Bergstresser and Luby will discuss their findings in the opening session of the 2017 Municipal Finance Conference. Tune in here Monday, July 17, 2017, at 1:30 PM EDT to watch.

Beside the obvious and immediate damage it inflicted on asset values, the financial crisis of 2007-2009 reshaped the structure, functioning, and regulation of American securities markets. A forthcoming new paper from Daniel Bergstresser and Martin Luby takes a close look at how the market for municipal bonds has changed in recent years. Bergstresser and Luby will present the results of their findings at the opening panel of the 2017 Municipal Finance Conference, co-hosted by the Hutchins Center on Fiscal and Monetary Policy at Brookings, the Rosenberg Institute of Global Finance at Brandeis International Business School, the Olin Business School at Washington University in St. Louis, and the University of Chicago Harris School of Public Policy.

In the paper, which will be published as a Hutchins Center Working Paper, Bergstresser and Luby highlight the changes in the municipal market related to primary market issuance and secondary market trading trends, bond ownership composition, bond structures, products and processes, and market participants. They also offer a discussion of future developments that are likely to impact the municipal securities market in the future. Here are some key factors they discuss.

State and local governments are less reliant on municipal bonds than they were before the financial crisis.

State and local governments issued $470 billion of municipal bonds in 2016, about 2 percent less, in nominal dollars, than in 2005. New bond issuance (as opposed to issuance that restructures or refinances existing debt), fell even more, about 25%, between 2005 and 2016. This decline in new issuance is far larger than the decline in state and local capital spending over this period, suggesting that municipal bonds are now increasingly complemented by other funding and financing sources for infrastructure. Understanding these other sources will be an area of concern for bond market participants.

Still, new bond structures have proven to be important financing tools.

While some bond products and structures have declined in use after the financial crisis (e.g., bond insurance, floating rate debt), developments have emerged and proved to be an important source of financing. For example, as part of the American Recovery and Reinvestment Act of 2009, the Build America Bond program (BAB) created bonds that were taxable (unlike most muni bonds), but provided issuers a federal subsidy equal to 35% of the interest costs. Those subsidies made BABs popular among state and local governments and among bond-buyers in the market for taxable securities. Bergstresser and Luby argue the program drove a spike in bond sales just after its enactment. By the end of 2010, BABs represented more than 37 percent of total long-term municipal bond issuance. However, after the bond issuance program expired in December of 2010, the share of bond sales that were taxable fell back to roughly their pre-crisis levels.

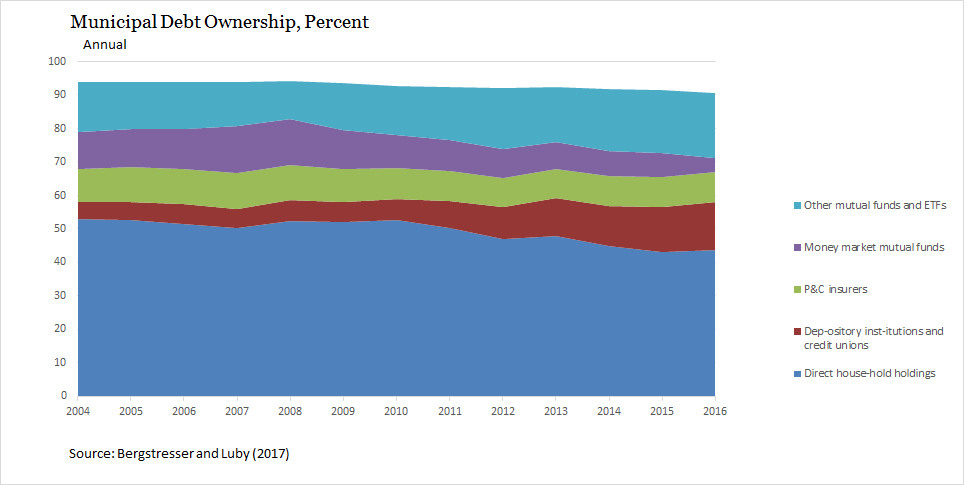

Banks are holding a larger share of municipal bonds than before the crisis, and household ownership has been increasingly concentrated among the very wealthy.

The share of bonds held by depository institutions rose from 5 percent in 2005 to almost 15 percent in 2016. Over that same period, household ownership fell by a similar amount, from 53 percent to 44 percent. For the most part, that decline resulted in the concentration of bond ownership among very wealthy households. Although ownership rates have fallen among all households since 2007, the steepest declines took place among those in the 75th to 90th percentile of asset ownership. Meanwhile, those in the 90th percentile have claimed a larger share of total muni bond ownership among households.

Underpricing increased significantly during the financial crisis

Underpricing—the spread between the issuance price and the price at which eventual buyers purchase the bond in the first 30 days after issuance—represents an additional cost of issuance for the issuer. Underpricing increased significantly during the financial crisis but has dropped considerably since although not yet returning to pre-financial crisis levels. Bergstresser and Luby also explore the relationships between bond amount, underwriter size, bond sale method, issuance costs and financial advisor size and the degree of primary market underpricing. The number of interdealer trades between issuance and sale to final customer within first 30 days increased significantly and was also associated with the level of underpricing.

Trading trends and costs in the secondary market changed significantly over the last two decades.

While large trades remain significantly cheaper than smaller trades in the secondary market, the spread declined significantly between sized trades over the last 15 years. Smaller trades have become much less expensive while larger trades actually increased modestly during and after the financial crisis. Electronic trading and greater price transparency has likely aided in this narrowing of the costs between retail and institutional trades. Another interesting change in the municipal secondary market since the financial crisis is the increasing prevalence of interdealer trades. The average number of interdealer trades between bond placement with customers was .53 in the pre-financial crisis period and 1.15 in the post crisis period.

President Trump’s policy choices could have direct impact on municipal bond holders and states.

Bergstresser and Luby argue that proposed tax reforms from the Trump administration would dampen demand for municipal securities in two ways. First, reducing the corporate tax rate would make tax-exempt municipal bonds relatively less attractive to corporations, and fewer firms would choose to invest in them. Meanwhile, other parts of the tax proposals (in particular, the ending of the deductibility of state and local taxes) could lead to a deterioration in the credit ratings of state and local governments.

On the other hand, President Trump has proposed an infrastructure rebuilding initiative that could expand state and local governments’ access to financing. Whether that plan would involve a revival of the Build America Bond program, new direct subsidy bonds, or tax credits is unclear so far.

Authors

Commentary

Key changes in the municipal bond market since 2007

July 14, 2017