LABOR

NAFTA-USMCA and wages in Mexico

The North American Free Trade Agreement (NAFTA) represented a significant step towards the integration of the three economies of that region. Launched in 1994, it superseded a previous agreement between Canada and the U.S., so the substantive change was the incorporation of Mexico, a country with a relatively lower average per capita income. NAFTA made significant advances in trade and foreign investment regulations but excluded any binding provisions on immigration or the free movement of labor (other than commitments to enforce pre-existing legislation). Indeed, the expectation was that trade in goods would in part substitute for trade in factors, particularly labor, so that the agreement would narrow wage differences between Mexico and its two northern partners.1

Assessing the impact of NAFTA on wages in Mexico is complex because they respond to many circumstances, not all related to trade. Ideally, one would like to perform a “counterfactual exercise” to identify what wages would have been without NAFTA keeping constant all other factors.2 This exercise is not attempted here. Rather, this note focuses on some features of Mexico’s labor market that, in our view, have been insufficiently considered in previous analyses.

In our assessment we find that:

- Despite NAFTA, average wages in Mexico did not increase from their pre-NAFTA levels, although in its absence they would have been marginally lower.

- So long as Mexico’s current domestic regulations remain — particularly those pertaining to labor and social insurance — it is unlikely that the U.S.-Mexico-Canada Agreement (USMCA), the trade pact that superseded NAFTA in 2019, will lead to higher average wages.

- If the USMCA increases labor costs significantly in the USMCA-related segment of the economy, aggregate productivity in Mexico may suffer.

