Development strategies have emphasized export led manufacturing growth, which have typically delivered both productivity gains and job creation for unskilled labor. The sector’s tradability in international markets not only reinforced scale economies and technology diffusion, but importantly provided greater opportunities to access demand beyond the domestic market and increased competition. The agricultural sector was also tradable. However, the demand for commodities does not rise much with income, and innovation has largely replaced workers with new capital. Many low-end services could also absorb surplus labor from agriculture but provide little by way of productivity growth. But these characteristics of sectors are starting to change.

Looking ahead, new technologies and shifting globalization patterns raise doubts about both the desirability and the feasibility of manufacturing-led development strategies. Trade is slowing. Global value chains remain concentrated among a relatively small number of countries. The Internet of Things, advanced robotics, and 3-D printing are shifting the criteria that make locations attractive for production and are threatening significant disruptions in employment, particularly for low-skilled labor. These trends raise fears that manufacturing will no longer offer an accessible pathway for low-income countries to develop and, even if feasible, would no longer provide the same dual benefits of productivity gains and job creation for unskilled labor. As a result, the potential risk of growing inequality across and within countries warrants closer attention to the implications of changing technology and globalization patterns.

Considering manufacturing subsectors provides important nuances as to how the promise of productivity growth and employment may be changing. Which goods a country makes matters, not because some goods are inherently superior but because of their potential to provide spillovers, dynamic growth gains, and job creation—and because production processes across subsectors are likely to be differentially affected by changes in technology and globalization in the future.

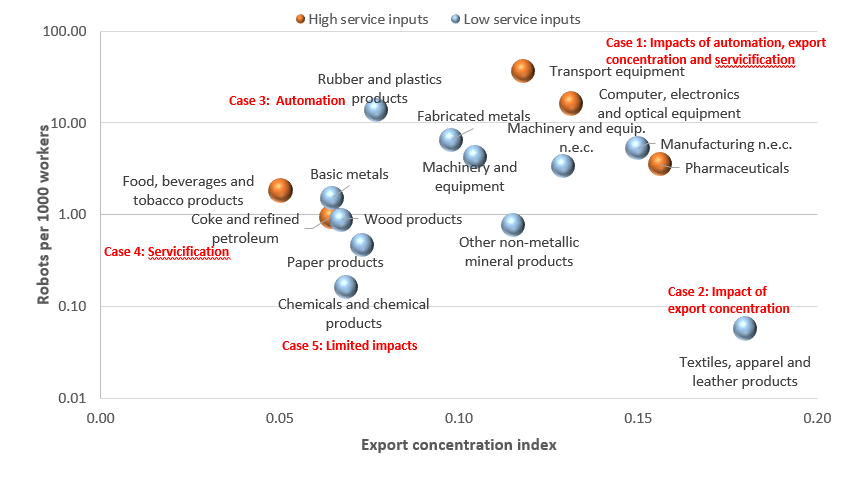

Figure 1: The magnitude of automation, export concentration and services intensity is different across manufacturing industries Sources: Hallward-Driemeier and Nayyar, 2017, Trouble in the Making? The Future of Manufacturing-Led Development. Calculations based on United Nations Industrial Development Organization Industrial Statistics INDSTAT database; International Federation of Robotics (IFR) World Robotics database; and U.N. Comtrade database.

Sources: Hallward-Driemeier and Nayyar, 2017, Trouble in the Making? The Future of Manufacturing-Led Development. Calculations based on United Nations Industrial Development Organization Industrial Statistics INDSTAT database; International Federation of Robotics (IFR) World Robotics database; and U.N. Comtrade database.

There are considerable differences across subsectors, although some groupings do emerge. In Figure 1, sectors on the top right are highly traded and concentrated among top export locations, more automated as per the stock of robots per 1,000 workers, and use professional services more intensively. Therefore, electronics, transportation equipment, and pharmaceuticals are facing multiple changes and a raising bar to stay competitive. On the bottom right, garments, textiles, and footwear are highly traded and have become more concentrated. However, the use of robots is still limited. And services currently play a lower role. Being connected to global markets and having a competitive business environment rather than needing to adopt new technologies is important for countries operating in these sectors. On the left, there are subsectors that are more commodity based. Some, like plastics and rubber, are becoming more automated. Some, like food processing and beverages, increasingly need more complementary services. Most others, however, show little current signs of any of the three outlined sources of change.

As a result, some manufacturing industries will remain feasible entry points for less-industrialized countries and drivers of low-skill employment. Those, where scale economies, increased “servicification,” and new labor-saving technologies reduce the importance of low wages in determining costs, current production processes in less-industrialized countries may not be as viable in the future. Further, if the only way to remain competitive in these industries is the adoption of new technologies, manufacturing’s job creation features will not be as pronounced. On the flip side, if countries can maintain the use of traditional production processes, the job potential would remain. However, the impact on productivity could fall as much of the innovation, and resulting scope for technology diffusion would likely switch to the new technologies.

Manufacturing can therefore remain a part of a successful development strategy—but the dual benefits of productivity and job creation may come in somewhat different combinations. Opportunities to benefit from productivity growth and job creation will also increasingly be associated with the broader manufacturing process—which includes many services. Some, such as finance, transport, and telecom, are embodied in the design, production, and distribution of goods. Others are increasingly embedded in, and bundled with, the goods post-production, such as advertising and marketing, apps on electronic devices, and after-sales consulting. Yet, much like increasingly automated manufacturing sectors, these productivity-enhancing services are unlikely to absorb much unskilled labor. Complacency is therefore not an option on the part of policymakers. There is need to emphasize, with urgency, the competitiveness of the business environment, capabilities of workers and firms, and connectedness to global markets.

“Trouble in the Making? The Future of Manufacturing-Led Development” is a new study published by the World Bank. It was launched on 20 September 2013 and has since been showcased at the WTO Public Forum and the World Bank-SPRING Singapore Global Innovation Forum.

Authors

Commentary

Is the future of manufacturing export-led development in trouble?

October 12, 2017