Studies in this week’s Hutchins Roundup find that college tuition hikes do not affect higher educational attainment but decrease homeownership, diminished competition among U.S. firms partly explains soft business investment, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Tuition hikes increase debt but have no affect on higher education attainment

Tuition and fees at public colleges in the US rose by 81 percent ($3,843) between 2001 and 2009. Zachary Bleemer and coauthors at the New York Fed find that these tuition hikes had little effect on educational attainment, but did lead students to borrow more. In particular, they find that tuition increases accounted for about one third ($1,628) of the rise in average student debt among 24-year-olds over this period. They also find that the tuition hikes explain up to one third of the eight percentage-point decline in homeownership for 28-to 30-year-olds over 2007-15. The authors conclude that states that increase college costs can expect to see weaker spending and wealth accumulation among young consumers in future years.

Declining U.S. firm competition partially explains low investment

German Gutierrez and Thomas Philippon from NYU argue that declining competition among firms partially explains low U.S. corporate investment since the early 2000s. For example, although industries most affected by Chinese competition saw a decline in the number of US firms, leaders of those industries increased investment the most, suggesting a causal relationship between competition and investment. They argue that the decline in competition may be explained by increases in regulation that benefit large firms and lead to increased rent-seeking.

Potential GDP may not have fallen as much as mainstream forecasters suggest

Olivier Coibion from the University of Texas and Yuriy Gorodnichenko and Mauricio Ulate from the University of Califonia, Berkeley, find that estimates of potential GDP from leading macroeconomic forecasters—the CBO, the Fed, the IMF, and the OECD—overreact to cyclical changes that do not have long run effects on output (such as monetary policy and government spending) and underreact to structural changes (such as productivity growth) that do. Using an alternate method not subject to these shortcomings, the authors find a smaller decline in potential output since the global financial crisis than these agencies do. They argue that that current U.S. output remains almost 10 percentage points below potential output, suggesting that there is room for policymakers to use demand-side policies to boost economic activity.

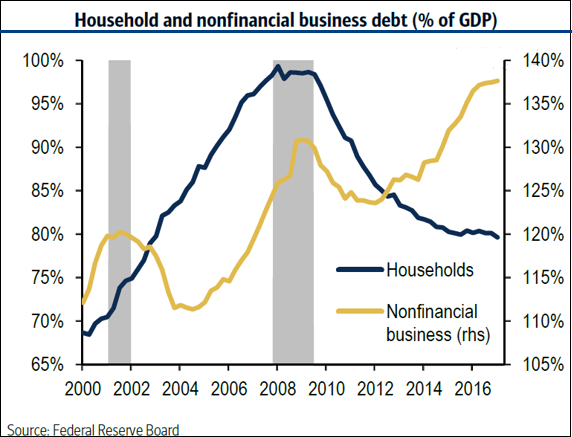

Chart of the week: U.S. household debt loads fall while business borrowing increases

Quote of the Week:

“In my view, the neutral level of the federal funds rate is likely to remain close to zero in real terms over the medium term. If that is the case, we would not have much more additional work to do on moving to a neutral stance. I will want to monitor inflation developments carefully, and to move cautiously on further increases in the federal funds rate, so as to help guide inflation back up around our symmetric target,” says Federal Reserve Governor Lael Brainard.

“In recent days, we have begun to hear acknowledgement from other major central banks that they too are seeing conditions that suggest policy normalization could be on the table before too long…[T]he pace and timing of how central banks around the world proceed with normalization, and the importance of balance sheet policy relative to changes in short term rates in these normalization plans, could have important implications for exchange rates and financial conditions globally.”

Related Content

Related Books

Authors

Commentary

Hutchins Roundup: College tuition hikes, firm competition, and more

July 20, 2017