Wages in Mexico

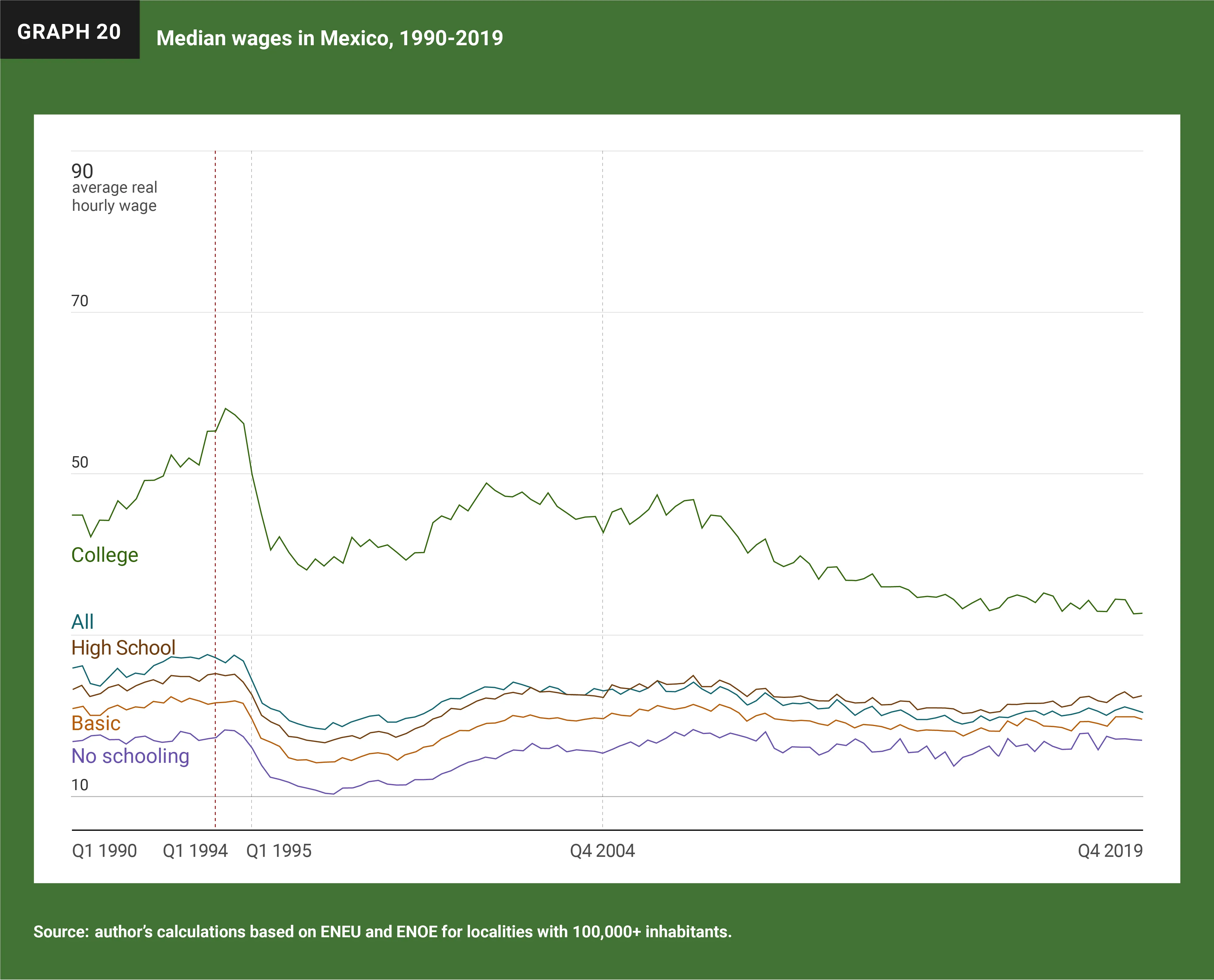

The black line in Graph 19 shows the average real urban hourly wage between 1990 and 2019.3 In this and the next graph (Graph 20), the first dashed vertical line marks the beginning of NAFTA, the second the 1994-1995 financial crisis, and the third the change in employment survey from Encuesta Nacional de Empleo Urbano (ENEU) to the Encuesta Nacional de Ocupación y Empleo (ENOE).

After an initial upward trend starting in 1990, there is a sharp drop in 1995 associated with the financial crisis. This is followed by a gradual recovery, with the net result that in 2019, the real average urban wage is practically the same as in 1990. This is a puzzling result for two reasons: Mexico recovered macroeconomic stability quickly after the 1995 crisis and average years of schooling increased by 47 percent from 1990 to 2019 (from 6.6 to 9.7 years). Since workers with more schooling earn higher wages, one would expect that as average years of schooling increase, so would the average wage, more so in a context of macroeconomic stability and increased trade and investment flows with Canada and the U.S.

The reason this did not occur is displayed in the colored lines in the same graph, separating workers into four schooling categories.4 Wages for workers with college education have fallen in absolute terms, and have remained constant for those with fewer or no years of schooling. Wages of workers with more schooling fell because their supply outpaced their demand and this, together with the fact that their share in total employment increases over time, pulls the average down. This is partly compensated by the fact that the share of employment by workers with little or no schooling moved in the opposite direction, resulting in a stagnant average.5

Graph 20 uses the same data as Graph 19 but shows median rather than average wages, showing that the wage distribution is not symmetric. The average mean wage is higher than the average median wage (also in black), indicating that a few high-income workers pull the average mean wage over the average median wage. Over time fluctuations are more nuanced than those shown in Graph 19, but the basic result stands: For the period captured in the graphs, the average median wage was constant, with a downward trend for those with college education.

