A few years ago, least-cost electrification models began pointing to an exciting possibility: solar and solar-diesel hybrid mini-grids could be the cheapest way to deliver reliable, on-demand electricity for hundreds of millions of people without power. This was especially promising for sub-Saharan Africa, where the insolvency and dysfunction of national utility companies had led to slow progress in electrifying rural populations. Governments and donors formed partnerships to support an array of new mini-grid programs. It’s time to begin the learning about regulatory development and financing structures required to ramp up this delivery platform.

Most mini-grid incentive programs in Africa are still in their early years, so it’s premature to draw final conclusions about their efficacy. That said, we thought it would be fruitful to take stock of where things stand. We studied 20 mini-grid programs in sub-Saharan Africa, 17 of which are currently being implemented. The findings of the full report are summarized below. The graphics include only those programs where data was available.

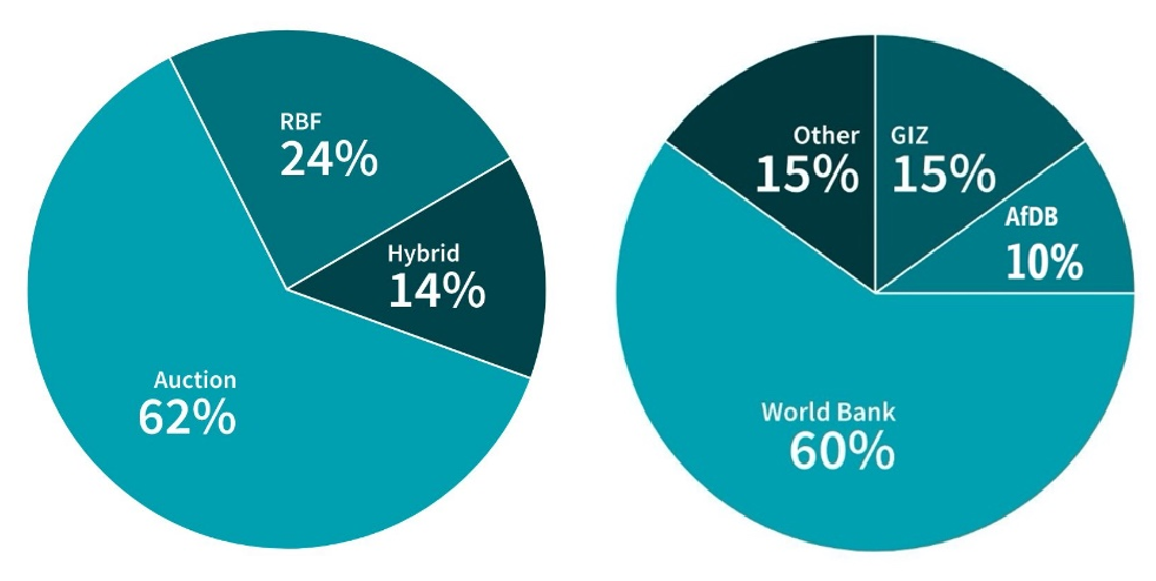

Figure 1. Incentive models and primary financing sources

Note: RBF is results-based financing.

Results-based financing shows considerable promise

Auctions are great for scale, but they’re being used to build pilots and force regulatory development. RBFs and hybrid programs offer a promising alternative.

In the grid-scale solar and wind markets, generous incentives, generally in the form of feed-in-tariffs and tax credits, encouraged large-scale development of renewable energy projects. These first-generation public support programs were the initial sources of demand for the scale up of OEM capacity and drove component prices down 70-90 percent. Once these scale-driven cost declines made renewables grid-competitive, the sector shifted from direct incentives to competitive procurement, typically through public auctions and tenders, which in stable markets are nearly always competitive and oversubscribed.

But top-down competitive auctions are designed for markets that are mature enough to benefit from competition. There is a direct relationship between the availability of competitive supply in the market and the benefits of competitive procurement. In the African mini-grid market, there simply are not enough experienced developers.

And yet, 62 percent of the mini-grid programs analyzed rely on auction mechanisms to allocate risks and opportunities between the developers, off-takers, and regulators. Program implementation documents for mini-grid scale-up programs describe programs as “pilots” or “demonstrations” and markets as “nascent” and “immature,” even while aiming to increase the number of installed systems by a factor of four or more. Often these programs are implemented without regulatory frameworks in place. Instead, the pilots are accompanied by large technical assistance packages.

