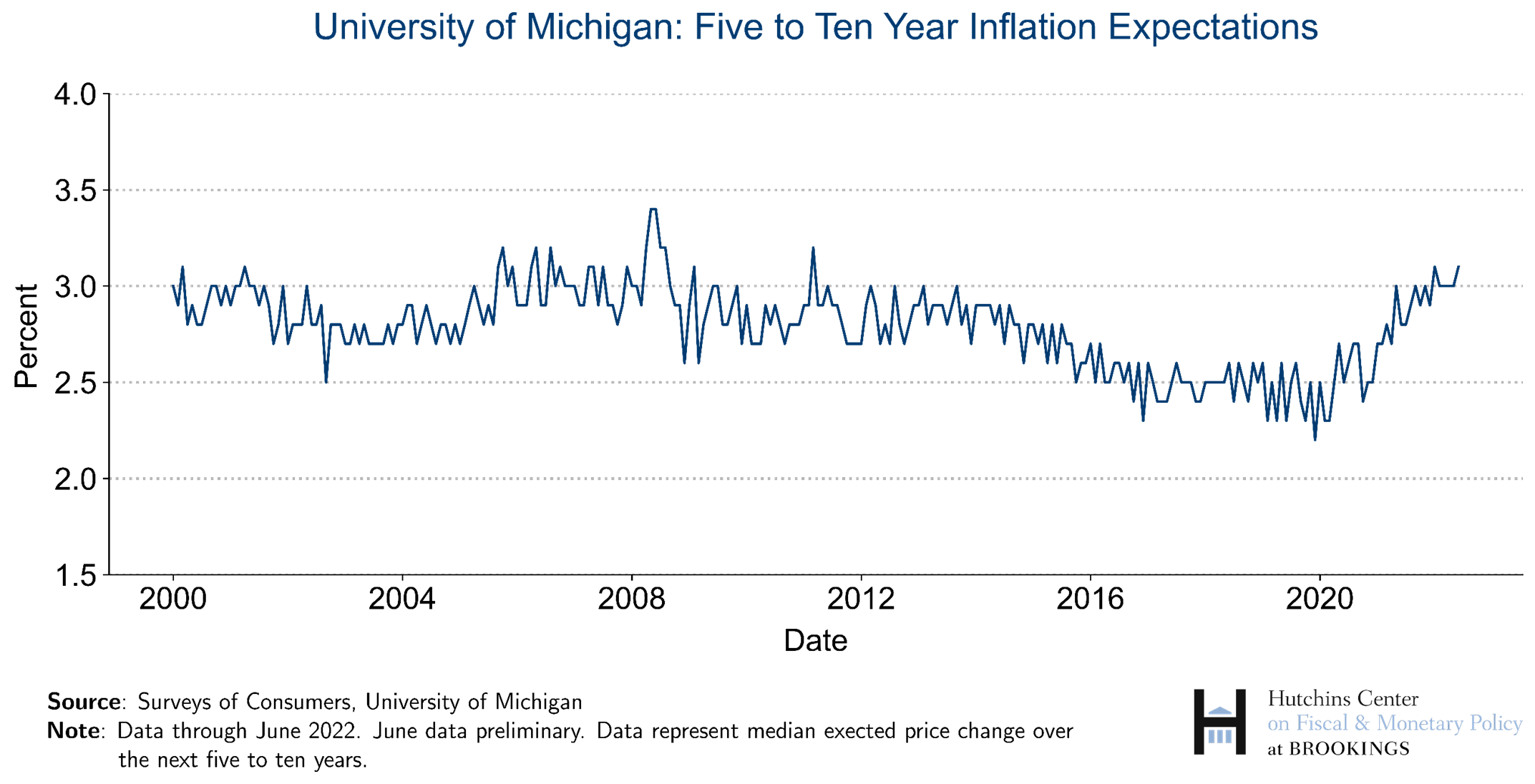

There are three primary ways to track inflation expectations: surveys of consumers and businesses, economists’ forecasts, and inflation-related financial instruments. The University of Michigan’s Survey Research Center, for instance, asks a sample of households (about 600 each month) how much they expect prices to change over the next year as well as five to ten years into the future. The Federal Reserve Bank of New York and the Conference Board field similar surveys.

For much of the first couple decades of the 21st century, the University of Michigan’s surveys found one year inflation expectations hovering at about 3.0 percent, while expectations for the five to ten years were around 2.8 percent. However, that changed as pace of inflation quickened in 2022. Final data for June 2022 showed one year inflation expectations at 5.3 percent and five to ten year expectations at 3.1 percent.

