The COVID-19 global pandemic has brought unprecedented disruption to the global economy, already tremendously impacting livelihoods in Africa by reducing earnings and increasing poverty. While the scale and reach of the impact on employment will differ among countries and sectors, the main effects will be a drop in earnings (income) and increased underemployment (reduced hours) rather than unemployment. Quick action to reduce damage to livelihoods could reduce the social and economic costs this year and in the future. In this blog, we discuss how to reduce the income losses of formal sector employee earnings; in our next blog we will discuss how to shore up incomes in the informal sector.

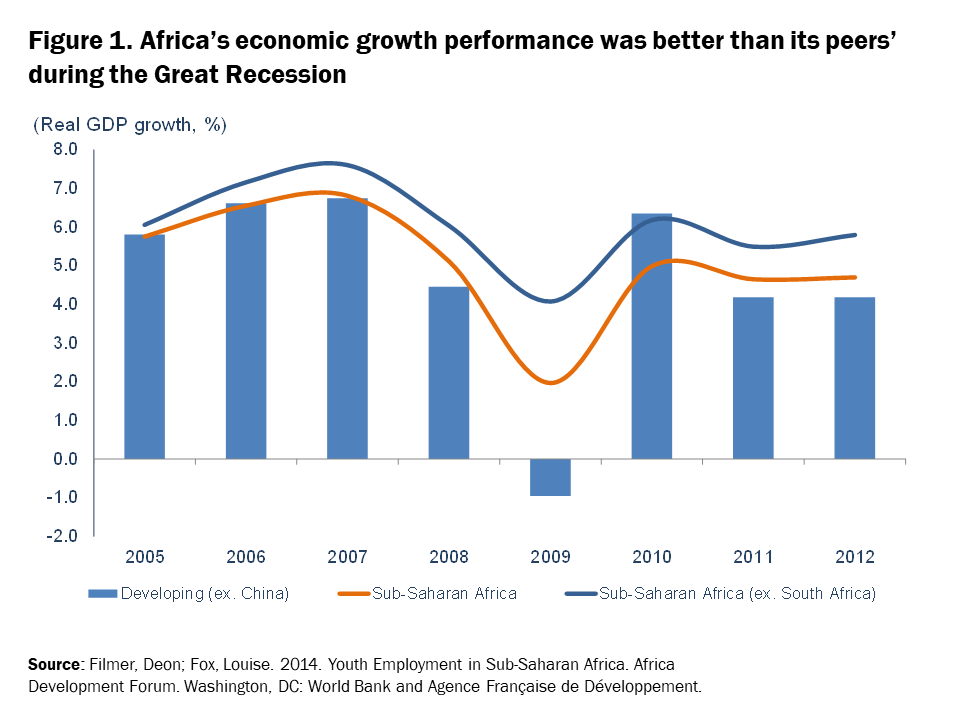

During the Great Recession, to the surprise of many, African low- and lower-middle-income economies (LICs and LMICS, respectively) did not suffer the economic decline that other developing countries did (Figure 1). While economic growth in all developing countries averaged -1 percent in 2009, for the LICs and the LMICs in sub-Saharan Africa, average economic growth was about 4.5 percent. Earnings and consumption continued to rise, and the share of the population in extreme poverty continued its slow decline. Higher prices for mineral and commodity exports buoyed Africa’s economies, and their lower level of globalization kept them (somewhat) insulated from the decline experienced by richer economies. Following the debt forgiveness of the early 2000s, African countries had the fiscal space to shore up local demand and continue public investments. Africa’s strength was its large, informal economy of household farms and firms, which continued to supply the domestic market in response to higher food prices and increased domestic demand.

African countries will not be so lucky this time. As with the previous worldwide recession, global supply chains have been disrupted and overall global demand for goods and services has dropped precipitously. In Africa, high debt levels limit fiscal space and the likely large health care costs—to be borne by both the public sector and households—will drain any available savings and eat into households’ assets. Exacerbating these problems are low mineral prices and export earnings, and the weather is not helping—drought threatens many farmers and urban dwellers in southern Africa, while flooding and locusts are destroying crops in East Africa. Declines in domestic and foreign demand threaten formal firms, while the informal economy, where three-quarters of Africa’s labor force works, will not be able to buffer these forces this time without help from governments. Regardless of the type of employment, belts will have to be tightened as incomes contract.