Impact of NAFTA on wages in Mexico

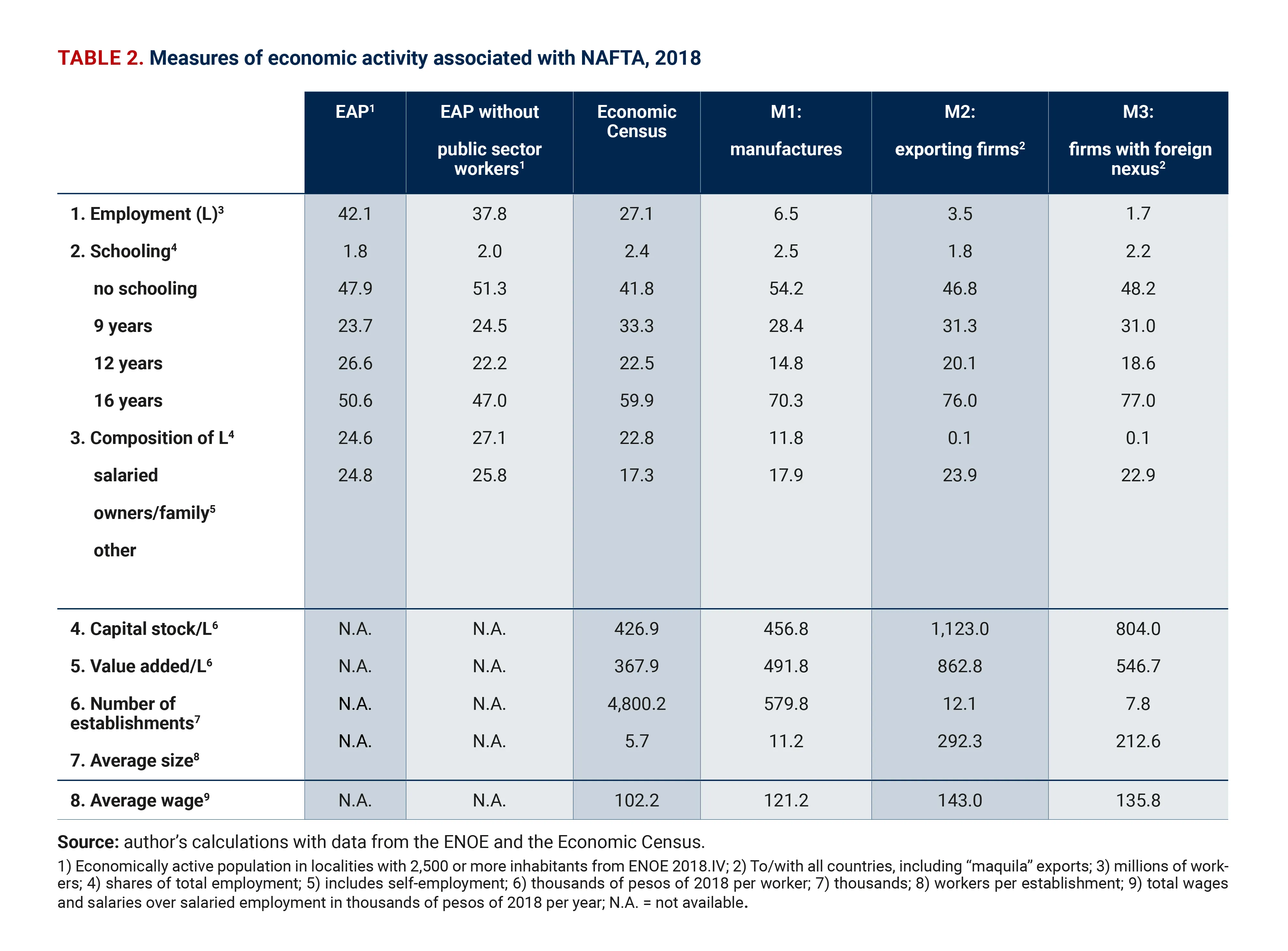

How are Graphs 19 and 20 related to NAFTA? Unfortunately, the employment surveys contain little information regarding the firms where workers are employed. Table 2 remedies this, combining information on workers from the ENOE with information on firms from the 2018 Economic Census, the last one available.6 The first two columns show measures of employment and schooling from the ENOE, for localities of the same size as those considered in the Census regardless of whether economic activity occurs in a fixed premise or not. As a result, it provides a more complete description of Mexico’s urban labor market than the Census which, despite its name, excludes part of urban economic activity.

The next four columns show measures of employment and schooling from the Census and other variables not collected in the ENOE. The first refers to the whole Census and the last three to alternative measures of economic activity associated with NAFTA: All firms in manufacturing (M1); all firms that export (M2); and all firms with a foreign nexus (M3). The first measure assumes that all firms in manufacturing export to Canada or the U.S. or compete with imports from those countries in the domestic market. The second measure captures exports to all countries but is a good proxy of those going to Canada and the U.S., since around 85 percent of them have that destination. The third captures firm exposure to the rest of the world. More precisely, it measures whether the firm “participates in integrated processes through contracts or economic collaboration programs with firms located in other countries” (Census questionnaire, our translation). It also overestimates the importance of NAFTA since the question refers to all countries, and although in this case there is little information to judge by how much, it is safe to assume that most links occur with Mexico’s two northern neighbors.