Historically, respondents to the University of Michigan’s surveys of consumers expect higher levels of inflation than actually occur. For this reason, analysts focus on the trend in these surveys—whether consumers expect the pace of inflation to be rising, falling, or remaining stable—rather than the level of expected inflation

The Survey of Professional Forecasters (SPF) asks professional economic forecasters about their outlook for two major government measures of inflation, the consumer price index (CPI) and the personal consumption expenditures (PCE) price index (which is the Federal Reserve’s preferred measure).

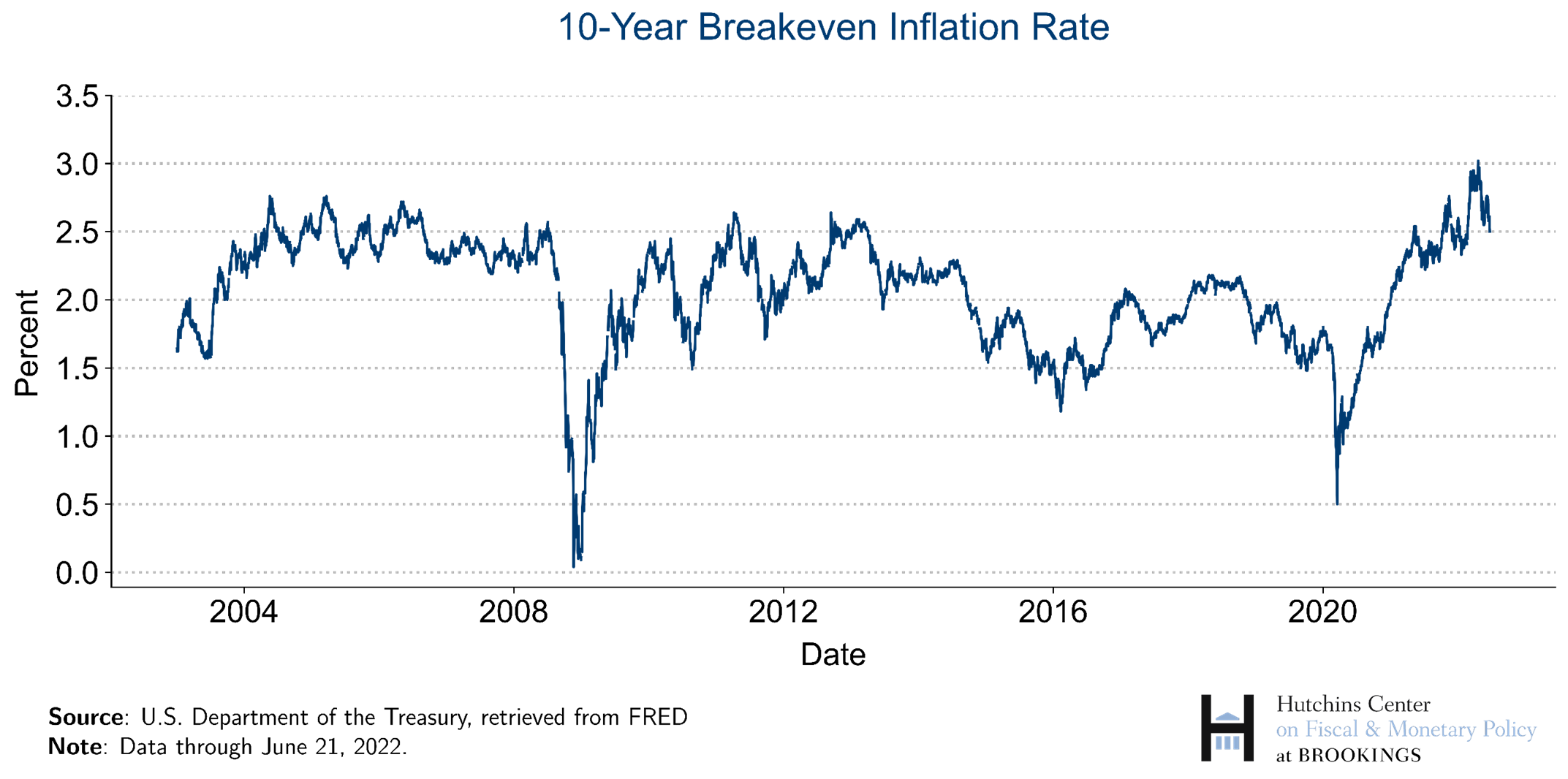

One widely used gauge of market-based inflation expectations is known as the 10-year breakeven inflation rate. The breakeven rate is calculated by comparing 10-year nominal Treasury yields with yields on 10-year Treasury Inflation Protection Securities (TIPS), whose yield is tied to changes in the CPI. The difference between the two approximates the market’s inflation expectations because it shows the inflation rate at which investors would