In a previous post, we identified three sources of concern about Africa’s debt. The question is what can be done to prevent these troubling factors from turning into a full-blown debt crisis. As elaborated in our paper, we suggest three possible remedies that range from the medium- to the long-term.

Countercyclical fiscal policies

The recent rise in African debt levels, with 15 countries at risk of debt distress, was clearly associated with the fall in commodity prices starting in 2014; Africa’s terms of trade fell by 20 percent between 2014 and 2015. The fall in commodity prices followed a period of rising commodity prices that started in the early 2000s. Most countries seem to have treated this rise in commodity prices as permanent.

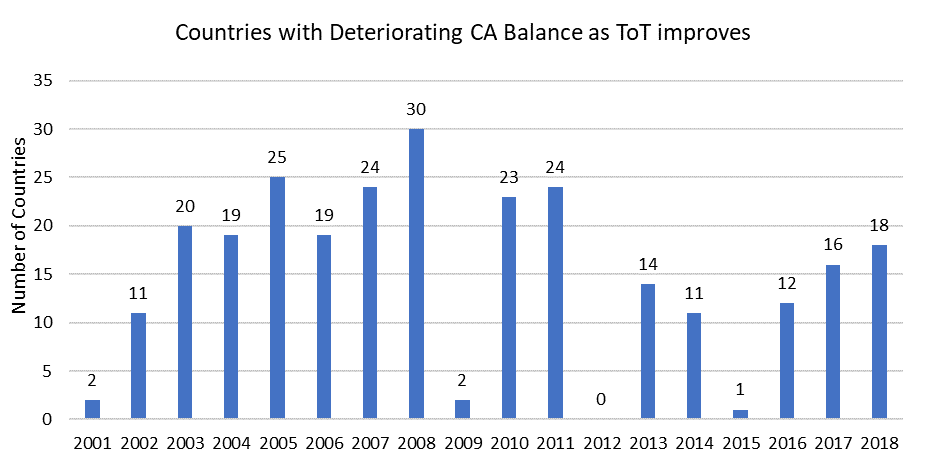

How do we know this? As shown in a simple framework, if a rise in commodity prices is temporary, it is optimal for a country to save part of the windfall revenues for the future. This is then reflected in a reduction in the current account deficit (or an increase in the surplus). Most African countries, however, saw their current accounts deteriorate during the favorable terms of trade shocks of the 2000s (Figure 1). By not saving part of the windfall in the early 2000s, they were ill-prepared to withstand the negative shock of falling commodity prices after 2014, resulting in a sharp rise in their debt levels.

Figure 1: Terms of trade and current account balances in Africa

Source: Authors’ calculations, using IMF data.

To be sure, these countries may have found countercyclical fiscal policies politically difficult to implement. Their infrastructure and other needs are huge. An IMF mission chief once suggested to a senior African government official that he save some of the additional revenues “for a rainy day.” The policymaker responded, “But it’s raining today.”

Borrowing for infrastructure in weak governance settings

Africa has the worst energy and transport infrastructure in the world. Some 600 million Africans live without electricity. Road density has been declining over the last 20 years. But there are many weak links in the chain between borrowing for infrastructure and improved infrastructure services. There is at best a weak correlation between public investment and improvements in infrastructure quality (Figure 2). Why? Public spending is managed poorly, and the binding constraint on infrastructure improvements is not finance.

Figure 2: The binding constraint on infrastructure is not always money

Source: IMF (2015). Making Public Investment More Efficient.

Developing countries in general, and some African countries in particular, fare poorly in the allocation of public resources to investment projects; in the use of funds for their intended purposes; and in getting value for money spent. A recent analysis of the public-sector efficiency frontier for many countries shows almost every African country is far inside the frontier.

Reducing Africa’s infrastructure deficit will require policy and institutional reforms alongside better finance. These will reduce financing needs; conversely, lack of reform increases them. Rozenberg and Fay (2019) show that the money needed to meet infrastructure services in a sustainable way drops from 8.2 percent of GDP to 4.5 percent with policy- and regulation-induced efficiency.

The implication for the debt strategy is that short-term borrowing to finance long-term investment can be dangerous. The foreign-exchange earnings from infrastructure investments may take a long time to be realized, particularly if they require policy and institutional reforms before the investments bear fruit. If the creditors require repayments in the short term, the country may find itself in a liquidity crisis, some of which have been known to trigger a debt crisis.

