Last week, the Africa Department at the International Monetary Fund released its biannual Regional Economic Outlook for Sub-Saharan Africa. Each edition of the report includes analysis of current development issues and provides updates on key macroeconomic indicators in the region. This edition forecasts average GDP growth recovering from 2.8 percent in 2017 to 3.4 percent in 2018. Rising debt levels, as 40 percent of low-income African countries are in debt distress, are highlighted as a key challenge in sustaining the region’s growth recovery.

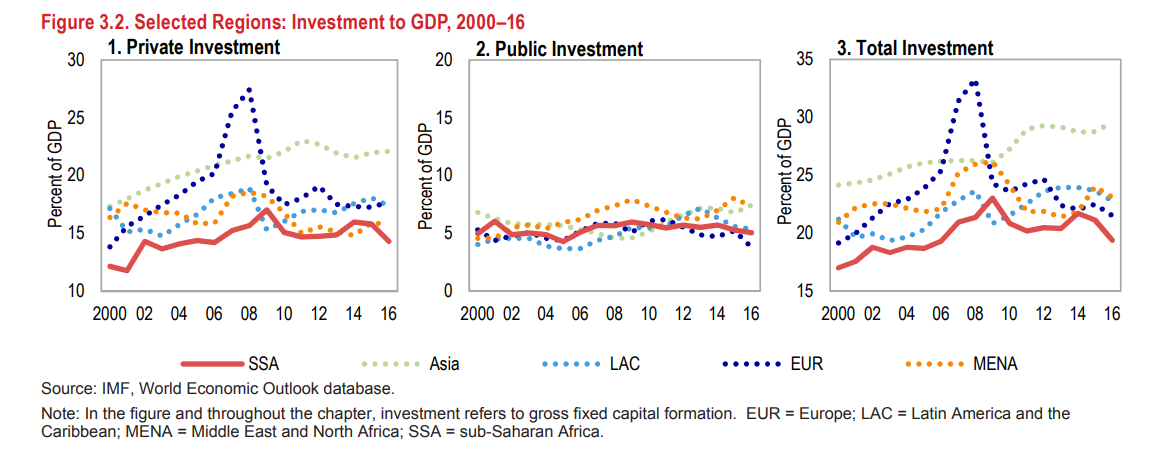

Private investment in the region, the net increase in physical assets there, is one of the main topics covered in this year’s report. As Figure 3.2 shows, private investment in the region has been rising since the early 2000s. Within sub-Saharan Africa, private investment levels have been lowest for oil exporters, at 14 percent of GDP over 2010-2016 compared to 15 percent for non-resource-intensive countries and 17 percent for other resource-intensive countries.

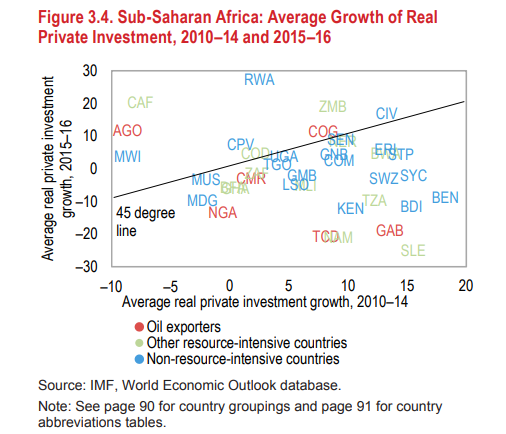

The rising trend in private investment has recently reversed as average private investment growth slowed or turned negative in a majority of countries in 2015-2016 compared to their 2010-2014 averages (Figure 3.4). The report attributes this slowdown to lower commodity prices, particularly oil, during the period and likely spillovers from slower growth in the region’s largest economies (Angola, Nigeria, and South Africa). Policy shocks, such as the interest rate caps in Kenya, slowed credit growth, negatively affecting private investment.

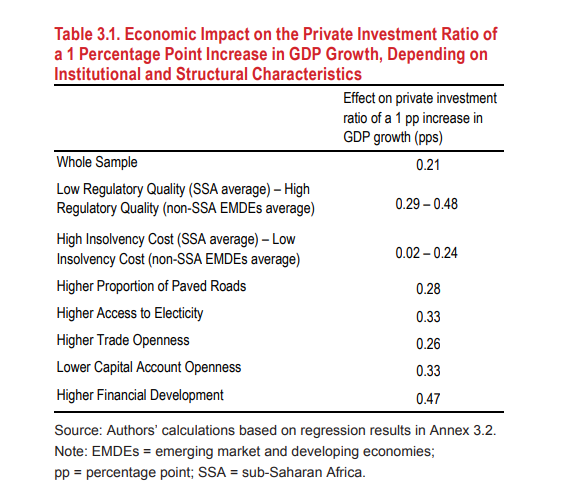

The report finds that private investment increases when GDP growth is high (above an individual country’s historical average); however, the effect on private investment depends on institutional and structural factors. Across the full sample, a 1 percentage point increase in GDP growth rates leads to a 0.21 percentage point increase in the private investment rate. However, as Table 3.1 shows, the impact of higher GDP growth on private investment is lower in environments with low regulatory quality and higher insolvency costs, with an average difference of 0.2 percentage points. This trend suggests that reforms that strengthen the judiciary and regulatory environment are crucial for promoting private investment during periods of strong economic growth.

The report finds larger impact on private investment from increased GDP growth in countries where access to electricity, trade openness, and financial development are higher than the global median (Table 3.1). In countries with very low levels of financial development, firms do not invest in new capital to enhance capacity even when there is strong demand for their products and a favorable economic climate. Thus, more developed financial markets and increased bank lending are highlighted as key areas to support increased private investment. The report recommends reforms such as strengthening financial protections for investors and improving technical and regulatory infrastructure for the development of equity and bond markets.

Authors

Commentary

Figures of the week: Private investment trends in sub-Saharan Africa

May 17, 2018