earn the same real return on the two types of securities. If investors expect higher inflation, they will buy 10-year TIPS instead of nominal Treasuries, driving down yields on TIPS and driving up the breakeven rate. A similar measure, also derived from Treasury spreads, is an estimate of inflation expectations for the five years that begin five years from the present, known as the 5-Year, 5-Year Forward Inflation Expectation Rate. Like the breakeven rate, it is calculated by comparing TIPS yields with nominal Treasury yields. These market-based indicators are, however, imperfect measures of inflation expectations, as they combine true expectations for inflation with a risk premium—compensation that investors require to hold securities with value that is susceptible to the uncertainty of future inflation.

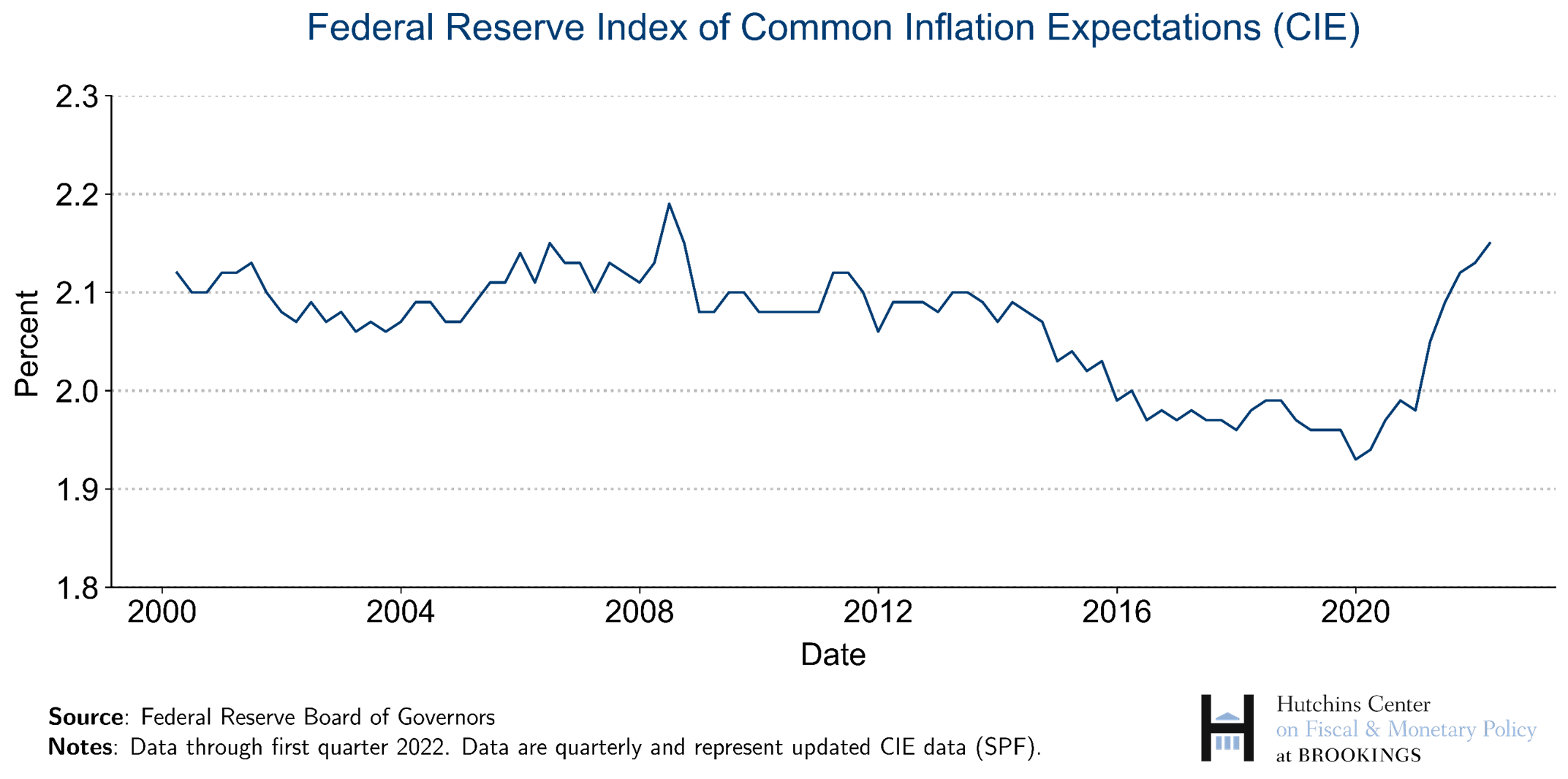

Federal Reserve economists maintain an index that combines 21 measures of inflation expectations, the Index of Common Inflation Expectations (CIE). That index was below 2 percent for much of the late 2020s, but began creeping up at the beginning of 2022.