None of these measures are fully satisfactory. M2 and M3 are probably too narrow since they exclude firms that produce inputs for exporting firms or focus only on firms with contractual arrangements with foreign ones. On the other hand, M1 is probably too broad since it assumes that all manufacturing firms compete with Canadian or U.S. firms. Considered jointly, however, they are a reasonable first-order approximation to the relative importance of economic activity associated with NAFTA.

Consider the first block in Table 2. Line 1 shows that there were 42.1 million urban workers in 2018. However, the Census only captures 27.1 million, or 64 percent (72 percent excluding public sector workers). The difference is explained by the fact that 10.7 million urban workers carry out their activities in the streets and are therefore not included in the Census. Note that by any of the three measures used, NAFTA-related employment is not large: 15 percent of all urban employment in the case of M1, 8 percent for M2, and 4 percent for M3.

While NAFTA has had a small positive effect on urban wages in Mexico, it has not been sufficiently powerful to offset other forces that keep labor earnings low.

Line 2 provides information on schooling. Workers with 12 or more years of schooling represent 50 percent of the whole urban labor force (47 percent excluding public sector workers) but 55 percent of that captured in the Census. This share is lower for M1, 43 percent, but very similar for the two other measures of NAFTA-related activities, 51 percent for M2 and 50 percent for M3. Note that the share of workers with 16 or more years of education is lower in all three measures compared to the whole urban labor force, with or without public sector employees. These figures suggest that all in all, NAFTA-related activities are not more intensive in educated workers than all other urban activities.

On the other hand, line 3 shows that the composition of employment varies substantially between the ENOE, the whole Census, and NAFTA-related activities. In the ENOE, excluding public sector employment, salaried workers — who are paid salaries and wages — account for less than half of the labor force, 47 percent. The second largest share, 27 percent, is accounted for by workers who run their own business or work for a family enterprise and are remunerated through profit-sharing or other arrangements.7 These shares reflect the critical role played by self-employment and small family firms in Mexico. The contrast with the composition of employment captured in the Census is large. The share of salaried employment increases to 60 percent for the whole Census, and to between 70 to 77 percent depending on the measure used of NAFTA-related employment. In parallel, the share of owner/family firm employment falls, and is almost negligible for M2 and M3.

Consider now the second block: Lines 4 and 5 show that regardless of the measure used, NAFTA-related employment occurs in more capital-intensive firms and has higher labor productivity, as measured by value added per worker. Note that the differences are particularly large when we use M2 and M3. Differences in firm size are also quite sharp.

Finally, line 8 in the third block compares the average wage between the whole Census and NAFTA-related activities. The measure is very rough but is the only one that can be constructed with the Census data.8 The differences are notable: 19 percent higher for M1, 40 percent for M2 and 35 percent for M3, and that, prima facie, they cannot be attributed to differences in schooling. That said, it should be noted that unfortunately the information on workers’ characteristics in the Census is very rough and only refers to years of schooling. As a result, one cannot discern the extent to which the difference in average wages reflects differences in other dimension of human capital not captured in the Census (e.g., experience, on-the-job learning) or the fact that firms in NAFTA-related activities capture rents, which they shared with their workers in the form of higher wages. What is clear is that wages in NAFTA-related activities are higher than in the rest of urban economic activities and therefore raise the average urban wage.

Altogether, the picture that emerges from Table 2 is that NAFTA-related activities, particularly when measured by M2 or M3, are markedly different from those captured in the ENOE or even the whole Census. While they are not more intensive in workers with more years of schooling, they occur in substantially larger and more capital-intensive firms, with a different salaried/non-salaried employment composition and with higher average wages for salaried workers. That said, only a tiny share of all firms is directly engaged in NAFTA-related activities, 0.003 percent in the case of M2 and 0.002 percent in the case of M3, and even though these firms are 37 to 51 times larger, they nonetheless directly employ a small share of urban workers (8 percent in M2 and 4 percent in M3). These conclusions hold under the more generous M1 measure of NAFTA-related activities, although the differences are not as sharp, including in average wages.