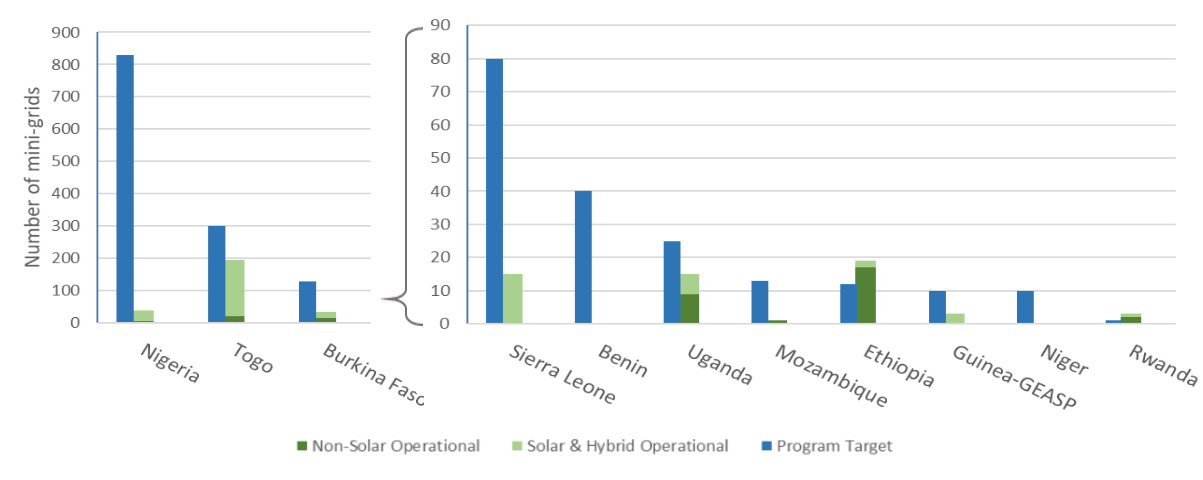

Figure 2. Mini-grid program targets

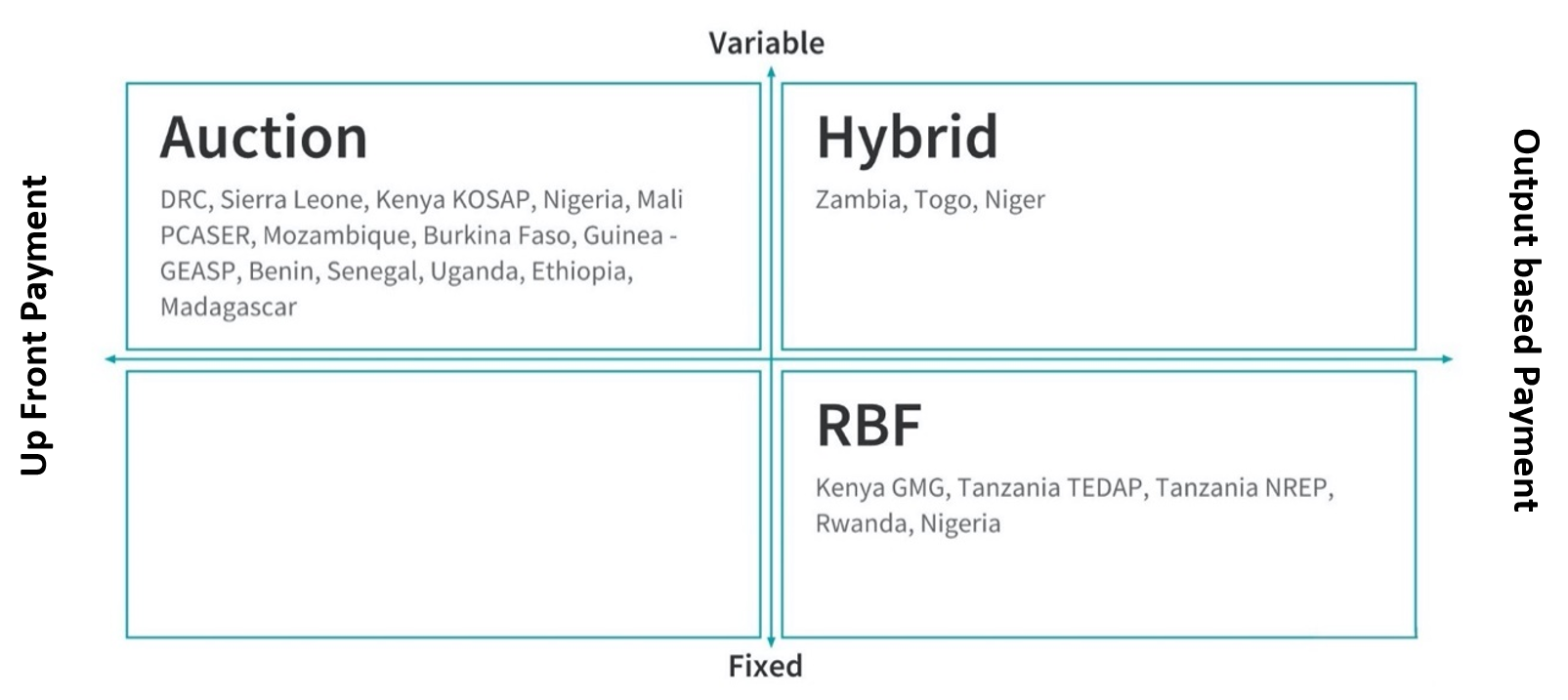

Even after the mini-grid market matures, it may need both competition and subsidy. Mini-grids still represent rural infrastructure, delivering social benefits that do not show up in the internal rates of return needed for purely commercial projects. This is the same reality faced by grid extension programs, which commonly require investments of $1,500 per connection or more, but which frequently enjoy connection subsidies covering 70-100 percent of those costs. Results-based financing (RBF) and hybrid programs like the Beyond the Grid Fund Africa and Universal Energy Facility offer a promising path to coupling competition with subsidy. These and other new programs are using a variety of hybrid models that incorporate key auction elements like competition with RBF elements like output-based payments (Figure 3).

Figure 3. Mini-grid support programs, categorized by payment approach

Given the early stage of nearly every mini-grid market in Africa, it is likely that the sector would benefit less from competition than from clear subsidies, bankable regulation, and capacity building. This would support a scale-up phase in the market, which could bring new market entrants, drive costs down, and build the capacity of regulators to allocate market opportunity efficiently.

The lack of transparency is inhibiting innovation

We have a good understanding of mini-grid costs and subsidy requirements, but a lack of transparency in programs is inhibiting learning and delaying candid conversations regarding tariffs.

While mini-grids are not new, “third-generation” systems designed for grid interconnection and utilizing solar photovoltaics, battery storage, smart metering, and remote monitoring systems represent an underfunded segment with few competitive market participants and challenging unit economics. So it is worth noting that while mini-grid costs have ranged widely, a review of program documents reveals relative consistency in assumptions around mini-grid capital expenditures ($4,400-$6,200/kW). Stated subsidy levels across programs were remarkably consistent as well, with RBF payments of $350-$500/connection and auctions providing 60-80 percent of upfront capital expenditures. This reflects a narrowing range of expectations regarding the viability gap facing mini-grids.