What will happen to public and private sector employees?

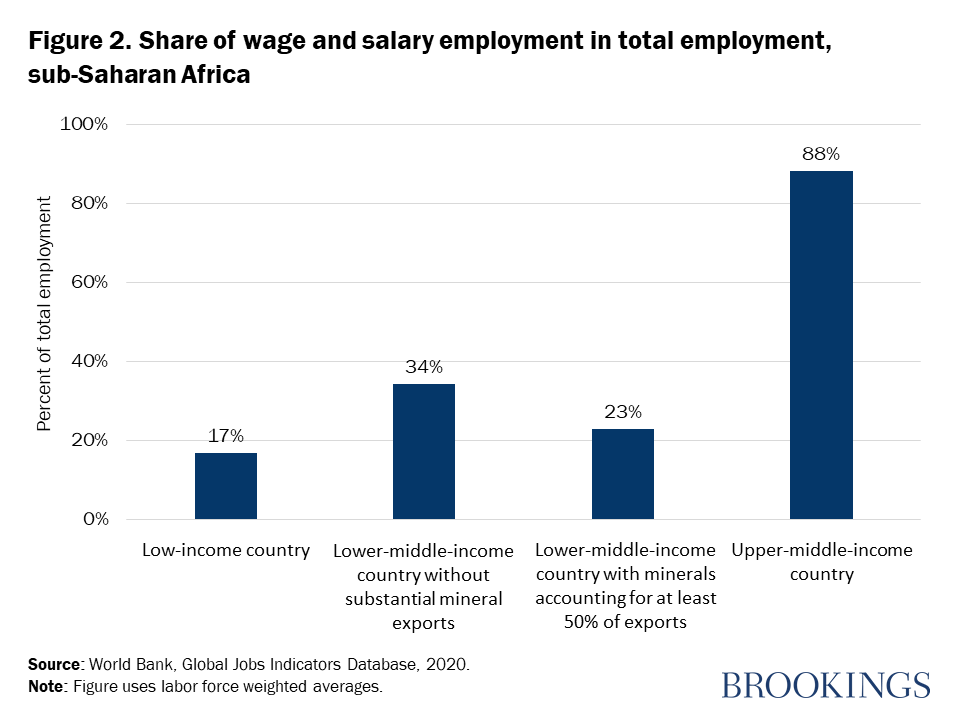

Wage and salary employees account for about 15 percent of total employment in LICs and 20 to 35 percent in non-mineral exporting LMICs, with a smaller share in mineral-rich countries even as income grows (Figure 2). Of that, public sector employment accounts for about one-third of all employment in LICs, one-sixth in LMICs, and almost half in resource-rich countries. About half of private sector wage employment is casual or temporary work, not backed by formal contracts. As in the U.S., these casual workers are almost certain to lose most or all income as firms cut back while facing the pandemic. While firing formally hired public and private workers is expensive in the region, private firms without revenue will do it anyway, but they may first incur wage arrears and/or try to make only partial wage payments.

Prior to COVID-19, the private sector in Africa was already having difficulty accessing markets due to infrastructure limitations, corruption, and the high cost of doing business—hindering new job creation more broadly. Now, the virus has further disrupted markets through measures like travel bans, social distancing, and restricted economic activities, leading to a drastic decline in demand for goods and services, especially in sectors such as hospitality, tourism, transportation, and manufacturing for local markets (e.g., food and beverage).

Many of the 24.3 million jobs supported by the tourism industry are at risk in the short and medium term, owing to reductions in tourist arrivals as concerns about safety take precedence over business travel needs and leisure tourist intent. In the U.S., as of the end of April, 70 percent of hotel employees had been laid off or furloughed; similar data are not yet available for Africa. Consumer goods and retail—especially businesses that depend on imported products from affected countries—have also been hit hard by supply disruptions. Even when lockdown measures are relaxed, pay cuts and job losses will leave households with far less disposable income to spend in these sectors.

Some companies are repurposing production lines, but that doesn’t mean employees won’t be fired: As of May 7, Uganda’s Premier Distilleries—which repurposed production lines to make hand sanitizers—had only retained 20 percent of its employees. Although the telecoms and tech industries are not anticipated to be the most affected, some companies have already announced layoffs of 10 percent to 30 percent of their staff due to the limited business expansion caused by the pandemic. Private sector activities in South Africa reached a record low in April, as many companies shut down operations in response to a nationwide lockdown. IHS Markit analysts predict unemployment will reach 40 percent soon while GDP will drop 12 percent in 2020 in South Africa alone.

