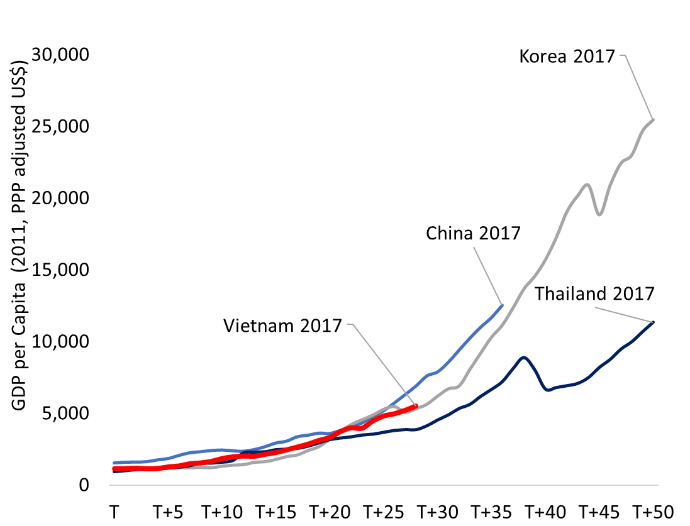

Vietnam is one of the great economic success stories of the 21st century thus far. Just a generation ago, the country was one of the poorest in the world, scarred by decades of conflict and with an economy stifled by a central planning system. Following three decades of virtually uninterrupted rapid growth, Vietnam has emerged as a thriving middle-income economy. Foreign investors are beating a path to its door, demanding to participate in and contribute to its growing prosperity. However, as can be seen from Figure 1, Vietnam’s transition to becoming a prosperous and modern economy has only just begun. Vietnam’s per capita income is currently only about 40 percent of the global average.

Figure 1: Vietnam’s transition to a modern economy is not yet done

T = Year when reforms began

In order to become a high-income country by 2045, Vietnam will need to sustain average growth rates of at least 7 percent over the next 25 years—this would bring GDP per capita to about $25,000. While Vietnam has the potential to meet this aspiration, without reforms, the country is likely to experience a slowdown in growth and fall short of its own aspiration (see Figure 2). A rapidly aging population, tepid productivity, and sluggish investment growth all weigh on Vietnam’s medium-term growth potential. Many of the drivers that propelled the country’s growth in the past will diminish over the next decade. Gains from structural transformation—workers moving from lower-productivity agriculture to higher productivity manufacturing and services—is running its course. Wages are rising and will start to erode Vietnam’s current comparative advantage in relatively low-value, labor-intensive segments of global value chains.

Figure 2: Vietnam’s growth potential is lower than other Asian Tigers

Vietnam will also need to navigate shifting global trade patterns and disruptive technologies, which are both reshaping opportunities and creating new risks. World trade volume has grown by just over 3 percent per year since 2012, less than half the average rate during the previous three decades. Meanwhile, the increasing adoption of advanced manufacturing technologies—robotics, 3D printing, smart manufacturing—in labor-scarce economies and in China exacerbates concerns over wage competitiveness. For example, the sports apparel company Adidas has plans to re-shore production from Vietnam and other low-cost manufacturing hubs to a new 3D printing factory in its home country, Germany. These trends could challenge Vietnam’s ability to continue to emulate the success of Asian Tiger economies but they may also create new opportunities for faster technological catch-up and even leapfrogging. Some evidence from early adopters suggests that new manufacturing technologies may, in fact, boost trade. For example, the production of hearing aids shifted almost entirely to 3D printing over the last decade. Contrary to conventional expectations, this was in fact associated with an expansion of global trade in hearing aids.

So what will it take for Vietnam to take advantage of these new opportunities but also to manage downside risks? We suggest four priorities.

First, accelerate productive investment. Vietnam’s economy is still relatively capital-scarce. This means much is to be gained by boosting the productivity of the country’s abundant labor force with investment in productive infrastructure, machinery, and technology. This will require a more efficient financial system that reduces the cost of financing and allocates Vietnam’s significant domestic savings into productive private sector and infrastructure investment. It will also require removing bottlenecks to private sector investment to de-risk and raise the returns on these investments.

Second, promote a productive workforce with 21st-century skills. Vietnam’s rapidly developing economy requires a new and more complex set of skills and production processes than in the past. According to the recently released World Bank Human Capital Index (HCI), which ranks Vietnam 48 out of 157 countries, the lifetime productivity of a child born in Vietnam today will be only 67 percent of their potential with full education and health. Despite remarkable achievements in expanding educational attainment and quality, only two in three children complete high school and less than one in 10 current workers have a university degree or vocational training. Already today more than half the firms in Vietnam report difficulties in finding workers with relevant skills. Vietnam will need a big reform push to build inclusive and competitive vocational training systems and world-class universities not only to ensure competitiveness but also to enable its people to participate productively in the opportunities offered a rapidly growing economy.

Third, foster innovation. Innovation will need to become a more important driver of increased productivity, both through the upgrading of processes, technologies, and products by existing firms, as well as the entry of high-productivity and exit of low-productivity firms. Opportunities abound for firms in Vietnam to adopt existing knowledge and technologies. Secure intellectual property rights, competition—easy entry and exit of firms—as well as openness to trade and investment are key ingredients to stimulate innovation among firms. For example, Vietnam’s increasing integration into global value chains can serve as a vehicle for diffusion of technology and ideas.

The final and perhaps most important priority: institutions! Institutional legacies, including the still large state-owned sector, incomplete market institutions, and a cumbersome investment climate continue to impede the development of Vietnam’s private sector. With the state still involved in productive activities and resource allocation, questions about a level playing field, independent regulation of markets, and an effective competition framework remain pertinent. This is compounded by fragmentation within and across levels of government, implementation gaps, and weak accountability. If left unaddressed these governance weaknesses may become a drag on future growth and social outcomes.

Related Content

Authors

Commentary

How can Vietnam avoid the middle-income trap?

May 16, 2019