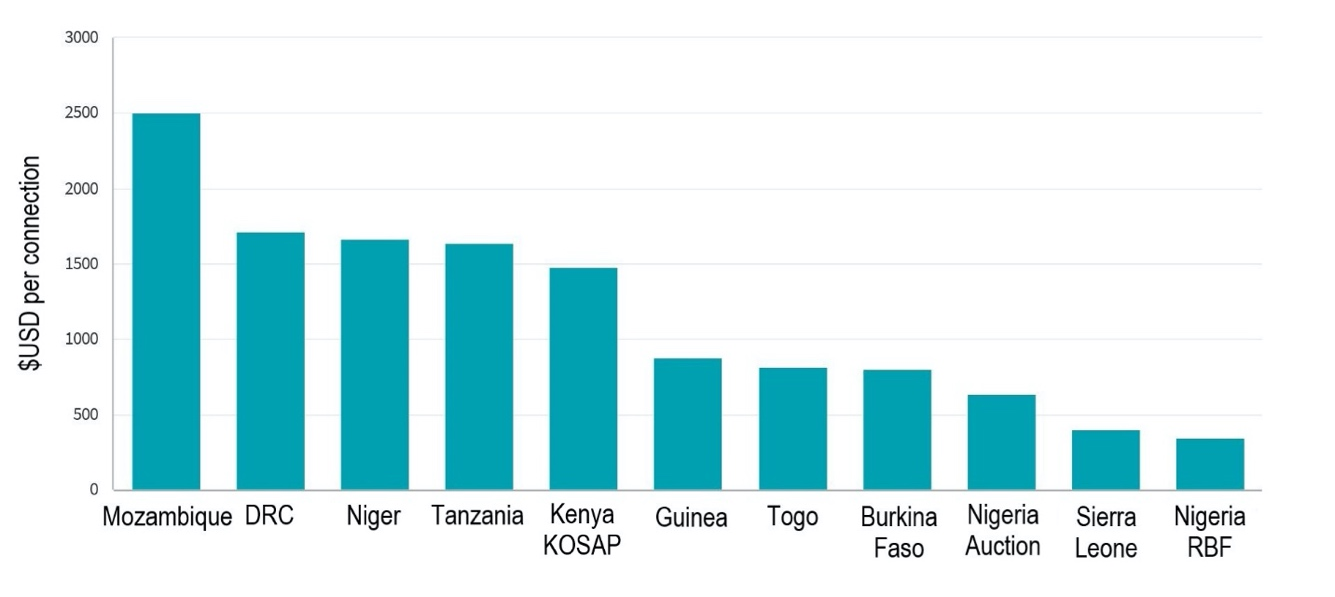

However, due to a lack of transparency in program budgets, it is unclear whether technical assistance, capital expenditure subsidies, or other cost components are driving overall program costs, which we found to vary widely. For example, the average cost per connection—an important metric for comparing costs of different power delivery options and benchmarking mini-grid programs—across analyzed programs ranged from $348 to $2,500/connection.

Figure 4. Program cost/connection (US dollars)

This lack of transparency may have troubling consequences when it comes to tariff setting. Even as mini-grids reach cost parity with the grid—which they already have in some countries—the tariffs needed to fully recover costs of a mini-grid will typically be much higher than the retail tariffs charged by the utility because of the deep subsidies enjoyed by the latter. Different forms of grid subsidies allow African utilities to charge tariffs that have been, on average, 41 percent below their levelized cost of generating power.

Transparency in program costs may prove to be an important lever in driving the tough longer-term conversations within governments regarding subsidy allocation across the sector. Otherwise, the least-cost advantage that mini-grids may enjoy will mean nothing to those that matter most: the rural customers they’re intended to serve.

Expectations of many programs are unrealistic

Countries want their mini-grids to be built by local companies, deliver for last-mile communities, support productive use, and—ultimately—be commercially viable. From where the sector currently stands, that is a tall order.

There may be a pathway to commercially viable mini-grids in Africa that require no subsidy. The World Bank has mapped out how cost declines from technology development and scale, combined with increasing income-generating uses of electricity—like irrigation, agriculture milling, or other commercial uses—could boost load factors of mini-grid systems to 40 percent and drive down costs to $0.22/kwh by 2030. This would be cheaper than 23 of 39 utilities in Africa.

Programs aiming to nudge mini-grids to commercial viability must focus on identifying sites that can support higher load factors, work in tandem with programs targeting increased productivity at sites, and attract experienced developers who can procure equipment at global spot prices and deliver projects at lowest cost. However, there is a huge swath of communities where load factors are unlikely to increase, where incomes and commercial opportunities are too limited to yield much from demand stimulation efforts, and where local companies may deliver potential cost savings over international suppliers. Mini-grids could still be attractive, and a potentially least-cost solution for many communities.

In these circumstances, governments and donors must take a wider view and prioritize their objectives. Where the objective is maximizing high-quality rural access, cost is still an important factor, but a recognition of the need for subsidy will be essential, at least in the near to medium term, to delivering affordable power to rural populations. Countries aiming to maximize high-quality rural access with mini-grids rather than hitting cost targets could benefit from programs that prioritize capacity building and technical assistance, offer upfront payments or other measures that expand access to capital for local firms, include more generous subsidies to support development at sites facing thin commercial demand and lower load factors, and offer opportunities to negotiate terms post-auction. Emphasizing these measures over a narrower focus on prices and competition might help establish a domestic industry capable of delivering mini-grids at scale.

Africa’s many emerging mini-grid programs have admirably big ambitions, but some may be seeking to leverage auctions as a scale-up mechanism without the underlying market fundamentals needed for auctions. The core question facing these and future programs is whether the objective is commercially viable, unsubsidized mini-grids or maximizing high-quality rural access. Programs designed to simultaneously achieve both will have a tough time achieving either.

Related Content

Authors

Commentary

Lessons from the proliferating mini-grid incentive programs in Africa

December 11, 2020