We do not attempt here to estimate wages in the no-NAFTA scenario, although the discussion suggests that results would be more disappointing than those shown in Graphs 19 and 20.9 We conclude that while NAFTA has had a small positive effect on urban wages in Mexico, it has not been sufficiently powerful to offset other forces that keep labor earnings low. In particular, the forces that have overtime depressed the earnings of workers with more years of schooling; NAFTA has helped but clearly far from enough.10

A few remarks on labor regulations in Mexico

Mexican labor institutions are very different from Canada and the U.S. First, labor and social security laws in Mexico make a critical distinction between salaried and non-salaried workers. The former have a relationship of dependency and subordination with respect to a boss/firm in exchange for a wage. The latter work for themselves or for firms but are not paid wages because they are engaged under contractual arrangements that do not imply subordinated labor. Second, only salaried workers are covered by minimum wage regulations, can form unions, and have the right to strike for better benefits and working conditions. Third, only firms and salaried workers are obligated to contribute to social security programs which, as opposed to Canada and the U.S., include various types of pensions, health insurance, housing, and daycare services. Finally, salaried workers do not have unemployment insurance; rather, they are protected from the loss of employment by stringent job stability regulations. These considerations matter greatly since most of the labor provisions in NAFTA and now USMCA, apply only to salaried labor.

The functioning of the associated institutions is also different. For many reasons, salaried workers in Mexico undervalue the benefits of social security programs, so that there is an implicit tax on salaried employment. In parallel, non-salaried workers have access to some social benefits that, while not exactly equivalent to those for salaried ones, are free (Levy, 2008, 2019). The implicit tax on salaried employment, combined with stringent job stability regulations, on one hand, and the implicit subsidy to non-salaried employment, on the other, have two effects. First, they induce firms hiring salaried workers to evade labor and social insurance regulations, a situation that is facilitated by their imperfect enforcement. Second, they induce firms to elude these regulations through non-salaried contractual arrangements and promote self-employment. The result is that the labor market is segmented into two groups of workers: Salaried ones employed by firms that comply with the relevant labor and social insurance regulations, henceforth called “formal.” The rest are categorized as “informal,” a heterogenous group made up of salaried workers hired by firms that do not comply with the relevant regulations, self-employed and domestic workers and, very importantly, workers associated with firms without salaried contractual agreements.

The segmentation of the labor market is reflected in the structure of Mexico’s firms, which also divide into formal and informal depending on whether they hire salaried workers and comply with labor and social insurances laws or not. Importantly, firms can be informal without breaking these laws if they engage with workers without salaried contractual arrangements. These distinctions matter greatly. In 2018, 90 percent of all firms captured in the Economic Census were informal, 65 percent legally so. Informal firms, legal and illegal, are substantially smaller than formal ones (as measured by the number of workers), less capital intensive, controlling for size demand relatively fewer workers with more years of schooling, and on average have lower productivity than formal ones (Levy, 2018).

The formal-informal dichotomy, a central feature of Mexico’s economy and a critical determinant of labor market outcomes, has been resilient to increases in the years of schooling of the labor force and to structural changes in output markets, as exemplified by NAFTA. In 2005, the first year of the ENOE, the urban labor informality rate was 58 percent, not that different from the one observed at the end of 2019, 56 percent. In the same period, the firm informality rate increased from 84 percent in 1998 to 90 percent in 2018.11 The dichotomy needs to be seen as a deeply engrained structural feature of Mexico — a feature that is hard to rationalize with arguments about insufficient investments in human capital or lack of integration into the world economy. After a quarter of a century since NAFTA, there are two relevant lessons for the USMCA:

- It is difficult to change the labor market through reforms to output markets, particularly when many other regulations that bear on the labor market tend to deepen the formal-informal dichotomy (Levy, 2018).

- So long as this dichotomy persists, it will be difficult for wages to increase, because it is associated with low productivity and a depressed demand for workers with more years of schooling (Levy, 2018; Levy and López-Calva; 2020, Bobba, Flabbi and Levy, 2021).