How can the Fed influence inflation expectations?

One way is to use its monetary policy tools – particularly short-term interest rates – to achieve and maintain inflation around 2 percent. However, the Fed can also influence expectations with its communications, particularly by elaborating on the likely future course of monetary policy. This strategy is known as forward guidance, and it has over time become an important tool in the Fed’s toolbox.

In August 2020, after years of inflation running below the 2 percent target, the Fed modified its monetary policy framework to influence both actual inflation and inflation expectations. The decision left its 2 percent inflation target intact. However, the new framework stipulated that periods of below-2 percent inflation would be offset with periods of above-2 percent inflation, an approach it is calling Flexible Average Inflation Targeting (FAIT). In its old framework, if inflation fell below the 2 percent target, the Fed pledged to try to get it back to target without compensating for the period of inflation shortfall. The change makes explicit that, following a period in which inflation has fallen short of target for a time, the Fed will accept and even encourage periods of above-2 percent inflation going forward, discouraging a decline in inflation expectations. However, if inflation overshoots the 2 percent target, the Fed will not seek future undershoots of the target. In other words, the Fed will not encourage inflation below 2 percent to offset this current bout of inflation.

Why does the Fed worry about inflation expectations falling too low?

When inflation expectations are anchored at target, it is easier for the Fed to steer inflation to 2 percent. If inflation expectations move down from 2 percent, inflation could fall as well—a reverse wage-price spiral. In the extreme, this process can increase the risk of deflation, a damaging economic condition in which prices fall over time rather than rise.

Another reason that the Fed worries about low inflation expectations is that they are closely related to interest rates. When setting prices on loans, lenders and investors account for the expected rate of inflation over the life of the loan. Nominal interest rates are the sum of the real interest rate that will be earned by lenders and the expected rate of inflation. When nominal interest rates are very low, the Fed has less room to cut interest rates to fight a recession. By keeping inflation expectations from dipping too low, the Fed protects its ability to stimulate the economy during downturns.

Fed Chair Jerome Powell discussed this while announcing the new framework: “Inflation that runs below its desired level can lead to an unwelcome fall in longer-term inflation expectations, which, in turn, can pull actual inflation even lower, resulting in an adverse cycle of ever-lower inflation and inflation expectation. This dynamic is a problem because expected inflation feeds directly into the general level of interest rates. Well-anchored inflation expectations are critical for giving the Fed the latitude to support employment when necessary without destabilizing inflation. But if inflation expectations fall below our 2 percent objective, interest rates would decline in tandem. In turn, we would have less scope to cut interest rates to boost employment during an economic downturn, further diminishing our capacity to stabilize the economy through cutting interest rates. We have seen this adverse dynamic play out in other major economies around the world and have learned that once it sets in, it can be very difficult to overcome. We want to do what we can to prevent such a dynamic from happening here.”

What role did inflation expectations play in the Fed’s June 2022 decision to lift short-term interest rates by an unusually large three-quarters of a percentage point?

In response to a historically high inflation rate and a strong labor market, the Fed began raising interest rates in early 2022. At its June 2022 meeting, the Fed raised its target for the federal funds rate by 0.75 percentage points to a target range of 1.5 to 1.75 percent, its largest single-meeting rate hike since 1994.

In his post-meeting press conference, Powell highlighted the role of inflation expectations in the Fed’s deliberations. “One of the factors in our deciding to move ahead with 75 basis points today was what we saw in inflation expectations,” he said. “Some indicators of inflation expectations have risen, and projections for inflation this year have been revised up notably. In response to these developments, the committee decided that a larger increase in the target range was warranted at today’s meeting.” (A few days before he spoke, the University of Michigan’s preliminary reading on five to ten year inflation expectations for June had moved up to 3.3 percent, a bit higher than the 2.9 to 3.1 percent range in which it had been. The final reading, based on more interviews, came in at 3.1 percent.)

“[O]ur approach of expeditiously moving our policy rate up to more normal levels…will help ensure that longer-term inflation expectations remain well anchored at 2%,” Powell said.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Related Content

2020

Authors

Commentary

What are inflation expectations? Why do they matter?

November 30, 2020