Related Books

Export sectors will suffer. For example, in 2019, Kenya was the largest exporter of cut flowers in Africa. In only a couple of weeks in early March, Kenyan flower exports to the European Union fell 50 percent, putting about 1 million direct and indirect jobs at risk. Mineral exports, which were already down due to low prices and low demand (especially from China), are expected to stay low this year. The number of jobs in the mining, oil, and gas sectors is relatively low compared to output volumes, but they are well paid. Now, the closing of mines or halt to new production will affect employment in countries such as South Sudan, Angola, Ghana, the Democratic Republic of the Congo, Equatorial Guinea, Zambia, South Africa, Gabon, and Nigeria. Meanwhile, companies trying to stay afloat will be handicapped by unpredictable temporary shortages of imported inputs (as they are in the West).

Access to finance has always been a challenge for the private sector in Africa. The banking system is inefficient and bureaucratic and—without government support—will not extend additional financing to private sector firms trying to stay afloat. Startup and growth funding will dry up because non-bank intermediaries and accelerators will suffer from a shortage of capital. AfricArena, a well-known accelerator, is anticipating a 40 percent decrease in startup funding. Inability to raise capital is already putting jobs at risk.

As African governments are receiving debt relief and emergency assistance from international financial institutions and bilateral partners, job losses are not expected for civil servants. Given firing costs, the public sector is expected to retain its workers, but salary payment delays could occur—or in some cases, continue—depending on the country’s fiscal position. Already, a number of ministers and other high-ranking, highly paid officials in countries such as Rwanda, Mozambique, and Kenya have agreed to reduce their own salaries as a precursor to further public sector belt-tightening. Overdue payments to private sector suppliers (arrears)—already on the rise even before the COVID-19 crisis—can be expected to increase further, contributing to a cash crunch for private sector firms and stressing the banking system.

The situation may be different for publicly owned corporations (including utilities). These workers are usually unionized, but do not have civil service protections. Reduced product demand as well as increased payment arrears from public and private customers will result in delayed pay, layoffs and reduced work schedules, or even firings, depending on the length of the economic disruption.

What should governments do to protect incomes of public and private employees?

Recent promises of short-term debt relief; public sector liquidity funding from the IMF, the World Bank, and the African Development Bank; emergency food from the U.N.; and funding for urgent health supplies from bilateral donors and NGOs will provide African governments with urgently needed funding. Development finance institutions (DFIs), bilateral and multilateral, have announced new financing for their private sector clients (mostly medium and large businesses).

In addition to providing increased liquidity for the public sector and support for the health system, funds from overseas donors should be combined with domestic resources to reduce income losses of private sector wage and salary employees in order to sustain urban households and buttress domestic demand for goods and services. Key measures should include.

1. Avoiding, or at least limiting, arrears to private firms from the public sector, especially in supply chains for critical sectors like health and education. This will limit knock-on effects that will delay the recovery.

2. Providing finance for the private sector in Africa to save jobs, unlock Africa’s business potential, and continue the momentum of the past couple of decades.

- Bilateral and multilateral DFIs need to provide about 2 billion to 5 billion euros ($2.2 billion to $5.5 billion) of “new capital, increased risk tolerance, temporary suspension of minimum return requirements and new credit lines and guarantees,” according to a recent study. This financing is needed to keep the businesses afloat and support employment. International financial institutions such as the African Development Bank should provide resources directly to public and private banks so that they can help small and medium enterprises (SMEs). The African Development Bank has already provided $40 million to Angola’s Bank Millennium Atlântico to support jobs through the financing of SMEs.

- Governments could finance the rest of the private sector through tax waivers and extended deadlines for tax filing. Central banks should lower or stabilize interest rates (as has happened in Uganda and Nigeria), provide special financial resources to public and private banks, as well as ease regulations to reduce the cost of borrowing and make access to capital easier and faster for private businesses (while keeping in place measures preventing illicit flows).

Related Content

Authors

Commentary

COVID-19 and the future of work in Africa: How to reduce income loss for formal sector employees

May 21, 2020