A few remarks on the potential impact of USMCA on wages in Mexico

As opposed to NAFTA, the USMCA did imply reforms to Mexico’s labor law. These reforms, carried out in 2019, strengthened the mechanisms allowing salaried workers to decide on the unions that represent them and improved enforcement of pre-existing regulations (De Buen and Leycegui, 2021). Importantly, the USMCA included the right by Canadian or U.S. firms to request investigation of non-compliance by Mexico and when appropriate, the imposition of trade-related remedies. However, it did not change the underlying labor and social insurance architecture; in particular, the asymmetry in the treatment of salaried and non-salaried workers with respect to social insurance, nor job stability regulations for salaried workers. It also did not change the scope of social insurance or the functioning of the associated institutions.

By developing new mechanisms to exercise the rights of salaried workers and enhancing the credibility of sanctions in cases of non-compliance, the USMCA strengthened their bargaining power — particularly of those employed by USMCA-related firms. In principle, this will likely raise the labor costs of Mexican firms exporting to Canada and the U.S. or competing in the domestic market with imports from those countries. It is difficult to quantify the magnitude of this effect as it depends on the extent of pre-USMCA violations of salaried labor regulations and the effectiveness of the inspection-cum-sanction provisions. However, the direction is clear: All else equal, production in Mexico for the North American market will be less attractive because labor costs will be higher. Differently put, Mexico will lose some of its competitiveness vis-à-vis Canada and the U.S.12

Will the USMCA increase the average wage in Mexico? We consider two scenarios. But before discussing them, we point out that both ignore any changes in the world economy that independently of the USMCA, could improve Mexico’s comparative advantages (e.g., re-design of regional sourcing patterns triggered by competition between China and the U.S.). The first scenario assumes that the labor provisions of the USMCA are enforced mostly on USMCA-related firms in Mexico and that these firms enjoy rents, so that they can absorb higher labor costs without changing their demand for labor. In this case, the average wage will increase since it is the weighted average of wages in the USMCA-related segment of the economy and the rest (where the weights are the share of employment in each), and since by assumption the composition of employment does not change (implying no change in wages or labor earnings in the non USMCA-related segment of the economy). That said, recall from Table 2 that the share of employment in the USMCA-related segment is small so that the increase in the average wage is bound to be small.

Paradoxically, the “success” of the USMCA labor provisions — assuming this is interpreted as an increase in labor costs to USMCA-related firms in Mexico — may end up lowering aggregate productivity in Mexico, making it more difficult to sustain a higher average economy-wide wage.

The second scenario allows for changes in the composition of employment. If wages or labor costs in USMCA-related firms increase substantially, firm rents will be exhausted, and these firms will adjust employment levels. This can also occur if investments in Mexico become less profitable vis-a-vis Canada and the U.S. because production costs in Mexico increase in response to other provisions in the USMCA like those related to rules of origin.13 The result is that USMCA-related employment falls and, concomitantly, the supply of labor to the non-USMCA segment of the economy increases. Ignoring outward migration or open unemployment, the change in the average wage is now ambiguous, as the increase in the USMCA-related segment is offset by a wage decrease in the rest of the economy and by the lower share of employment in the USMCA-related segment. But even if the change is positive, its magnitude will be smaller than in the first scenario, which already suggested that any wage increase would be fairly small.

Critically, the labor provisions of the USMCA do not change the underlying productivity of firms or workers in Mexico. In the first scenario, they only redistribute rents from firms to workers in the USMCA-related segment of the economy without impacting resource allocation. However, in the second scenario these provisions do change resource allocation, and they do so in the direction of increasing resources to the non-USMCA-related segment of the economy — the segment which, as shown in Table 2, has lower productivity. Differently put, from the point of view of productivity, in this scenario the labor provisions of the USMCA are doing exactly the opposite of what is needed.

Critically as well, note that the likelihood of the second scenario is proportional to the impact of the USMCA labor provisions on labor costs in USMCA-related firms: The greater it is, the greater the shift in resource allocation. Paradoxically, the “success” of the USMCA labor provisions — assuming this is interpreted as an increase in labor costs to USMCA-related firms in Mexico — may end up lowering aggregate productivity in Mexico, making it more difficult to sustain a higher average economy-wide wage.

