A new report released this month by the European Investment Bank (EIB), “Banking in Africa: Delivering on financial inclusion, supporting financial stability,” highlights progress in financial inclusion and banking expansion in Africa. The report documents increasing financial inclusion in sub-Saharan Africa led by the adoption of mobile payment services across the continent. In 2017, 43 percent of the region’s population had access to an account (including mobile money accounts), up from 23 percent in 2011. Accounts at financial institutions have grown more slowly, rising from 23 to 33 percent of the population during 2011-17.

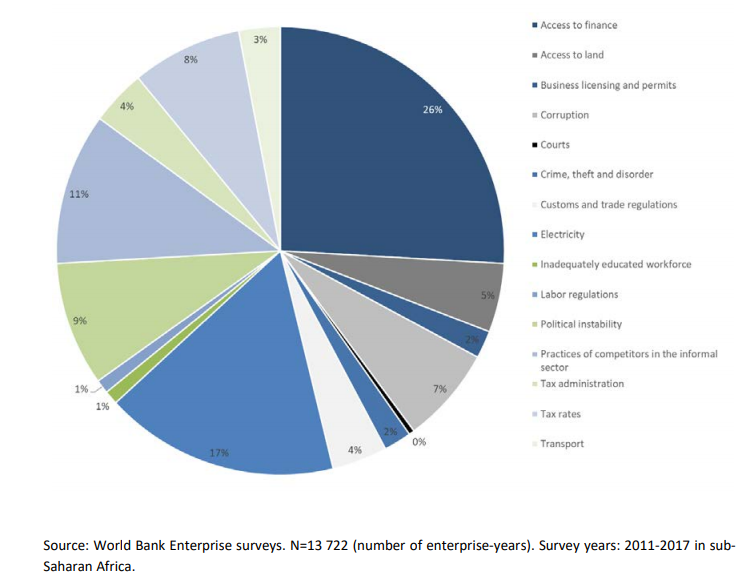

The report also documents the current financing landscape for small and medium-sized enterprises (SMEs) and the challenges faced by financial institutions in extending credit to SMEs using data from World Bank Enterprise Surveys and a 2018 EIB survey of banks in sub-Saharan Africa. As Figure 1 shows, 26 percent of survey respondents between 2011 and 2017 in sub-Saharan Africa listed access to financing as their biggest challenge, making it the most cited obstacle for their business. Electricity is second at 17 percent and competition from the informal sector is in third place at 11 percent. This limited access to finance is further highlighted as almost three-quarters of surveyed SMEs were financed by internal funds and only 10 percent have used bank finance.

Figure 1: Biggest business obstacles for SMEs in sub-Saharan Africa

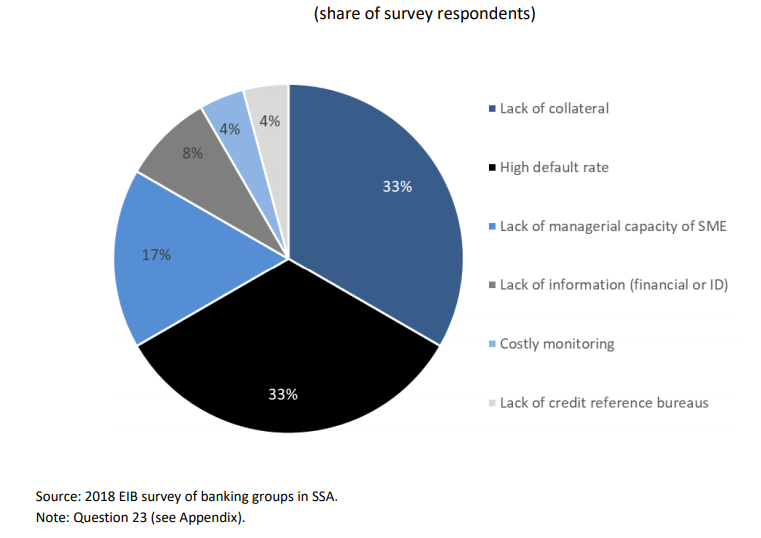

For banks, as Figure 2 shows, lack of collateral and high default rates are the main challenge in lending to SMEs. Credit information gaps and high cost of monitoring borrowers together are cited by 16 percent of banks in the survey. Outside of SME specific constraints, increasing bank lending to the public sector in recent years has crowded out private sector lending in some countries, affecting SME lending in particular.

Figure 2: Main obstacles to SME lending

The report suggests that improving managerial capacity and access to credit information are areas where development partners can play a role through training and technical assistance. Helping SMEs improve financial reporting can increase their chances of getting bank credit. Further, well-developed credit bureaus can increase access to financing and lower interest rates for borrowers that are otherwise unable to demonstrate good creditworthiness, by making their information readily available to lenders.

Related Content

Authors

Commentary

Figures of the week: Financing for small and medium-sized enterprises in sub-Saharan Africa

November 30, 2018