Taxation and the marginal cost of funds

As an alternative to borrowing, several people have suggested that African countries finance their infrastructure needs by raising domestic taxes. The tax revenue-to-GDP ratios in Africa are low.

But there are problems in inferring that African countries should therefore raise their tax-to-GDP ratios. Almost all taxes are distortions and impose costs on the economy. In the simplest formulation of the problem, a tax reduces both the consumer and producer surplus by more than the tax revenue generated. In terms of the pretax economy, there is a fall in total welfare known as the deadweight loss. This is the cost to the economy of raising tax revenues.

The question is whether this cost is significant relative to the revenue raised. The answer is often expressed in terms of the marginal cost of funds (MCF), which is the revenue raised plus the deadweight loss as a share of the revenue raised. In other words, how much does it cost the economy to raise a dollar of tax revenue? The magnitudes are an empirical matter, not a theoretical one.

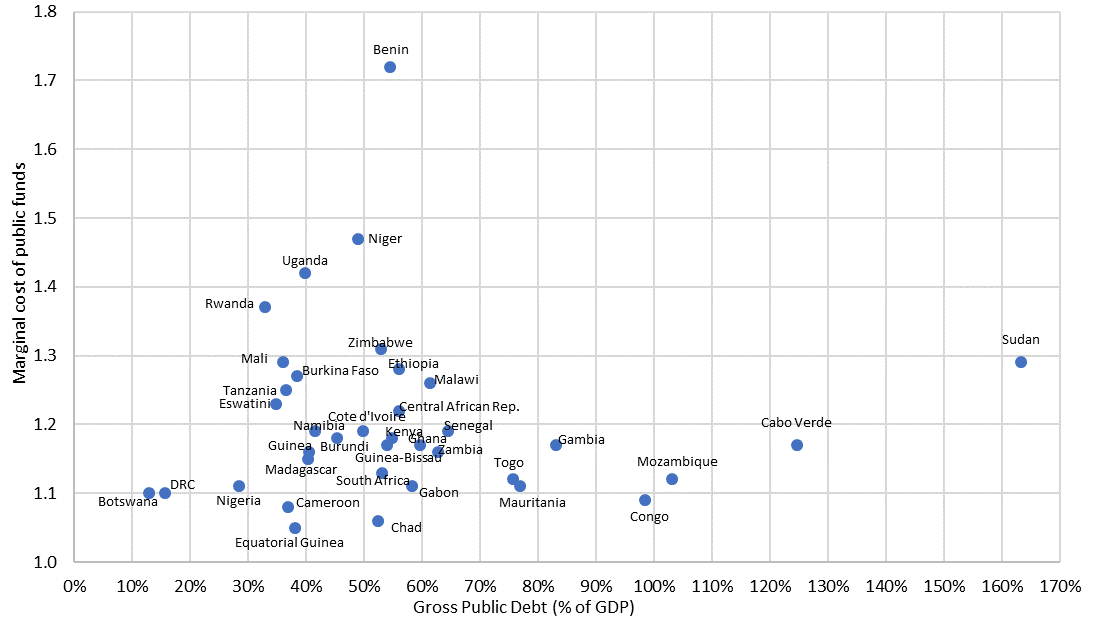

Figure 3: Marginal cost of public funds and gross public debt, Africa Region

Source: Authors’ calculations, using data from the IMF and Auriol and Warlters (2012).

Auriol and Warlters have calculated the MCF for 38 African countries. They find that the average MCF across five different tax handles is 1.2. However, there is a variation around that mean, with some countries—including some highly indebted ones—having MCFs of 1.4 or higher. While there does not seem to be a systematic pattern between MCFs and the debt-to-GDP ratio (Figure 3), the bottom line is that recommendations for countries to rely more on domestic taxation should be treated with caution. The deadweight losses from raising taxes may outweigh the benefits from a decreased debt burden. These countries should take up tax reforms before trying to raise revenue as an alternative to debt.

In sum, to avoid a debt crisis, we suggest three remedies:

- Treat commodity price increases as temporary shocks, not permanent changes; this rule applies to every country.

- Address the cost of taxation in countries where the marginal cost of funds is high before applying a blanket policy of increasing domestic revenues to reduce external debt burdens.

- Make sure that the maturity of loans matches the gestation periods of infrastructure investments.

For another look at Africa’s rising debt and policies to address it, see the recent Brookings Africa Growth Initiative report, Is sub-Saharan Africa facing another systemic sovereign debt crisis?

Related Content

Authors

Commentary

Avoiding a debt crisis in Africa

July 11, 2019