This brings us to the crux of the matter. The average rate of growth of total factor productivity in Mexico between 1990 and 2017 — a period spanning NAFTA — was (-) 0.43 percent (Fernández-Arias, 2021). Over this period the productivity gap between Mexico and the U.S. widened despite NAFTA. Or to put it differently, NAFTA did not result in productivity convergence between Mexico and its northern neighbors.14

The average wage in Mexico will increase when the productivity of all of Mexico’s economy increases, not only that of its relatively small USMCA-related segment. The average wage will increase when, across the economy, low productivity firms exit the market, high productivity firms grow, and entering firms are more productive than incumbents — something that, at least through 2013, had not occurred (Levy, 2018). The average wage will increase when higher productivity formal firms that are more intensive in workers with more years of schooling are not undercut by lower productivity informal firms. NAFTA was unable to improve overall firm dynamics in Mexico, not because of deficiencies in the agreement itself, but because the forces offsetting it were more powerful. Graphs 19 and 20 illustrate this unfortunate fact. Unless these forces change in Mexico, it is difficult to foresee that the USMCA will produce a different outcome. Labor provisions in the USMCA may help tighten the enforcement of regulations pertaining to salaried labor in a subset of firms in Mexico and redistribute some rents from firms to workers. However, these issues are far removed from the roots of Mexico’s productivity problem.

Endnotes

- 1. Standard trade theory specifies that since relative to the U.S. and Canada, Mexico is the labor-abundant country, NAFTA should result in higher wages in Mexico.

- 2. Various papers attempt to identify the impact of NAFTA on wages and employment in Mexico; see, for instance, Hanson (2003), Esquivel and Rodríguez-López (2003), Robertson (2007), Chiquiar (2008), Vázquez (2013) and Trachtenberg (2018).

- 3. The graph refers to salaried and non-salaried workers aged 18 to 65 working 20 or more hours a week in localities with 100,000 or more inhabitants. The expression “wage” also denotes the equivalent earnings of non-salaried workers. Wages are expressed in prices of 2008. Mexico’s employment survey changed in 2005, making it necessary to join the Encuesta Nacional de Empleo Urbano, ENEU (1990-2004), with the Encuesta Nacional de Ocupación y Empleo, ENOE (2005-2019). Both are quarterly household-based surveys, but the ENEU only samples localities with 100,000 or more inhabitants while the ENOE samples the whole country. To make them comparable, in graphs 1 and 2 we restrict the ENOE to localities with 100,000+ inhabitants. In both surveys, worker’s earnings are measured in pesos and in ranges of the minimum wage but in some cases the peso value is missing. In these cases, we extrapolate its value with the average peso earnings of workers in the same range of the minimum wage.

- 4. No schooling, 9 years of schooling (basic education), 12 years (high school) and 16 years (college). Both ENEU and ENOE provide more granular information on schooling, but we chose these categories to make them comparable with the ones used in the Economic Census; see Table 2.

- 5. In 1990, the shares of workers in localities with 100,000 or more inhabitants with no schooling, 6, 9 and 12 years of schooling were 3.8%, 68.3%, 10.4% and 17.5%, respectively. In 2019 they were 1.1%, 42.4%, 24.7% and 31.8%.

- 6. The Census captures information about all establishments in a fixed premise (i.e., with walls and a roof) regardless of ownership structure or registration with various authorities in urban areas, defined in the Census as localities with 2,500 or more inhabitants. Workers and establishments carrying out activities in the streets are excluded.

- 7. Other type of workers refers to those associated with firms through non-salaried contractual arrangements different from family-type ones, like sub-contracting, who are paid through honorariums or other mechanisms for which there is no information in the Census.

- 8. Wages are best measured with the ENOE, but one cannot identify NAFTA-related activities in it.

- 9. If we mechanically impute the average wage of workers in the Census to workers in NAFTA-related activities, the average would be 1% lower for the case of M2, and less for the other two measures.

- 10. The fall in the returns to education implicit in Graphs 19 and 20 lowers the incentives to invest in schooling in Mexico, as discussed in Bobba, Flabbi and Levy (2021). Thus, one can argue that in the absence of NAFTA there would have been fewer investments in schooling, a positive aspect of NAFTA that sometimes goes unnoticed. Importantly, there is little empirical evidence to support the proposition that the fall in the returns to schooling has been caused by a reduction in the quality of education (Levy, 2018).

- 11. The urban labor informality rate refers to localities with 2,500+ inhabitants, which for the reasons already cited cannot be obtained from ENEU. Focusing only on localities with 100,000+ inhabitants, the labor informality rate was 49.30% in 1990 and 49.28% in 2019. On the other hand, the firm informality rate is calculated from the Economic Census, which is only available every 5 years. However, for technical reasons the 1993 Census cannot be compared with the subsequent ones.

- 12. Of course, USMCA-related firms in Mexico can offset higher costs of salaried labor through labor-saving technologies or productivity gains in their production processes, so that the translation from higher labor costs to lower exports need not be automatic; much depends as well on the behavior of wages in Canada and the U.S. That said, note that these technical changes and innovations would likely reduce the share of employment in USMCA-related activities, particularly if they occur in very relevant ones like automobile production and auto parts.

- 13. USMCA-related firms in Mexico could try to preserve their rents and market share lobbying for looser monetary policy and a lower real exchange rate. We ignore these issues here.

- 14. Various reforms to increase total factor productivity were carried out after NAFTA. However, their impact was fully offset by less-visible changes in tax and social insurance policies that negatively affected the performance of firms and workers in the labor market, and by the persistence of distortions in sectors producing non-tradable goods and of an environment where contracts are enforced imperfectly (Levy, 2018).

References

Bobba, M., Flabbi, L. and Levy, S. (2021). “Labor Market Search, Informality, and Schooling Investments”, forthcoming, International Economic Review.

Chiquiar, D. (2008). “Globalization, Regional Wage Differentials and the Stolper-Samuelson Theorem: Evidence from Mexico”, Journal of International Economics, Vol. 74(1), pp. 79-93.

De Buen, C. and Leycegui, B. (2021). “Los Retos Laborales para México a la Luz del T-MEC”, Reporte SAI: Economia, Comercio e Inversión, Mexico City.

Esquivel, G., and Rodríguez-López, J.A. (2003). “Technology, Trade and Wage Inequality in Mexico before and after Nafta”, Journal of Development Economics, 72(2), pp. 543-65.

Fernández-Arias, E., & Fernández-Arias, N. (2021). “The Latin American Growth Shortfall:

Productivity and Inequality”. Discussion Paper 24, Latin American and Caribbean Bureau of the

United Nations Development Program.

Hanson, G. (2003). “What has happened to Wages in Mexico since Nafta?”, National Bureau of Economic Research, Working Paper 9563.

Levy, S. (2008). “Good Intentions, Bad Outcomes: Social Policy, Informality and Economic Growth in Mexico”, Brookings Institution Press.

Levy, S. (2018). “Under-Rewarded Efforts: The Elusive Quest for Prosperity in Mexico”, Inter-American Development Bank.

Levy, S. (2019). “Una Prosperidad Compartida: Transformando la Seguridad Social en México para Crecer con Equidad”, Banco Interamericano de Desarrollo, Nota Técnica IDB-TN-1788.

Levy, S., and López-Calva, L.F., (2020). “Persistent Misallocation and the Returns to Education in Mexico”, World Bank Economic Review, Vol. 34 (2), pp. 284-311.

Robertson, R. (2007). “Trade and Wages: Two Puzzles from Mexico”, The World Economy, pp. 1378-98.

Trachtenberg, D. (2018). “Local Labor-Market Effects of Nafta in Mexico: Evidence from Mexican Commuting Zones”, InterAmerican Development Bank, Working Paper WP-01078, Washington, D.C.

Vázquez, R. (2013). “Why did Wage Inequality Decrease in Mexico after Nafta?”, Economia Mexicana, vol (22), 2, pp.245-78.

Acknowledgements

We thank Manuel Ramos Francia for very useful comments and suggestions.

Viewpoints

Liz Shuler explains how the AFL-CIO came to support the U.S.-Mexico-Canada Agreement.

Jerry Dias explains how the U.S-Mexico-Canada Agreement broke new ground by rewriting the labor conditions of trade.

Related